Basel III Regulations Finally Kick In: What This Means For Gold

On Monday, the long-anticipated (by gold bulls) banking rules implemented under a sweeping international accord known as Basel III came into effect (for European banks) and – as discussed previously both here and elsewhere – mark a major change for European banks and their dealings with gold, “potentially altering the landscape for precious metal demand and prices” as MW puts it.

In a nutshell, Basel III elevates allocated gold, in tangible form, to be classified as a zero-risk asset under the new rules, but unallocated – or the hated by gold purists – “paper” gold, which banks typically deal with the most often, won’t — meaning banks holding paper gold must also hold extra reserves against it. The new liquidity requirements aim to “prevent dealers and banks from simply saying they have the gold, or having more than one owner for the gold they have” on the balance sheet.

A little background: the Basel Committee on Banking Supervision, which sets standards for regulation of banks, developed what is called Basel III in response to the global financial crisis. As such, Basel III was envisioned as a multiyear regime change that aims to prevent another global banking crisis, by requiring banks to hold more stable assets and fewer ones deemed risky. The rule overhaul is defined by the Bank for International Settlements, also known as the central banks’ central bank, as an internationally agreed set of measures that aim to strengthen bank regulation, supervision and risk management.

While there are many nuances, what is relevant to gold is that under the new regime, physical, or allocated, gold, like bars and coins, will be reclassified from a tier 3 asset, the riskiest asset class, to a tier 1 zero-risk weight, putting it “right alongside with cash and currencies as an asset class,” said Adam Koos, president of Libertas Wealth Management Group.

For the newbies in the gold space, allocated gold is metal owned directly by an investor, in physical form, such as coins or bars without liens, claims or any rehypothecation chains of ownership on it. Unallocated gold, or paper contracts, on the other hand is often owned by banks, but investors are entitled to that gold, and avoid storage and delivery fees. Unallocated gold is widely despised by purists in the gold community as it represent potentially countless claims on the same metal, while the metal itself may be in an entirely different location.

Bank of America has a more colorful explanation:

If the gold is held in allocated form, a specific bar is attributed to the client. The bank effectively acts as a custodian, with the precious m etal held off balance sheet. This also means that banks cannot access the gold for their own business activities.

If customers of a bank hold gold in an unallocated account, they essentially are an unsecured creditor. Gold held in unallocated accounts, similar to currency deposited, can be used by banks for their normal conduct of business. As such, unallocated gold is fungible and can be used to clear and settle physical metal transactions. Because of this, it provides the liquidity essential for the clearing and settlement system (similar to fiat money which is frequently rehypothecated hudnreds of times among its various claimants in a fractional reserve system). The LBMA points out that this allows clearing banks to debit/credit market participants’ accounts with metal immediately, even before the seller’s metal is delivered to the buyer. [That’s because there is no actual gold being moved around, just promises of said gold]

It goes without saying that the obvious reason why gold bugs have been salivating at today’s transition is that since going forward physical gold will have a risk-free status, Basel III could cause banks around the world to continue to buy more, Koos said, adding that central banks already have stepped up purchases of physical gold to be held in the institutions’ vaults, and not held in unallocated, or paper form. Inversely, under the new rules paper gold would be classified as more risky than physical gold, and no longer counted as an asset equal to gold bars or coins.

* * *

As part of the Basel III regulations, MW notes that European banks will also face new liquidity requirements, known as the Net Stable Funding Ratio (NSFR). It’s a liquidity standard that banks must follow to ensure adequate stable funding to cover their long-term assets. The ratio is the amount of available stable funding relative to the amount of required stable funding, which should be equal to at least 100% on an ongoing basis. NSFR regulations will be introduced to banks in the European Union on Monday, the U.S. on July 1, and in the U.K. on Jan. 1, 2022, according to Alasdair Macleod, head of research at Goldmoney Inc.

“It affects all bank liabilities and assets” and the objective is to ensure that bank assets are “properly funded and that depositor withdrawals will not lead to bank insolvency and the transmission of systemic risk,” said Macleod.

The objective of the NSFR is “oblige banks to finance long-term assets with long-term money” to avoid liquidity failures that were seen during the 2007/2008 global financial crisis, according to the London Bullion Market Association (LBMA).

