Goldman’s commodities team, which for most of 2021 has been extremely bullish on the price of oil which it sees rising to $90 by year end and remaining higher for years to come, has not been exactly timid in its view on what Biden’s SPR release will do to the price of oil: two months ago, when the idea was first floated, Goldman said that an “SPR Sale Would Release Only 60MM Barrels; Will Bring Even Higher Oil Prices“, and then, less than a week ago when oil prices tumbled, the bank said that with Brent below $80, “A Biden SPR Release Is Now Fully Priced In And Will Send Oil Price Even Higher In 2022.”

Well, Goldman was right, and as we showed today, Brent exploded higher after news of the smaller than expected SPR exchange (not release) finally hit turning sell the rumor into a “buy the news” frenzy.

Not surprisingly, after the dust finally settled, it was time for Goldman’s commodity guru Damien Courvalin to take a victory lap and in a note titled “A Drop in the Ocean” (it’s all too clear what the title was referencing)…

… he writes that as details of government crude reserve releases started being released today, with 50 million barrels (mb) from the US and as much as 30 mb from Korea, Japan, China, India and the UK, “the aggregate size of the release of c. 70-80 mb was both smaller than the 100+ mb the market had been pricing in, with the swap nature of most of these barrels implying an even smaller c. 40 mb net increase in oil supplies over 2022-23.” That, as Courvalin points out, is in the context of a market drawing up to 2mb/d at present!

Translation: enjoy the low oil and gas prices while you can… we are going much higher.

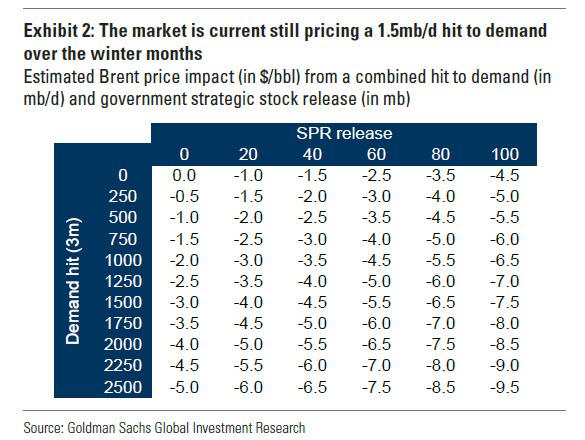

How much higher? As Courvalin explain, on his pricing model, such a release would be worth less than $2/bbl, significantly less than the $8/bbl sell-off that occurred since late October. So at $82/bbl currently, Brent prices are in fact not only pricing in today’s announced release, but an additional hit to global oil demand of 1.5 mb/d for the next three months. That is equivalent to pricing in both a repeat of last winter’s 1 mb/d hit to EU oil demand due to the COVID wave (which occurred in the absence of vaccinations) as well as a repeat of this summer’s 0.5 mb/d hit to Chinese demand from lockdowns.

Needless to say, the Goldman strategist views these as “excessive concerns over the next three months, leaving the recent sell-off overshooting fundamentals due to the year-end decline in trading activity.”

Separately, while Goldman concedes that on their own, the coordinated government stock releases would warrant a $2/bbl downgrade to the bank’s $90 year-end Brent price forecast, it sees offsetting risks from the lack of progress on negotiations with Iran. To be sure, the restart of negotiations next Monday, November 29, will provide some sense of potential timeline to an agreement, with clear risks that Goldman’s assumption for an April lift of sanctions (and February onward unwind of 60mb Iranian floating storage) could prove too optimistic. In addition, and in retaliation for the SPR release, OPEC could easily consider halting its production hikes to offset the detrimental SPR impact of lower oil prices on the needed recovery in global oil capex, likely justifying such action as prudent in the face of COVID demand risks.

In conclusion, Courvalin reiterates his view that such government intervention is not the solution to higher oil prices that are required to overcome the slow supply response of producers, something he discussed earlier this week. This instead has been driven by:

- the damage to investors caused by oil producers’ capital destruction over the last seven years, now compounded by ESG allocation inefficiencies, and

- the demand uncertainties of COVID, China and energy transition.

One thing is certain: neither of these two will be resolved by palliative measures such as an SPR release, or potentially counter-productive measures, such a US export ban.

One final point: while not even the Biden admin is dumb enough to consider it, some have speculated that once the SPR release is shown to be a total disaster, Biden may implement an oil export ban. The problem: this would have catastrophic consequences. As Goldman explains, a US export ban would significantly disrupt the US and global oil markets, and potentially be a counterproductive tool to attempt to lower oil prices.

The US exports 3 mb/d of crude and domestic pipelines would not be able to reroute these volumes to US refiners, which further don’t have enough capacity to process this much crude. This would leave excess US crude supply quickly reaching tank tops and forcing shut-in production, with investment and production soon to enter significant declines. At the same time, the global market would be deprived of 3 mb/d of US supply (light sweet crude that is Brent like in quality). Brent prices would therefore need to spike to push demand lower as there is simply not enough spare capacity (nor suitable crude) to replace US lost exports.

Finally, with the US an importer of gasoline from Europe, US gasoline prices would spike to curtail domestic demand, creating a negative hit to US economic activity.

Come to think of it, this is precisely what Biden will do next.