Basel III & The New Role For Gold

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

Last week both Martin Armstrong and Alistair MacLeod wrote about the changes to the Basel III rules and how they will greatly affect the physical and paper gold markets if implemented in their current form.

MacLeod’s article from last week is an excellent primer on the definitions and inner workings of the rules, the gold market and the changes to the rules. The short redux is that the advantage to using unallocated accounts, savings accounts which are linked to gold by holding futures contracts, will end.

We’ve discussed parts of this in the past. The process of creating fake supply to control the price of gold is on the line with these rule changes.

These rules are coming at the end of June for the European Banking System which will adopt the new Basel III rules. In short, the incentive to have exposure to gold as a pile of credit will go away if the banks can’t use any of that as part of their reserve calculations for their ASF – Available Stable Fundings.

Moreover, any physical gold they hold will be held at a 15% discount. Bottom line: these rules will make it impossible for the LBMA member banks to hold any exposure to unallocated pools of gold derviatives –futures and swaps — on their balance sheets.

It will force a liquidation of those positions and end any fractional reserve leveraging of gold used to suppress the price. There will still be futures markets but the whole of the gold trade will collapse back to simply coordinating supplies of gold from producers to consumers through time, like any other commodity market.

In effect, Basel III, if implemented in its current form, would change the gold market from a speculative one based on perceptions of the efficacy of monetary policy to control real interest rates to one that should force price discovery in an almost purely physical market. As I told my Patrons in May 16th’s Market Report video, physical gold will go from being the price taker to the price maker.

And the Free Gold contingency, of which MacLeod is one, will claim victory here. These are the people who have contended for years that once the leverage in the monetary system became so big it would collapse the paper gold market as it went bidless and everyone demanded physical.

In a way they argue the same end to the current system as Murray Rothbard predicted how Bretton Woods would end when someone — France under De Gaulle — would drain the U.S. Treasury of its gold if they believed the U.S. printed more dollars than could support a peg to $35/ounce.

I sense from reading MacLeod’s last two articles, he is doing his best to contain his optimism and exuberance. Now, this week’s article from him goes into some speculation as to why this is happening. And I think he’s avoiding the real issues.

MacLeod’s avoiding the elephant in the room in the same way that Martin Armstrong last week berated the BIS for these rules knee-jerk reacting to them as more evidence of regulator incompetence, not giving much credence that it may be part of a wider strategy.

To Armstrong’s immense credit he did warn us of this in 2019, stating that Basel III’s requirements would create the very liquidity crisis we’ve been inching towards since the blowout of SOFR in September 2019, which resulted in the market spasm I call the Coronapocalypse last March once the heroin wore off and the flood of liquidity created by the Fed since then to keep the financial system alive, if on life support.

But the cliff edge of Basel III is now right in front of us, if reports are true.

To me this situation begs a number of obvious questions.

And the first is, Why Now?

We’ve been discussing these changes vis a vis Basel III for more than five years. So, why, all of a sudden is Europe so hot to implement them in June and for the U.K. to adopt them in January 2022, knowing full well that this will end the bullion banks and the central banks’ program of controlling the rise in gold prices through the application of newly-printed money to create fake supply and allow nearly infinite leverage in the gold market relative to unencumbered physical supply.

MacLeod goes through the math in this week’s article speculating as to what the real available supply of gold is versus the stated available supply. It’s vanishingly small if you assume, like he does, that both China and Russia vastly understate their gold holdings, which is a good assumption.

In October 2014 I published an article explaining why China had considerably more gold in storage than her declared reserves, and I estimated that by 2002, when the Chinese government removed the ban on personal ownership and opened the Shanghai Gold Exchange, the state could have acquired up to 25,000 tonnes. Much of this gold would have been leased gold sold into the London market …

That China had accumulated substantial undeclared bullion stocks was confirmed to me anecdotally by experienced China watchers. If we treat that as part of our estimate of monetary gold, and make an allowance for Russia, of perhaps an unrecorded 5,000 tonnes, monetary gold in the hands of everyone else appears to amount to only 15,000 tonnes.

So, again, why this, why now if suppressing gold is such a useful tool for continued faith in the central banks? Well, MacLeod gets about halfway there in my opinion.

