By Alasdair Macleod via GoldMoney.com. In recent years, America’s unsuccessful attempts at containing China as a rival hegemon has only served to promote Chinese antipathy against American capitalism. China is now retreating into the comfort of her long-established moral values, best described as a mixture of Confucianism and Marxism, while despising American individualism, its careless regard for family values, and encouragement of get-rich-quick financial speculation.

After America’s defeat in Afghanistan, the geopolitical issue is now Taiwan, where things are hotting up in the wake of the AUKUS agreement. Taiwan is important because it produces two-thirds of the world’s computer chips. Meanwhile, the large US banks are complacent concerning Taiwan, preferring to salivate at the money-making prospects of China’s $45 trillion financial services market.

The outcome of the Taiwan issue is likely to be decided by the evolution of economic factors. China is protecting herself against a global credit crisis by restraining its creation, while America is going full MMT. The outcome is likely to be a combined financial market and dollar crisis for America, taking down its Western epigones as well. China has protected herself by cornering the market for physical gold and secretly accumulating as much as 20,000-30,000 tonnes in national reserves.

If the dollar fails, which without a radical change in monetary policy it is set to do, with its gold-backing China expects to not only survive but be able to consolidate Taiwan into its territory with little or no opposition.

Introduction

On the one hand we have America and on the other we have China. As civilisations, America is discarding its moral values and social structures while China is determined to stick with its Confucian and Marxist roots. America is inclined to recognise no other civilisations as being civilised, while China’s leadership has seen America’s version and is rejecting it. Both forms of civilisation are being insular with respect to the other, and their need to peacefully cooperate in a multipolar world is increasingly hampered.

Understanding another nation’s point of view is essential for peaceful harmony. This truism has been ignored by not just America, but by the Western alliance under American coercion. The Federal Government and its agencies are pursuing a propaganda effort against China’s exports and technology, while the average American appears less troubled. Perhaps we can put this down to a nation based on immigrants having a more cosmopolitan psyche than its predominantly Anglo-Saxon establishment.

In Europe, it sometimes appears to be the other way round, with the politicians more prepared to tolerate China than their US counterparts. But then geography is involved, and the silk roads do not involve America, while rail links between China and Western Europe work efficiently, delivering vital trade between them.

Economic interdependency is rarely considered. Nor are the potential consequences of diverging economic and monetary policies. While China has been squeezing domestic credit, the West has been issuing currency and credit like drunken sailors on shore leave. Being starved of extra credit, China’s economy has been deliberately stalled, and there is a real or imagined crisis developing in its property markets. Only now, it has become apparent that the West’s major economies are running into troubles of their own.

Economic destabilisation heightens the risk of conflict, and perhaps the timing of the build-up of tensions in the South China Sea and over Taiwan is not accidental. On Wall Street there is an air of complacency, with the US investment community led by the big banks ignoring the developing risks of this dysfunction. In the context of deteriorating relations between China and America and with China’s growing contempt for US political resolve, Taiwan is becoming extremely important geopolitically.

China’s plans for Taiwan

Taiwan is in the world’s geopolitical crosshairs with President Xi insisting it returns to China. The West, which has failed to protect Taiwan from China’s claims of sovereignty in the past, thereby endorsing them, is only now belatedly coming to its aid with a new Pacific strategy. But the signals already sent to the Chinese are that the Western alliance is too divided, too weak to prevent a Chinese takeover. This surely is the reasoning behind China’s attempts to provoke an attack on its air force by invading Taiwan’s airspace. And all the West can do is indulge in finger-wagging by sailing aircraft carriers through the Taiwan Strait.

Taiwan matters, being the source of two-thirds of the world supply of microchips. Faced with a pusillanimous west, this fact hands great power to China — which with Taiwan corners the market. Furthermore, the big Wall Street banks are salivating over the prospects of participating in China’s $45 trillion financial services market and are preparing for it. China has thereby ensured the US banking system has too much invested to support the US administration in any escalation of the Taiwan issue.

The actual timing of China’s escalation of the Taiwan issue appears related to the AUKUS nuclear submarine deal. That being so, the posturing between China and the Western Alliance has just begun. There are four possible outcomes: China backs off and the tension subsides, America and the Western Alliance back off and China gets Taiwan, there is a negotiated settlement, or a military war against China ensues.

In this context it is important to understand the civilisation issue, which increasingly divides China and America. There is little doubt that the hitherto normal relationship between America and China was disrupted by President Trump becoming nationalistic. His “make America great again” policy was a declaration of a trade war. That was accompanied by a political attack on Hong Kong, which provoked China into taking Hong Kong under direct mainland control. There followed a technology war, leading to the arrest of the daughter of Huawei’s founder in Canada.

