- Inflationary forces and strong demand for industrial metals and oil have lifted commodity prices in 2021

- After years of being shunned on Wall Street and by traditional financial markets, bitcoin and cryptocurrencies finally enjoyed their moment in the sun last year

- After years of playing laggards, commodities outperformed most other asset classes in 2021 and are widely expected to remain competitive in 2022

Shortly after the World Health Organization (WHO) declared Covid-19 a global pandemic, governments everywhere unveiled massive monetary and fiscal stimuli (over $15T globally) in a bid to forestall an economic fallout. The U.S. federal government stepped in with a broad array of measures, including a $2.3 trillion package designed to support financial markets, state and local governments, employers, and households. Democrats are pushing for yet another $3 trillion package to shield eligible Americans from the effects of the pandemic.

But a Wall Street expert warned that these generous packages would later come back to haunt the markets and end up doing more harm than good.

New York Times bestselling author and founder of ‘The Bear Traps Report’ Lawrence ‘Larry’ McDonald warned of the ‘cobra effect’ whereby the stimuli designed to save the economy will instead “…cause a hyperinflationary economic collapse.”

Larry sounded an eerie warning of signs of a “Lehman-like drawdown” developing in the markets and that “…we are at the early stage of the biggest cobra effect in the history of economics.” The cobra effect that Larry was alluding to is the school of thinking that says that every human decision brings with it unintended consequences.

Other than stubbornly high inflation, the markets did not see much of the cobra effect last year as most asset classes finished comfortably in the green. Bitcoin and crude oil investors enjoyed the best returns while precious metal investors had a year to forget.

The current year could finally see Larry’s predictions come true with the markets coming unstuck thanks to a hawkish Fed and rising interest rates. The S&P 500 is down 2.3% in the year-to-date; bitcoin is down nearly 11% while oil, metals, and commodities, in general, continue to do well. Gold and silver have also started the new year well thanks to a risk-off mentality pervading the markets.

Here’s how various asset classes performed in 2021.

Source: Visual Capitalist

#1. Bitcoin

2021 Returns: 59.8%

After years of being shunned on Wall Street and by traditional financial markets, bitcoin and cryptocurrencies finally enjoyed their moment in the sun last year. After a 3-year drought, crypto bulls were once again basking in the limelight as bitcoin, and its altcoin peers went on a parabolic rally beginning late 2020 that saw them take out fresh all-time highs. Bitcoin hit an all-time high of nearly $65,000 in April, and even Wall Street got carried away by the hype, with Guggenheim Globals CIO’s Scott Minerd calling a $400K price target for bitcoin.

Last April marked a real turning point in the race for cryptocurrencies going mainstream after the world’s largest cryptocurrency exchange, Coinbase Inc. (NASDAQ:COIN), finally went public via a direct listing on the NASDAQ.

The listing came at the height of the mad bitcoin rally as the leading cryptocurrency continues to enjoy growing acceptance by Wall Street and some of the world’s biggest and most recognizable institutions and companies such as Visa Inc. (NYSE:V), Square Inc. (NYSE:SQ), PayPal Holdings (NASDAQ:PYPL) and Tesla Inc. (NASDAQ:TSLA).

But alas, the good times were not to last: Bitcoin crashed spectacularly since May, losing nearly 50% in the space of two months in one of its biggest corrections by the cryptocurrency in recent years.

The market crashed in mid-May after Beijing started cracking down on the space, curbing bitcoin mining due to concerns of excess speculation and warning financial institutions against offering crypto services.

Things quickly went to the dogs after the Department of Justice seized $2.3 million in bitcoin in early June as part of its investigation into a ransomware attack that shut down the Colonial Pipeline’s gas pipeline, the nation’s largest. The DoJ seizure helped fuel concerns that U.S. officials could ramp up their crypto oversight and threw a monkey wrench into one of bitcoin’s supposed forté–non-traceability. The DOJ revealed that it seized 63.7 bitcoins, worth approximately $2.3 million, from online hacking ring DarkSide by reviewing bitcoin’s public ledger, locating the transaction, and using a private key to access the tokens. It remains unclear what methods the DOJ employed to obtain the private key, but experts have suggested that Fed officials effectively hacked the hackers in an unprecedented show of government intervention in the crypto space.