Another popular theory is of an even wider financial reset. The BIS is coordinating research into central bank digital currencies, which if adopted cuts out the commercial banks altogether. In theory, it would allow central banks to more effectively target stimulus and do away with the destabilising cycle of bank credit. The ultimate aim could be to demote and then remove commercial banks from the financial system entirely, in which context the closure of derivative markets by regulatory means makes some sense.

That is the final act of the story not the beginning of it.

First you have to get through the crisis this would engender with the Central Banks 1) retaining some of the people’s faith they are competent and 2) they don’t go bankrupt in the process.

Now, because of its structure, the Fed can’t go bankrupt. It can print unlimited amounts of credit and ‘elastic money,’ as Martin Armstrong terms it to cover any and all time-mismatches within the banking system. That has been proven to be correct multiple times over the past 13 years since Lehman Bros. collapsed.

The ECB, on the other hand, can go bankrupt, since it has no capacity to do this. All it can do is buy the sovereign debt of the member countries’ central banks and hand them back euros, while swapping around deckchairs on this monetary Titanic. There is a definable limit to this process, especially if rates rise as people lose confidence in the underlying economic activity of those countries and their fiscal positions.

This is absolutely underway, and it isn’t like this is happening on the periphery of Europe. It’s happening in the core countries, like France and Germany. This is why I keep harping on the rise in the German 10 year bund, up nearly 60 basis points since the beginning of the year, despite Lagarde’s heroic efforts.

In March ECB President Christine Lagarde panicked and doubled the rate of bond buying within the Euro-zone by the ECB to keep rates under control. She has failed. The market woke up to the fact that she’s a lawyer not a central banker.

This week the ECB made the statement that there are ‘elevated financial stability risks’ because of a a high stock market. It was their ‘irrational exuberance’ statement. But it’s really an admission that the entire system is melting down and they have no more capacity to keep it under control.

Translation: The Banking System is Fucked and I don’t have any answers. https://t.co/35SZFC9lHM

— Tom Luongo (@TFL1728) May 21, 2021

Lagarde increasingly looks like someone overmatched for her job from a money professional’s perspective. But from the political vandalism perspective, as practiced by her real boss, Klaus Schwab of the World Economic Forum, she’s doing a bang up job screwing everything up.

Moreover, if you also are coordinating with the Bank of International Settlements and are manipulating events to transfer power from individual countries to the IMF and *shudder* the United Nations, it’s important that the institutions you have the most control over remain solvent and stand ready to offer a solution out of the incipient crisis.

That means, as a truly trapped ECB presiding over a banking system that has reached its terminal limit who is also sitting on trillions in deteriorating sovereign debt, what can you do to shore up your balance sheet at that point?

The answer is simple, the one thing the Fed cannot do, allow the price of gold to rise.

What?!

Yes.

The ECB has under its control roughly 10,000 tonnes of gold. It marks that gold to market. It’s worth at $1881 an ounce around $605 billion. The Fed, on the other hand, holds its gold, the 8133.5 tonnes it bought from the U.S. Treasury, on its balance sheet at the price it paid, $42.22 per ounce. It has a balance sheet entry of $11.04 billion

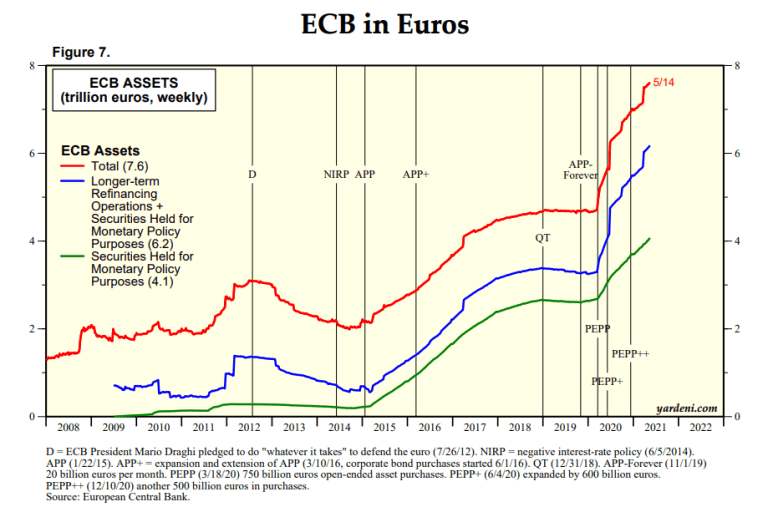

The problem is the ECB has around €6 trillion (or around $7.2 trillion at $1.21 EUR/USD) in securities on its balance sheet which are now falling in value with rising yields that Lagarde’s QE programs of various flavors cannot contain.