There appears to be little change in President Biden’s policy against China. Now that his administration has bedded in, China is beginning to test it over Taiwan. To give it context, we should understand the Chinese culture and why the state is so defensive of it, and how the leadership views America and its weaknesses. For that is what is behind its economic divergence from the West.

China’s changing political culture

Since becoming President, Xi has reformed China’s state machinery. After assuming power in 2012, he needed to clear out the corrupt and vested interests of the previous regime. He instigated Operation Fox Hunt against corrupt officials, who, it was estimated, had salted away the equivalent of over a trillion dollars abroad. By 2015 over 180 people had been returned to China from more than 40 countries. Former security chief Zhou Yongkang and former vice security minister Sun Lijun ended up in prison and Hu Jintao’s powerful Communist Youth League faction was marginalised.

By dealing ruthlessly with corrupt officials Xi got rid of the vested interests that would have potentially undermined him. He consolidated both his public support and his iron grip on the Communist Party for the decade ahead. His public approval ratings remain extraordinarily high to this day.

On the economic front Xi faced major challenges. Having become the world’s manufacturer, a sharp wealth divide opened between China’s concentrated manufacturing centres and rural China. Some 600 million people are still subsisting on a monthly income of less than 1,000 yuan ($156) a month. A rapidly increasing urban population has been denuding the rural economy of human resources and undermining the family culture.

The wealth disparity between city and country has become an important political issue, which is why as well as refocusing resources towards agriculture Xi has clamped down on super-rich entrepreneurs and their record-breaking IPOs. In his Common Prosperity policy, Xi declared that he was not prepared to let the gap between rich and poor widen, and that common prosperity was not just an economic issue but “a major political issue related to the party’s governing foundations”.

Following decades of communism under Mao, after China’s initial recovery and development Xi is now clamping down on unfettered capitalism. He and his advisers have observed the disintegration of family values in America and the rise of individualism at the expense of family life; and with popular culture how these trends are being adopted by China’s youth. The state has now shut down western-style social media, and erased celebrity culture.

The social impact of cultural change is often overlooked, but it is at the forefront of China’s policy-makers’ consideration. For millennia, a state-controlled Chinese civilisation endured. Despite the Cultural Revolution, the post-war Mao Zedong years failed to erase it. Never sympathetic to free markets, statist thoughts have turned inwardly to Confucius and Marx to escape the obvious failings of American capitalism and its decline from familial values to individualism and rampant speculation.

This is what Xi reflects in his presidency. His chief adviser, his éminence grise, is Wang Huning who operates in the political shadows. From all accounts, Wang is extremely clever, speaks French and English, spent a year in America and is a deep thinker who, having examined them, has rejected western values in favour of Chinese tradition. NS Lyons, an analyst and writer living in Washington, DC, has written an interesting article about Wang, published on Palladium Magazine — it is well worth reading.

As we saw with the UK’s temporary éminence grise, Dominic Cummings, the power to influence possessed by such a person is considerable, but always in a statist context. The economics of free markets are not involved, except as a source of revenue to fund statist ambitions. The result is an assumption, an ignorance of economic affairs concealed by an automatic acceptance of the status quo.

This is Wang’s weak point, and insofar as Xi relies on his advice, it is the President’s as well. Wang appears to be promoting a Confucian/Marxist hybrid civilisation which is intended to unify China’s many ethnic groups in a government-set culture, reverting to a morality of yesteryear. Comparing China’s future with that of American democracy and its moral degradation, the approach is understandable and enjoys popular support. But the consequences are that the state is drifting backwards towards its Marxist roots. The central command over the economy is exemplified in energy policy: power entities have been instructed to keep factories running without power outages, irrespective of coal and natural gas costs. In fact, the management of the economy was never relinquished by the state, which is now redoubling its efforts to retain control over economic outcomes.

All one can say is that so far, the Chinese appear to have made considerably less of a mess managing their economy and currency compared with America’s Federal Government and its central bank.

The political consequences are also important. By stemming the tide of Western moral decadence in her own territory China is insulating herself from the rest of the American-dominated world. This is being bolstered by steps to shift the emphasis from the export trade towards domestic consumption to improve living standards. In the process China will become more of an economic fortress, mainly interested in Africa and the Americas as sources of raw materials and commodities rather than as export markets to be fostered. China’s internationalism of the last four decades is increasingly redirected and confined to the Eurasian continent over which she exercises greater degrees of political and economic control. Which brings us back to the issues of Taiwan and the South China Sea, which China sees as consolidating her rightful political and cultural borders.