According to analysts, the new rules will mainly impact banks and their unallocated gold, as the majority of regular investors tend to hold physical, allocated gold. However, in a world where banks are the marginal price setters, any rotation out of a paper and into true physical gold – which is far more scarce – could have vast implications on price.

Meanwhile, in a note from BofA on monday, the bank’s analysts wrote that the new liquidity ratio requirements imply that banks may “need to set aside more funding for ‘unallocated’ gold.” BofA adds that rising funding requirements for unallocated gold means that financial institutions

Raising funding requirements for unallocated gold means the financial institution would either “reduce the bullion business” or “sustain activity and put more funding aside,” said analysts at BofA.

Those two options have slightly different implications for the gold market, “ranging from a reduction in liquidity to rising costs for market participants,” the analysts said. Either way, they do not believe these dynamics are bullish for gold, predicting that Basel 3 in itself won’t “push prices higher outright.” Also, it’s “unlikely that banks would replace usage of unallocated gold by gold purchased outright.”

So with Basel III frowning on allocated gold, why have banks dealt primarily with unallocated gold in the past? Two reasons: i) availability (in many ways, one can “create” unallocated gold with a simple signature and ii) it makes trading the metal easier.

Unallocated gold “provides the most convenient, cheapest and…effective way for trades to be done between professional counterparts, rather than having to move physical bars against each trade,” said Ross Norman, chief executive officer at Metals Daily. It’s primarily an “interbank mechanism” to help professional participants with clearing and settlement of trades.

Under the NSFR rules, however, “unallocated gold goes into the balance sheet of the banks involved” and the rules “propose to make it much more expensive for banks to hold unallocated gold balances,” Norman added, explaining that the new rules will not only “make the cost of clearing and settling trades more expensive, but the lending of precious metals to industrial counterparts, including miners, refiners and fabricators will become much more expensive as the costs get pushed down the value chain.”

It follows that the “proposed changes will make dealing in gold much more expensive for everyone in the sector,” even those acquiring physical bars, and it could make the market smaller, Norman said. All in all, he views that changes as “retrograde” and may “render gold less relevant as an investible asset.” Most gold bulls disagree with him, and note that if he is right, it is only because there is vastly less gold in the system than banks represent suggesting that if gold were to be uncollateralized, its price would have to soar as demand for allocated, physical gold would be far greater than supply.

If a physical gold broker’s cost of financing his stock of coins and bars, for example, doubles, then it’s likely he’ll hold less inventory, and charge higher premiums for his products, Norman said. “If financial markets become stressed and gold demand rises sharply, then physical supply would be greatly constrained – “you have just burned half of your lifeboats.” In turn, that would make gold less attractive as a safe haven, he said.

In a recent letter on the impact of the NSFR on the precious metals market, the LBMA and World Gold Council said the proposals under the NSFR “fail to take into account the damaging effect that the rules will have on the precious metals clearing and settlement system, potentially undermining the system completely, and on the increased costs of financing of precious metals production.”

It is easy to trace the LBMA’s concern: having manipulated the gold market for years (see “London Gold Vault Bait-And-Switch As LBMA Prepares Bigger Changes“) many allege that the LBMA’s sole role is to mask the fact that there is much less physical gold that banks and sovereign states represent, a claim which has been validated by the repatriation of gold by countries such as Germany and Austria.

There is another reason why the LBMA has been staunchly against Basel III: the majority of precious metals held by the London Precious Metals Clearing Limited, which was created by the LBMA and operates the clearing and settlement for precious metals transactions, is unallocated metal.

The vast majority of gold trading takes place in the London bullion market, said Gold Newsletter’s Lundin. The regulations are expected to take hold in the U.K. at the start of the new year, so the “real impact won’t be seen this month.”

* * *

But while there is broad agreement on what Basel III means for banks, analysts differ greatly when it comes to their options on the impact of Basel III and its NSFR requirements on the gold market.

Goldmoney’s Macleod expects banks to be “discouraged” from dealings in gold forward contracts in London and in futures contracts on Comex. That can lead to “greater price volatility and at the margin, some bank customers who have had unallocated gold and silver accounts will seek to maintain their exposure by buying physical bullion.”

These new changes also come at a time of accelerated monetary inflation and it’s “very likely” that the combination of the two events “will drive price higher,” Macleod said. How much higher depends on how weak the dollar becomes in terms of its purchasing power, he said.