https://www.yardeni.com/pub/balsheetwk.pdf

The Fed has the problem of rising inflation and real yields now running -3%. Moreover, they can’t taper QE or raise rates until they are done cutting the commercial banks out of the transmission system for dollar liquidity first. Chris Whalen’s latest article on Zerohedge has the details of what’s going on at the Marriner-Eccles building.

…the FOMC is going to make permanent the RRPs (reverse-repos), essentially accepting the proposal by the Federal Reserve Bank of St Louis to create a standing repo facility for banks and nonbanks alike. This means that funds, REITs and especially smaller dealers are going to be able to go direct to the Fed of New York and finance collateral, breaking the monopoly control of the big primary dealer banks. H/T to George Selgin at Cato Institute.

Like Basel III’s changes to funding ratios, the FOMC opening up its repo and credit facilities to non-banks, REITs and anyone with a pulse, means there are big changes in store for the big commercial banks who have been running roughshod over the financial landscape for decades.

But, back to the ECB. It should be obvious now where I’m goin with this. In order for the ECB to avoid bankruptcy in the coming sovereign debt crisis, which in many ways The Davos Crowd is engineering, the price of gold will have to rise in euro-terms to offset the losses as that debt goes bidless. When that happens amidst the panic, the ECB will offer George Soros’ preferred option to investors, perpetual bonds.

The old debt will be cancelled and reissued as perpetual debt. But to pull that off the ECB will officially take control over the gold reserves of the euro-zone completely, while gold rises, putting the Fed behind the eight ball having lost the battle against commodity inflation.

So, implement Basel III, crush the incentive structure of the paper gold trade and allow real price discovery to fuel an historic rise in the price of gold. If the commercial banks in London and New York fight this they will be outcompeted and their balance sheets degraded.

Let’s take this one step further and go back to my original question. Why Now?

Simple, the private markets are beginning to realize what’s happening. The commercial banks are embracing crypto to keep their clients from bolting. There are fissures forming, as I talked about last week between the central banks and the commercial money center banks.

But, the big one, timing-wise, is the emergence of a potential parallel monetary system is threatening to capture the imagination of a generation who:

Hate the commercial banks because of the last 13 years of financial repression.

Want something tied to a real asset or at least a non-fake one of infinite supply.

Firmly distrust the existing power structure and have voted that way consistently over the past decade of Western elections.

Like bitcoin or hate it, the latest rally was deeply embarrassing to everyone who’s been skimming the cream off society via the monopolistic monetary system. Their lies were laid bare for all of us to see.

It doesn’t surprise me at all that this week was the week chosen to do the hatchet job on crypto. It was also the week where the plumbing of the financial markets became so thoroughly clogged (see Whalen’s article above) that there was no choice but to demoralize the rubes who thought they would escape the Great Reset.

Everyone must be liquidated to make the world safe for German eugenicists and commies.

So, Basel III is coming to destroy the paper gold markets and destroy the money center banks in New York and London while setting the stage to bail out the euro-zone. Higher gold prices are the answer to all of these things. Think of it this way, in a world where debt assets are failing and new private forms of custodial assets are rising in mindshare, what’s the only real weapon the central banks have to maintain credibility?

Their gold reserves.

How do you, if you are the ECB, use that weapon simultaneously against your two main competitors, the commercial banking interests in New York and London and the nascent crypto anarchists? You deploy your gold and steal everyone’s thunder.

In the end the Free Gold community will get what they want, but not for the reasons they ever thought they would — a bidless paper gold market and true price discovery in gold. What they won’t ever get is the next step, the re-monetization of gold, unless enough people see this power play for what it is and start making the appropriate moves now, which includes getting off your high horse about crypto.

So, if you are looking for these new Basel III rules to be put off again, you are most likely going to wind up on the wrong side of the trade and be just more grist for Schwab’s mill.