However, the increasing autarky of both China and America is making the Taiwan issue more difficult to resolve peacefully. And we must also consider the opposing directions of drift for their two economies, which could decide the outcome.

The US’s economic condition and outlook

There is a mistaken assumption that the US’s economic troubles relate solely to the consequences of the covid lockdowns. Certainly, the Fed timed its funds rate cut to the zero bound and its current and unprecedented rate of quantitative easing of $120bn every month to March 2020, when lockdowns in Europe and the UK commenced. And it was becoming clear, despite President Trump’s prevarication, that the US would follow.

But that ignores developments which preceded covid. Probably due to earlier tapering of QE in 2019, financial markets signalled a developing slump, with the S&P 500 falling 35% in 23 trading sessions to mid-March 2020 — eerily replicating the Wall Street Crash between end-September and late October 1929. It took the reduction of the Fed funds rate to the zero bound, and $120bn of monthly QE feeding into pension funds and insurance companies to turn markets higher. The yield on 10-year US Treasuries fell to 0.5% and equities markets soared on the back of a new basis of relative valuation.

After the repo blow-up in September 2019, it became clear that bank balance sheets were too constrained to extend additional bank credit, and conventionally, that might have marked the turn of the bank credit cycle, which was why the comparison with late-1929 was so apt. Furthermore, the banks became less interested in extending credit to Main Street than to Wall Street after financial markets stabilised.

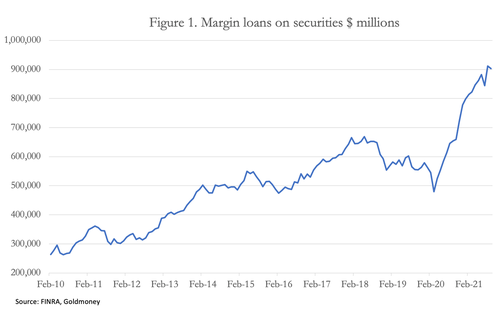

The recovery in equities and their move into new high ground is simply asset inflation. Speculators have been quick to add to the Fed’s QE liquidity by drawing on bank and shadow bank credit to play the game. Figure 1 shows how margin loans have nearly doubled as the bull market in equities proceeded from late-March 2020. Never has so much leverage been seen in US securities markets.

During covid lockdowns, beyond pure survival few in industry made judgements about the future. It was commonly assumed that when lockdowns ceased business would return to normal. But this made no allowance for the passage of time and the evolution of consumer needs and wants. Eighteen months later, we find that supply chains are still wrongfooted, disrupted by covid shutdowns and not supplying newly needed goods. Consumer demand patterns are not where they left off — they have radically changed.

Buoyancy in the US economy is now proving short-lived. The flood of initial spending following lockdowns has receded and different factors are now at play. Supply bottlenecks due to lack of components, transport, and labour are forcing up prices at a pace not reflected in official statistics.

In effect, GDP is insufficiently deflated by price rises on the high street to give a reasonable estimate of real GDP. With prices probably rising at over 15% annualised (Shadowstats.com estimated 13.5% three months ago and pressures on rising prices have increased significantly since) the US economy is in a slump which is beginning to replicate that of ninety years ago. The difference is that in 1930-33 the dollar was on a gold coin standard increasing its purchasing power as bank credit was withdrawn, while today it is pure fiat and declining at an increasing pace.

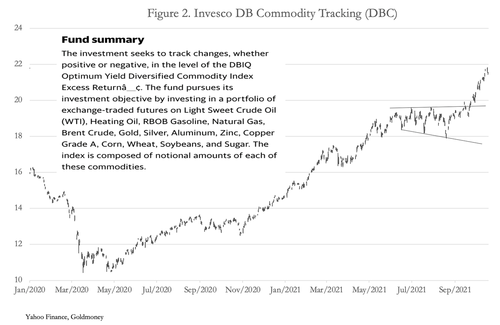

Rising prices across the board are another way of saying that the currency’s purchasing power is declining, which given the Fed’s monetary policies of recent years is not surprising. Figure 2 shows the impact of the Fed’s monetary policy on commodity prices, which reflects the dollar’s weakness as a medium of exchange.

Given that it takes anything between a few weeks and six months for energy and commodity prices to work through to consumer prices, the recent spurt in commodity prices strongly suggests that consumer prices are going to continue to rise into next year. Yet, only now are the Fed and other central banks beginning to accept that rising prices are not going to be as temporary as they first hoped. This is because it is not prices rising, but the dollar’s purchasing power falling. When they fully realise it, foreign holders of dollars, totalling $33 trillion held in securities, short-term instruments, and bank deposits will require higher interest compensation to persuade them to continue holding dollars. And this is where a conflicting problem arises.

