A trillion dollars is a lot of money. If you stacked a billion dollar bills on top of one another, the pile would be 67.9 miles high, but if you stacked a trillion dollar bills on top of one another the pile would be 67,866 miles high. And if you lined up a trillion dollar bills end to end, the line of dollar bills would be a staggering 96,906,656 miles long. That is longer than the distance from the Earth to the Sun.

A trillion dollars is such a vast amount of money that it is truly difficult to comprehend, but as you will see below, that much money has already been pulled out of “vulnerable” U.S. banks over the past year. Hordes of small and mid-size banks are now in trouble, and that is really bad news because those institutions issue most of the mortgages, auto loans and credit cards that our economy runs on.

The other day, I asked my readers to “imagine what our country will look like if the banking system implodes and the economy plunges into a depression”, because if our banks continue to collapse that is precisely where we are headed.

Unfortunately, the recent banking panic has greatly accelerated matters. In fact, a whopping 98.4 billion dollars was pulled out of U.S. banks during the week ending March 15th…

The readout, released shortly after the market closed Friday, came around the same time as new Fed data showed that bank customers collectively pulled $98.4 billion from accounts for the week ended March 15.

That would have covered the period when the sudden failures of Silicon Valley Bank and Signature Bank rocked the industry.

Just think about that.

Nearly 100 billion dollars in deposits evaporated in just one week.

And it turns out that small banks were being hit the hardest. Unsurprisingly, big banks actually saw enormous inflows…

Data show that the bulk of the money came from small banks. Large institutions saw deposits increase by $67 billion, while smaller banks saw outflows of $120 billion.

That article didn’t give numbers for mid-size banks, but it appears likely that they experienced large outflows as well.

Overall, JPMorgan Chase is telling us that the “most vulnerable” banks in this country have “lost a total of about $1 trillion in deposits since last year”…

JPMorgan Chase & Co analysts estimate that the “most vulnerable” U.S. banks are likely to have lost a total of about $1 trillion in deposits since last year, with half of the outflows occurring in March following the collapse of Silicon Valley Bank.

This really is a “banking meltdown”, and it has been going on for quite some time.

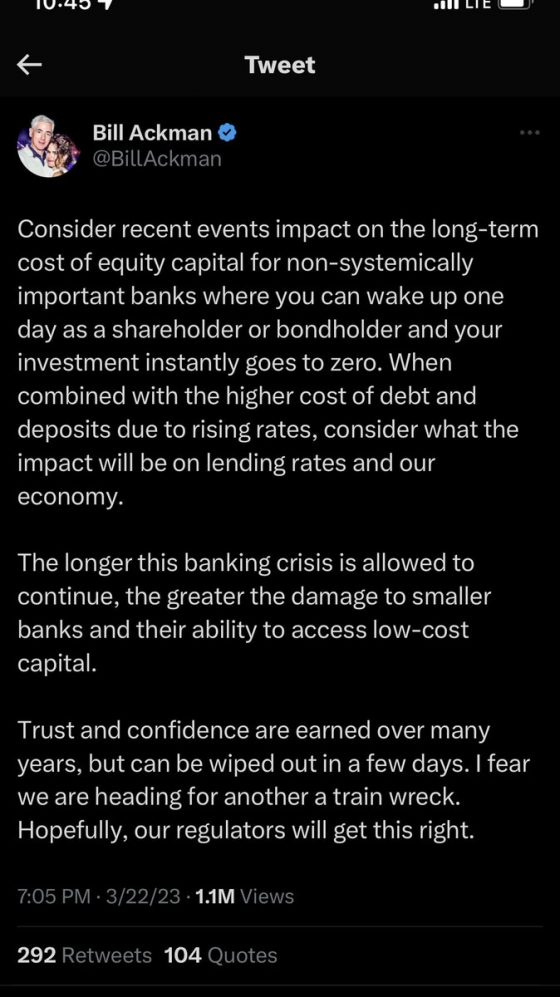

And as Bill Ackman has aptly noted, if something is not done our small and mid-size banks are headed for disaster.

There are more than 4,000 banks in the United States right now, and the vast majority of them are rapidly losing deposits.

As a result, U.S. banks are being forced to turn to the Fed for help at a very frightening rate…

Banks have been flocking to emergency lending facilities set up after the failures of SVB and Signature. Data released Thursday showed that institutions took a daily average of $116.1 billion of loans from the central bank’s discount window, the highest since the financial crisis, and have taken out $53.7 billion from the Bank Term Funding Program.

Meanwhile, the banking crisis in Europe has taken another very alarming turn.

On Friday, shares of Deutsche Bank plunged due to renewed concern about the stability of Germany’s biggest bank…

Deutsche Bank shares fell on Friday following a spike in credit default swaps Thursday night, as concerns about the stability of European banks persisted.

The Frankfurt-listed stock was down 14% at one point during the session but trimmed losses to close 8.6% lower on Friday afternoon.

The German lender’s Frankfurt-listed shares retreated for a third consecutive day and have now lost more than a fifth of their value so far this month.

It will be interesting to see if Credit Suisse or Deutsche Bank ends up going under first.

Of course the politicians continue to tell us that everything is just fine.

In fact, German Chancellor Olaf Scholz is insisting that there is “no reason to be concerned”…

German Chancellor Olaf Scholz said Friday that there was “no reason to be concerned” about Deutsche Bank.

“It’s a very profitable bank,” he told reporters in Brussels, where EU leaders issued a joint statement describing the European banking system as “resilient, with strong capital and liquidity positions.”

Deutsche Bank declined to comment.

Once upon a time we were told that Lehman Brothers would be just fine.

And earlier this month we were told that Silicon Valley Bank would be just fine.

As Robin Williams once observed, these banks love to make excuses.

https://twitter.com/defundnpr3/status/1639987730720382976

But it isn’t just a few isolated banks that are in trouble these days.

Right now the entire system is coming apart at the seams, and Steve Quayle is warning that things “will really kick into high gear in April”…

The word collapse is a great word, and the other word that comes with collapse is calamity. With the collapse and calamity under way, people think, well, as long as it doesn’t touch me, I’ll be okay or I’ll be dead, and my kids will have to deal with it. What a selfish way to deal with the Biblical times we live in. I think we are in big trouble with this banking situation that will really kick into high gear in April.

You may not have much sympathy for the banks, and I understand that.

But what is going to happen to our economy when the flow of mortgages, auto loans and credit cards is greatly restricted?

Our country is already being torn to shreds like a 20 dollar suit, and economic conditions are still relatively stable.

So what is going to happen when we do fall into a very deep economic depression?

These are such perilous times, and they are only going to get more difficult in the months ahead.

By Michael Snyder