* * *

Join my Patreon if you can think in more than two dimensions

Donate via

BTC: 3GSkAe8PhENyMWQb7orjtnJK9VX8mMf7Zf

BCH: qq9pvwq26d8fjfk0f6k5mmnn09vzkmeh3sffxd6ryt

DCR: DsV2x4kJ4gWCPSpHmS4czbLz2fJNqms78oE

LTC: MWWdCHbMmn1yuyMSZX55ENJnQo8DXCFg5k

DASH: XjWQKXJuxYzaNV6WMC4zhuQ43uBw8mN4Va

WAVES: 3PF58yzAghxPJad5rM44ZpH5fUZJug4kBSa

ETH: 0x1dd2e6cddb02e3839700b33e9dd45859344c9edc

Tyler Durden

Sun, 05/23/2021 – 15:30

Basel III & The New Role For Gold

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

Last week both Martin Armstrong and Alistair MacLeod wrote about the changes to the Basel III rules and how they will greatly affect the physical and paper gold markets if implemented in their current form.

MacLeod’s article from last week is an excellent primer on the definitions and inner workings of the rules, the gold market and the changes to the rules. The short redux is that the advantage to using unallocated accounts, savings accounts which are linked to gold by holding futures contracts, will end.

We’ve discussed parts of this in the past. The process of creating fake supply to control the price of gold is on the line with these rule changes.

These rules are coming at the end of June for the European Banking System which will adopt the new Basel III rules. In short, the incentive to have exposure to gold as a pile of credit will go away if the banks can’t use any of that as part of their reserve calculations for their ASF – Available Stable Fundings.

Moreover, any physical gold they hold will be held at a 15% discount. Bottom line: these rules will make it impossible for the LBMA member banks to hold any exposure to unallocated pools of gold derviatives –futures and swaps — on their balance sheets.

It will force a liquidation of those positions and end any fractional reserve leveraging of gold used to suppress the price. There will still be futures markets but the whole of the gold trade will collapse back to simply coordinating supplies of gold from producers to consumers through time, like any other commodity market.

In effect, Basel III, if implemented in its current form, would change the gold market from a speculative one based on perceptions of the efficacy of monetary policy to control real interest rates to one that should force price discovery in an almost purely physical market. As I told my Patrons in May 16th’s Market Report video, physical gold will go from being the price taker to the price maker.

And the Free Gold contingency, of which MacLeod is one, will claim victory here. These are the people who have contended for years that once the leverage in the monetary system became so big it would collapse the paper gold market as it went bidless and everyone demanded physical.

In a way they argue the same end to the current system as Murray Rothbard predicted how Bretton Woods would end when someone — France under De Gaulle — would drain the U.S. Treasury of its gold if they believed the U.S. printed more dollars than could support a peg to $35/ounce.

I sense from reading MacLeod’s last two articles, he is doing his best to contain his optimism and exuberance. Now, this week’s article from him goes into some speculation as to why this is happening. And I think he’s avoiding the real issues.

MacLeod’s avoiding the elephant in the room in the same way that Martin Armstrong last week berated the BIS for these rules knee-jerk reacting to them as more evidence of regulator incompetence, not giving much credence that it may be part of a wider strategy.

To Armstrong’s immense credit he did warn us of this in 2019, stating that Basel III’s requirements would create the very liquidity crisis we’ve been inching towards since the blowout of SOFR in September 2019, which resulted in the market spasm I call the Coronapocalypse last March once the heroin wore off and the flood of liquidity created by the Fed since then to keep the financial system alive, if on life support.

But the cliff edge of Basel III is now right in front of us, if reports are true.

To me this situation begs a number of obvious questions.

And the first is, Why Now?

We’ve been discussing these changes vis a vis Basel III for more than five years. So, why, all of a sudden is Europe so hot to implement them in June and for the U.K. to adopt them in January 2022, knowing full well that this will end the bullion banks and the central banks’ program of controlling the rise in gold prices through the application of newly-printed money to create fake supply and allow nearly infinite leverage in the gold market relative to unencumbered physical supply.

MacLeod goes through the math in this week’s article speculating as to what the real available supply of gold is versus the stated available supply. It’s vanishingly small if you assume, like he does, that both China and Russia vastly understate their gold holdings, which is a good assumption.