A rise in interest rates sufficient to compensate foreign holders of dollars for the currency’s loss of purchasing power will undermine the values of their US stock holdings, totalling $14 trillion, of which $12 trillion is held by private sector foreign investors. Furthermore, a further $12.5 trillion of foreign private sector funds are invested in long-term bonds which will also decline in value. Higher interest rates will certainly trigger private sector selling of these assets across the board.

The fate of $6.6 trillion of foreign official holdings of long-term securities will be partly political, demonstrated by the most recent Treasury TIC figures which showed China selling $21bn of US Treasuries, and Japan and the UK buying $39bn between them. This is strongly suggestive of swap lines being drawn down to support the US Treasury bond market, while presumably the US, either through the Treasury, the Exchange Stabilisation Fund, or the Fed itself has bought JGBs and gilts as the quid pro quo.

It is worth noting this point because it shows how low bond yields are perpetuated by cooperation between major central banks – along with the attendant monetary inflation. That being the case, private sector holders are misled by price stability while bonds are being wildly overvalued.

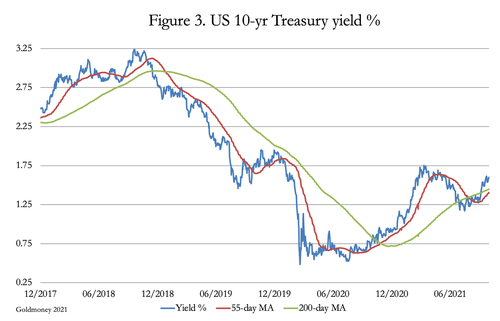

Another way of looking at it is that if John Williams at Shadowstats is right about inflation statistics, then US Treasuries should be yielding as much as 10% along the whole yield curve. Perhaps the recent rise in the 10-year US Treasury yield in Figure 2 is indicating the start of the process of this discovery for foreign and domestic investors alike.

The chart shows that once the 1.75% level is overcome, there is considerable upside in the yield, with a golden cross forming under the spot value. If yields rise from here, it will not be long before equity markets take note and enter a full-blown bear market.

The first reaction from the Fed to these events will almost certainly be to claim that falling equities are a leading economic indicator, suggesting the economy faces a post-covid recession. Interest rates cannot be eased further, but QE can be stepped up to cap bond yields and encourage pension funds and insurance corporations to increase their investments. This would be a U-turn from the projected policy of reducing QE due to inflation concerns. But at that point the neo-Keynesian argument can be expected to claim that the developing recession more than negates prospective inflation concerns.

Facing the same dynamics, the other leading central banks are certain to fall in line with the Fed’s new policy. But as John Law found in a similar situation in France in 1720, rigging a failing stock market (in his case the Mississippi venture) by currency and credit expansion ultimately fails and undermines the currency. Law destroyed the French economy, contrasting with the British South Sea Bubble, where the Bank of England was not involved and did not deploy its currency to ramp markets.

Today, it appears that Law’s experiment is about to be repeated on a grander scale by the issuer of the world’s reserve currency. The other major western central banks will follow suite. The whole fiat money system is at risk of being driven into a similar failure as that which faced the French livre. So, where would that leave China?

China’s economic and monetary outlook

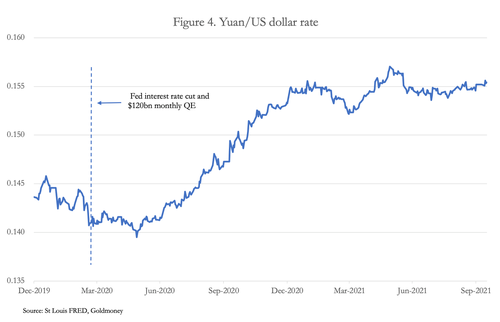

As noted above, China has followed a different monetary path from that of the Fed for some time — most pointedly since March 2020. Consequently, the yuan has risen against the dollar since then, illustrated in Figure 4.

After some initial uncertainty, the yuan began to rise against the dollar and is now about 10% up on the late-March 2020 level. This is not significant yet, because the dollar’s trade-weighted index has fallen by a similar amount. But with China’s monetary policy of clamping down on shadow banking and excessive bank credit creation, compared against the Fed’s more expansionary monetary policies, we can expect the trend for a stronger yuan relative to the dollar to continue.