Norman, on the other hand, thinks the new rules will “not have any significant effect on gold prices…only on the cost of dealings in these markets.”

But Gold Newsletter’s Lundin explains it best: “The range of opinions on the matter extend from no effect on one side, to absolute mayhem on the other, peppered…with a ‘believe it when I see it’ attitude.”

And then there is the risk that none of this actually happens: Lundin cautioned that since the implementation of the Basel III rules has been postponed so many times, there’s still lingering doubt it’s going to actually happen. Lundin also said he does not believe the bullion market and central banks would allow these regulations to interfere with the system they have set up, but he holds out hopes that they will.

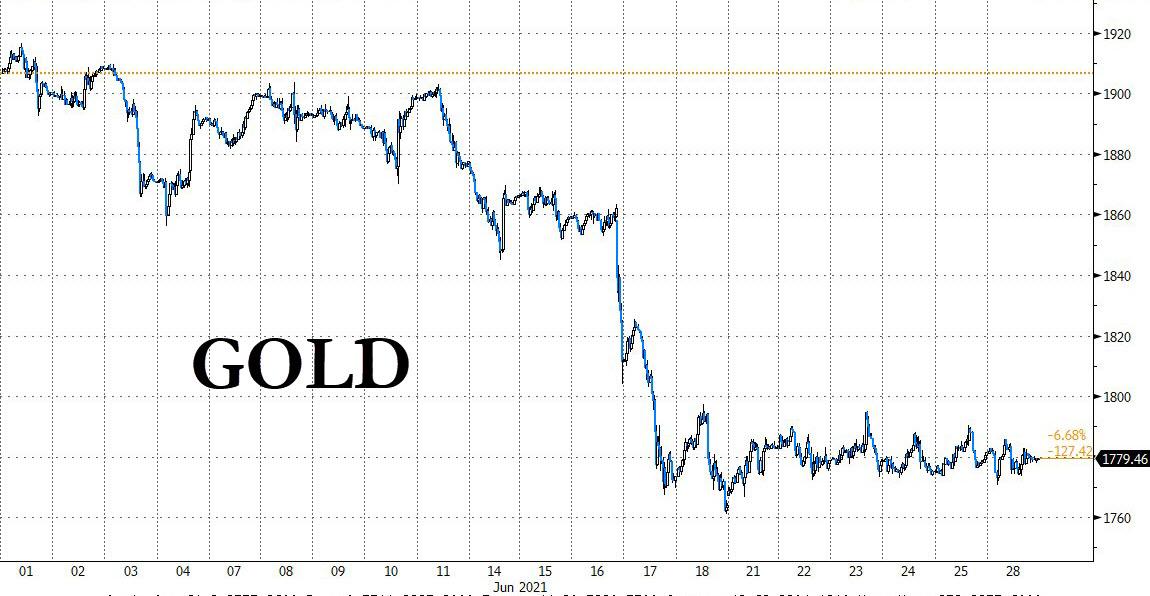

Finally, for those looking at price as a guide, today was a letdown: the historic rollout of Basel III saw gold barely move, closing down 0.1% after trading in a narrow – and lower – range ever since the hawkish FOMC meeting.

Tyler Durden

Mon, 06/28/2021 – 17:50

Basel III Regulations Finally Kick In: What This Means For Gold

On Monday, the long-anticipated (by gold bulls) banking rules implemented under a sweeping international accord known as Basel III came into effect (for European banks) and – as discussed previously both here and elsewhere – mark a major change for European banks and their dealings with gold, “potentially altering the landscape for precious metal demand and prices” as MW puts it.

In a nutshell, Basel III elevates allocated gold, in tangible form, to be classified as a zero-risk asset under the new rules, but unallocated – or the hated by gold purists – “paper” gold, which banks typically deal with the most often, won’t — meaning banks holding paper gold must also hold extra reserves against it. The new liquidity requirements aim to “prevent dealers and banks from simply saying they have the gold, or having more than one owner for the gold they have” on the balance sheet.

A little background: the Basel Committee on Banking Supervision, which sets standards for regulation of banks, developed what is called Basel III in response to the global financial crisis. As such, Basel III was envisioned as a multiyear regime change that aims to prevent another global banking crisis, by requiring banks to hold more stable assets and fewer ones deemed risky. The rule overhaul is defined by the Bank for International Settlements, also known as the central banks’ central bank, as an internationally agreed set of measures that aim to strengthen bank regulation, supervision and risk management.