In October 2014 I published an article explaining why China had considerably more gold in storage than her declared reserves, and I estimated that by 2002, when the Chinese government removed the ban on personal ownership and opened the Shanghai Gold Exchange, the state could have acquired up to 25,000 tonnes. Much of this gold would have been leased gold sold into the London market …

That China had accumulated substantial undeclared bullion stocks was confirmed to me anecdotally by experienced China watchers. If we treat that as part of our estimate of monetary gold, and make an allowance for Russia, of perhaps an unrecorded 5,000 tonnes, monetary gold in the hands of everyone else appears to amount to only 15,000 tonnes.

So, again, why this, why now if suppressing gold is such a useful tool for continued faith in the central banks? Well, MacLeod gets about halfway there in my opinion.

Another popular theory is of an even wider financial reset. The BIS is coordinating research into central bank digital currencies, which if adopted cuts out the commercial banks altogether. In theory, it would allow central banks to more effectively target stimulus and do away with the destabilising cycle of bank credit. The ultimate aim could be to demote and then remove commercial banks from the financial system entirely, in which context the closure of derivative markets by regulatory means makes some sense.

That is the final act of the story not the beginning of it.

First you have to get through the crisis this would engender with the Central Banks 1) retaining some of the people’s faith they are competent and 2) they don’t go bankrupt in the process.

Now, because of its structure, the Fed can’t go bankrupt. It can print unlimited amounts of credit and ‘elastic money,’ as Martin Armstrong terms it to cover any and all time-mismatches within the banking system. That has been proven to be correct multiple times over the past 13 years since Lehman Bros. collapsed.

The ECB, on the other hand, can go bankrupt, since it has no capacity to do this. All it can do is buy the sovereign debt of the member countries’ central banks and hand them back euros, while swapping around deckchairs on this monetary Titanic. There is a definable limit to this process, especially if rates rise as people lose confidence in the underlying economic activity of those countries and their fiscal positions.

This is absolutely underway, and it isn’t like this is happening on the periphery of Europe. It’s happening in the core countries, like France and Germany. This is why I keep harping on the rise in the German 10 year bund, up nearly 60 basis points since the beginning of the year, despite Lagarde’s heroic efforts.

In March ECB President Christine Lagarde panicked and doubled the rate of bond buying within the Euro-zone by the ECB to keep rates under control. She has failed. The market woke up to the fact that she’s a lawyer not a central banker.

This week the ECB made the statement that there are ‘elevated financial stability risks’ because of a a high stock market. It was their ‘irrational exuberance’ statement. But it’s really an admission that the entire system is melting down and they have no more capacity to keep it under control.

Translation: The Banking System is Fucked and I don’t have any answers. https://t.co/35SZFC9lHM

— Tom Luongo (@TFL1728) May 21, 2021

Lagarde increasingly looks like someone overmatched for her job from a money professional’s perspective. But from the political vandalism perspective, as practiced by her real boss, Klaus Schwab of the World Economic Forum, she’s doing a bang up job screwing everything up.

Moreover, if you also are coordinating with the Bank of International Settlements and are manipulating events to transfer power from individual countries to the IMF and *shudder* the United Nations, it’s important that the institutions you have the most control over remain solvent and stand ready to offer a solution out of the incipient crisis.

That means, as a truly trapped ECB presiding over a banking system that has reached its terminal limit who is also sitting on trillions in deteriorating sovereign debt, what can you do to shore up your balance sheet at that point?

The answer is simple, the one thing the Fed cannot do, allow the price of gold to rise.

What?!

Yes.

The ECB has under its control roughly 10,000 tonnes of gold. It marks that gold to market. It’s worth at $1881 an ounce around $605 billion. The Fed, on the other hand, holds its gold, the 8133.5 tonnes it bought from the U.S. Treasury, on its balance sheet at the price it paid, $42.22 per ounce. It has a balance sheet entry of $11.04 billion

The problem is the ECB has around €6 trillion (or around $7.2 trillion at $1.21 EUR/USD) in securities on its balance sheet which are now falling in value with rising yields that Lagarde’s QE programs of various flavors cannot contain.

https://www.yardeni.com/pub/balsheetwk.pdf

The Fed has the problem of rising inflation and real yields now running -3%. Moreover, they can’t taper QE or raise rates until they are done cutting the commercial banks out of the transmission system for dollar liquidity first. Chris Whalen’s latest article on Zerohedge has the details of what’s going on at the Marriner-Eccles building.