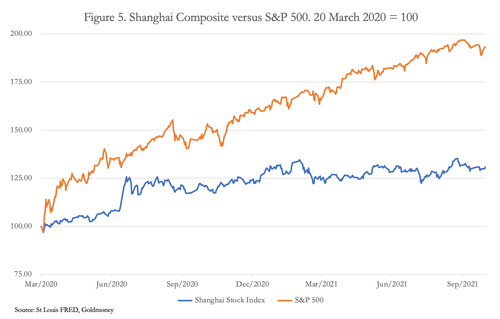

In neo-Keynesian language, China is in a period of deflation, leading to falling prices relative to those measured in dollars. But that misses the point: China has been careful not to encourage speculation in financial assets, reflected in relative stock market performances, shown in Figure 5.

While the Fed has been inflating stock prices through interest rate and monetary policies, the Chinese have discouraged speculation. The result is that financial assets in China should be less vulnerable to a general market downturn. It has been a deliberate policy to protect the Chinese economy from 2014 onwards, after the PLA’s chief strategist, Major-General Qiao Liang convinced Beijing that permitting unfettered speculation would leave markets vulnerable to a pump-and-dump attack by America.

To the Chinese, excessive financial speculation aided and abetted by the Fed must look like a cover for underlying economic failure. Every thread of their analysis must point to economic disintegration from which China must protect herself. Rates of credit expansion must be restricted, and the yuan be permitted to rise on the foreign exchanges. The change in policy emphasis from export markets towards increasing domestic consumption should be accelerated. In any event, China is the world’s dominant manufacturer, so she has a good degree of control over prices in international trade for consumer goods anyway. The prices of imported commodities and raw materials matter more today and rising dollar prices for commodities and energy can be countered by a higher exchange rate for the yuan.

The state’s policy of least risk is to quietly divorce the Chinese economy from the dollar’s influence. In switching some of its trade into the yuan and other currencies, it has been doing this since the Lehman failure, which was another seminal moment in Chinese thinking. The cultural analysis is that America is now destroying its own currency towards a terminal event, an outcome forecast by economics professors in China’s Marxist universities over fifty years ago. The post-Mao ride, piggybacking on American capitalistic methods, is no longer tenable.

The golden backstop

Like the Marxist professors in the universities, China’s thinkers, such as Wang Huning and President Xi himself, always believed America to be politically and morally rudderless and would destroy itself. Presumably the election of an unpredictable Trump followed by a President Biden who appears to be in a geriatric decline is seen in Beijing as evidence that American society is indeed rudderless and imploding.

It was against this likely event that in 1983 far-sighted Chinese strategists began to accumulate gold and to corner the word market for bullion. It would have been obvious to them that one day, dancing with the capitalist devils would become too dangerous and China’s future would have to be secured at the outset long before a capitalist collapse.

Accordingly, the Regulations on the Control of Gold and Silver were promulgated on 15 June that year, appointing the People’s Bank (PBOC) with sole responsibility for managing China’s gold and silver while private ownership remained banned. The PBOC then began to acquire gold from foreign markets, a task made easier by the 1980-2002 bear market. Meanwhile, the government threw substantial resources into developing gold mining, and became the largest gold producer in the world by a substantial margin, overtaking South Africa, Russia, and the United States. State owned refineries took in doré from abroad, adding to the accumulation.

It was only after the PBOC had accumulated sufficient bullion from imports and domestic production that she set up the Shanghai Gold Exchange in 2002 and permitted Chinese citizens to acquire gold. The government even ran advertising campaigns encouraging the purchase of gold, and since then, over 19,000 tonnes have been delivered into private sector ownership from the SGE’s vaults.

Together with the total ban on exports of Chinese refined gold, the pre-2002 ban on private ownership while the state acquired sufficient bullion for its purposes, coupled with the subsequent encouragement to the public to do the same, China clearly regarded gold as her most important strategic asset. It has still not shown its hand, but given the likely amounts involved, to do so would risk destabilising the dollar-centric fiat currency world. Until it happens, we should assume that the 20,000-30,000 tonnes likely to have been accumulated in various state accounts since 1983 is an insurance policy against the failure of American capitalism and the world’s reserve currency.

This brings us back to the Taiwan question. For China, the re-absorption of Taiwan may become a simpler matter when the capitalistic Americans are economically at their weakest and the dollar is collapsing. Taiwan itself might face up to this reality. A few steps to push America on its way may be tempting, such as selling down their holdings of US Treasuries (already in process) or disclosing a significantly higher level of gold reserves. The latter may wait until a dollar crisis really develops, which is now surely only a matter of a little time.