While there are many nuances, what is relevant to gold is that under the new regime, physical, or allocated, gold, like bars and coins, will be reclassified from a tier 3 asset, the riskiest asset class, to a tier 1 zero-risk weight, putting it “right alongside with cash and currencies as an asset class,” said Adam Koos, president of Libertas Wealth Management Group.

For the newbies in the gold space, allocated gold is metal owned directly by an investor, in physical form, such as coins or bars without liens, claims or any rehypothecation chains of ownership on it. Unallocated gold, or paper contracts, on the other hand is often owned by banks, but investors are entitled to that gold, and avoid storage and delivery fees. Unallocated gold is widely despised by purists in the gold community as it represent potentially countless claims on the same metal, while the metal itself may be in an entirely different location.

Bank of America has a more colorful explanation:

If the gold is held in allocated form, a specific bar is attributed to the client. The bank effectively acts as a custodian, with the precious m etal held off balance sheet. This also means that banks cannot access the gold for their own business activities.

If customers of a bank hold gold in an unallocated account, they essentially are an unsecured creditor. Gold held in unallocated accounts, similar to currency deposited, can be used by banks for their normal conduct of business. As such, unallocated gold is fungible and can be used to clear and settle physical metal transactions. Because of this, it provides the liquidity essential for the clearing and settlement system (similar to fiat money which is frequently rehypothecated hudnreds of times among its various claimants in a fractional reserve system). The LBMA points out that this allows clearing banks to debit/credit market participants’ accounts with metal immediately, even before the seller’s metal is delivered to the buyer. [That’s because there is no actual gold being moved around, just promises of said gold]

It goes without saying that the obvious reason why gold bugs have been salivating at today’s transition is that since going forward physical gold will have a risk-free status, Basel III could cause banks around the world to continue to buy more, Koos said, adding that central banks already have stepped up purchases of physical gold to be held in the institutions’ vaults, and not held in unallocated, or paper form. Inversely, under the new rules paper gold would be classified as more risky than physical gold, and no longer counted as an asset equal to gold bars or coins.

* * *

As part of the Basel III regulations, MW notes that European banks will also face new liquidity requirements, known as the Net Stable Funding Ratio (NSFR). It’s a liquidity standard that banks must follow to ensure adequate stable funding to cover their long-term assets. The ratio is the amount of available stable funding relative to the amount of required stable funding, which should be equal to at least 100% on an ongoing basis. NSFR regulations will be introduced to banks in the European Union on Monday, the U.S. on July 1, and in the U.K. on Jan. 1, 2022, according to Alasdair Macleod, head of research at Goldmoney Inc.

“It affects all bank liabilities and assets” and the objective is to ensure that bank assets are “properly funded and that depositor withdrawals will not lead to bank insolvency and the transmission of systemic risk,” said Macleod.

The objective of the NSFR is “oblige banks to finance long-term assets with long-term money” to avoid liquidity failures that were seen during the 2007/2008 global financial crisis, according to the London Bullion Market Association (LBMA).

According to analysts, the new rules will mainly impact banks and their unallocated gold, as the majority of regular investors tend to hold physical, allocated gold. However, in a world where banks are the marginal price setters, any rotation out of a paper and into true physical gold – which is far more scarce – could have vast implications on price.

Meanwhile, in a note from BofA on monday, the bank’s analysts wrote that the new liquidity ratio requirements imply that banks may “need to set aside more funding for ‘unallocated’ gold.” BofA adds that rising funding requirements for unallocated gold means that financial institutions

Raising funding requirements for unallocated gold means the financial institution would either “reduce the bullion business” or “sustain activity and put more funding aside,” said analysts at BofA.

Those two options have slightly different implications for the gold market, “ranging from a reduction in liquidity to rising costs for market participants,” the analysts said. Either way, they do not believe these dynamics are bullish for gold, predicting that Basel 3 in itself won’t “push prices higher outright.” Also, it’s “unlikely that banks would replace usage of unallocated gold by gold purchased outright.”