…the FOMC is going to make permanent the RRPs (reverse-repos), essentially accepting the proposal by the Federal Reserve Bank of St Louis to create a standing repo facility for banks and nonbanks alike. This means that funds, REITs and especially smaller dealers are going to be able to go direct to the Fed of New York and finance collateral, breaking the monopoly control of the big primary dealer banks. H/T to George Selgin at Cato Institute.

Like Basel III’s changes to funding ratios, the FOMC opening up its repo and credit facilities to non-banks, REITs and anyone with a pulse, means there are big changes in store for the big commercial banks who have been running roughshod over the financial landscape for decades.

But, back to the ECB. It should be obvious now where I’m goin with this. In order for the ECB to avoid bankruptcy in the coming sovereign debt crisis, which in many ways The Davos Crowd is engineering, the price of gold will have to rise in euro-terms to offset the losses as that debt goes bidless. When that happens amidst the panic, the ECB will offer George Soros’ preferred option to investors, perpetual bonds.

The old debt will be cancelled and reissued as perpetual debt. But to pull that off the ECB will officially take control over the gold reserves of the euro-zone completely, while gold rises, putting the Fed behind the eight ball having lost the battle against commodity inflation.

So, implement Basel III, crush the incentive structure of the paper gold trade and allow real price discovery to fuel an historic rise in the price of gold. If the commercial banks in London and New York fight this they will be outcompeted and their balance sheets degraded.

Let’s take this one step further and go back to my original question. Why Now?

Simple, the private markets are beginning to realize what’s happening. The commercial banks are embracing crypto to keep their clients from bolting. There are fissures forming, as I talked about last week between the central banks and the commercial money center banks.

But, the big one, timing-wise, is the emergence of a potential parallel monetary system is threatening to capture the imagination of a generation who:

Hate the commercial banks because of the last 13 years of financial repression.

Want something tied to a real asset or at least a non-fake one of infinite supply.

Firmly distrust the existing power structure and have voted that way consistently over the past decade of Western elections.

Like bitcoin or hate it, the latest rally was deeply embarrassing to everyone who’s been skimming the cream off society via the monopolistic monetary system. Their lies were laid bare for all of us to see.

It doesn’t surprise me at all that this week was the week chosen to do the hatchet job on crypto. It was also the week where the plumbing of the financial markets became so thoroughly clogged (see Whalen’s article above) that there was no choice but to demoralize the rubes who thought they would escape the Great Reset.

Everyone must be liquidated to make the world safe for German eugenicists and commies.

So, Basel III is coming to destroy the paper gold markets and destroy the money center banks in New York and London while setting the stage to bail out the euro-zone. Higher gold prices are the answer to all of these things. Think of it this way, in a world where debt assets are failing and new private forms of custodial assets are rising in mindshare, what’s the only real weapon the central banks have to maintain credibility?

Their gold reserves.

How do you, if you are the ECB, use that weapon simultaneously against your two main competitors, the commercial banking interests in New York and London and the nascent crypto anarchists? You deploy your gold and steal everyone’s thunder.

In the end the Free Gold community will get what they want, but not for the reasons they ever thought they would — a bidless paper gold market and true price discovery in gold. What they won’t ever get is the next step, the re-monetization of gold, unless enough people see this power play for what it is and start making the appropriate moves now, which includes getting off your high horse about crypto.

So, if you are looking for these new Basel III rules to be put off again, you are most likely going to wind up on the wrong side of the trade and be just more grist for Schwab’s mill.

* * *

Join my Patreon if you can think in more than two dimensions

Donate via

BTC: 3GSkAe8PhENyMWQb7orjtnJK9VX8mMf7ZfBCH: qq9pvwq26d8fjfk0f6k5mmnn09vzkmeh3sffxd6rytDCR: DsV2x4kJ4gWCPSpHmS4czbLz2fJNqms78oELTC: MWWdCHbMmn1yuyMSZX55ENJnQo8DXCFg5kDASH: XjWQKXJuxYzaNV6WMC4zhuQ43uBw8mN4VaWAVES: 3PF58yzAghxPJad5rM44ZpH5fUZJug4kBSaETH: 0x1dd2e6cddb02e3839700b33e9dd45859344c9edc

Tyler Durden

Sun, 05/23/2021 – 15:30

Read More

{kind=link}

{kind=link}

{kind=link}