So with Basel III frowning on allocated gold, why have banks dealt primarily with unallocated gold in the past? Two reasons: i) availability (in many ways, one can “create” unallocated gold with a simple signature and ii) it makes trading the metal easier.

Unallocated gold “provides the most convenient, cheapest and…effective way for trades to be done between professional counterparts, rather than having to move physical bars against each trade,” said Ross Norman, chief executive officer at Metals Daily. It’s primarily an “interbank mechanism” to help professional participants with clearing and settlement of trades.

Under the NSFR rules, however, “unallocated gold goes into the balance sheet of the banks involved” and the rules “propose to make it much more expensive for banks to hold unallocated gold balances,” Norman added, explaining that the new rules will not only “make the cost of clearing and settling trades more expensive, but the lending of precious metals to industrial counterparts, including miners, refiners and fabricators will become much more expensive as the costs get pushed down the value chain.”

It follows that the “proposed changes will make dealing in gold much more expensive for everyone in the sector,” even those acquiring physical bars, and it could make the market smaller, Norman said. All in all, he views that changes as “retrograde” and may “render gold less relevant as an investible asset.” Most gold bulls disagree with him, and note that if he is right, it is only because there is vastly less gold in the system than banks represent suggesting that if gold were to be uncollateralized, its price would have to soar as demand for allocated, physical gold would be far greater than supply.

If a physical gold broker’s cost of financing his stock of coins and bars, for example, doubles, then it’s likely he’ll hold less inventory, and charge higher premiums for his products, Norman said. “If financial markets become stressed and gold demand rises sharply, then physical supply would be greatly constrained – “you have just burned half of your lifeboats.” In turn, that would make gold less attractive as a safe haven, he said.

In a recent letter on the impact of the NSFR on the precious metals market, the LBMA and World Gold Council said the proposals under the NSFR “fail to take into account the damaging effect that the rules will have on the precious metals clearing and settlement system, potentially undermining the system completely, and on the increased costs of financing of precious metals production.”

It is easy to trace the LBMA’s concern: having manipulated the gold market for years (see “London Gold Vault Bait-And-Switch As LBMA Prepares Bigger Changes”) many allege that the LBMA’s sole role is to mask the fact that there is much less physical gold that banks and sovereign states represent, a claim which has been validated by the repatriation of gold by countries such as Germany and Austria.

There is another reason why the LBMA has been staunchly against Basel III: the majority of precious metals held by the London Precious Metals Clearing Limited, which was created by the LBMA and operates the clearing and settlement for precious metals transactions, is unallocated metal.

The vast majority of gold trading takes place in the London bullion market, said Gold Newsletter’s Lundin. The regulations are expected to take hold in the U.K. at the start of the new year, so the “real impact won’t be seen this month.”

* * *

But while there is broad agreement on what Basel III means for banks, analysts differ greatly when it comes to their options on the impact of Basel III and its NSFR requirements on the gold market.

Goldmoney’s Macleod expects banks to be “discouraged” from dealings in gold forward contracts in London and in futures contracts on Comex. That can lead to “greater price volatility and at the margin, some bank customers who have had unallocated gold and silver accounts will seek to maintain their exposure by buying physical bullion.”

These new changes also come at a time of accelerated monetary inflation and it’s “very likely” that the combination of the two events “will drive price higher,” Macleod said. How much higher depends on how weak the dollar becomes in terms of its purchasing power, he said.

Norman, on the other hand, thinks the new rules will “not have any significant effect on gold prices…only on the cost of dealings in these markets.”

But Gold Newsletter’s Lundin explains it best: “The range of opinions on the matter extend from no effect on one side, to absolute mayhem on the other, peppered…with a ‘believe it when I see it’ attitude.”

And then there is the risk that none of this actually happens: Lundin cautioned that since the implementation of the Basel III rules has been postponed so many times, there’s still lingering doubt it’s going to actually happen. Lundin also said he does not believe the bullion market and central banks would allow these regulations to interfere with the system they have set up, but he holds out hopes that they will.

Finally, for those looking at price as a guide, today was a letdown: the historic rollout of Basel III saw gold barely move, closing down 0.1% after trading in a narrow – and lower – range ever since the hawkish FOMC meeting.

Tyler Durden

Mon, 06/28/2021 – 17:50

Read More

{kind=link}

{kind=link}

{kind=link}