The developments rocked the markets, with bitcoin, ether, and binance coin crashing nearly 15% in a single day.

Luckily, bitcoin’s popularity ended up carrying the day, especially after the emergence of the so-called meme-based cryptocurrencies like dogecoin, Samoyedcoin, Luna, and Doge Dash. Several meme-based currencies garnered huge followings and helped propel the cryptocurrency market to a record $3 trillion market capitalization.

The leading crypto managed to pare back its losses to close the year at $47,733, good for a nearly 60% gain.

This year, bitcoin and the crypto markets have lately come under heavy selling pressure after it emerged that the Federal Reserve would likely raise interest rates sooner and more frequently than earlier anticipated. Bitcoin had tumbled 8% over the past week to trade at $42,700 just two months after hitting an all-time high of $69,000 in November, with analysts warning that it could soon breach the psychologically-important support at $40,000.

#2. WTI Crude

2021 Returns: 56.4%

Oil bulls enjoyed a banner year in 2021, and the good times appear set to continue in 2022.

The genesis of today’s high oil and gas prices can be traced back to financial pressure on oil companies from a decade of devastating losses and poor shareholder returns that have forced them to dramatically alter their business models. For years, Wall Street has pressured oil and gas companies to cut capex and shift their cash to financial goals like boosting dividends and buybacks, paying down debt, as well as decarbonization, after the fracking revolution left the U.S. shale patch bleeding cash and deeply indebted.

Consequently, investment in new wells has crashed 60% since its peak in 2014, causing U.S. crude oil production to plummet by more than 3 million barrels a day, or nearly 25%, just as the Covid virus hit, and then failed to recover with the economy. According to S&P Capital IQ data, 27 major oil makers tripled capital spending between 2004 and 2014 to $294 billion, and then cut it to $111 billion by last year. Once old wells were capped, new ones haven’t been available to fill the production gap quickly. The question is how long the restraint by publicly traded oil companies will last. Capital spending is expected to clock in around $135 billion next year, good for a 21.6% Y/Y jump but still less than half 2014’s level.

Other than severely limiting new drilling activity, U.S. shale has also been keeping its pledge to return more cash to shareholders in the form of dividends and share buybacks.

A recent report by progressive advocacy group Accountable. US says 16 of 24 large U.S. energy companies raised their dividends in 2021, while 11 made special dividend payouts totaling more than $36.5 billion. That’s a pretty impressive payout ratio considering that the sector has so far reported $174 billion in profits this year. Indeed, “variable dividends” that allow companies to hike dividends when times are good and to lower them when the going gets tough has become a favorite tool for oil and gas companies.

Meanwhile, oil and gas companies have spent a more modest $8 billion in share buybacks, though ExxonMobil ((NYSE:XOM)and Chevron (NYSE:CVX) have pledged to buy back as much as $20 billion of stock in the next two years. The energy sector has made robust share gains in the current year, which could explain the reluctance to spend too much on share repurchases.

But the most important reason, however, why oil prices have remained high is OPEC discipline:

“You have a cartel that is traditionally as disciplined as Charlie Sheen’s drinking, and for the last year they’ve been as disciplined as Olympic gymnasts,” Tom Kloza, president of Oil Price Information Service, has hilariously told CNBC.

#3. Commodities (S&P GSCI Commodity Index)

2021 Returns: 37.1% After years of playing laggards, commodities outperformed most other asset classes in 2021 and are widely expected to remain competitive in 2022.

Beginning in 2020 and extending into 2021, massive monetary and fiscal stimulus packages by the world’s governments helped facilitate the fastest economic recovery after the March deep slide. With factories humming again and consumers flush with cash, a broad commodity rally sputtered into life thanks to the so-called reflation trade.

In fact, Wall Street even predicted a commodity bull market that would rival the oil price spikes of the 1970s or the China-driven boom of the 2000s. Market experts, including Goldman Sachs, believe the commodity boom could rival the last “supercycle” in the early 2000s that powered emerging BRIC economies (Brazil, Russia, India, and China). These expectations are supported by the fact that the price movement of most commodities has historically been both seasonal and cyclical. Peering at the 10-year charts of leading commodities reveals a clear pattern of mean reversion where prices tend to oscillate backward and forward towards their mean or average.

Commodities have been among the most volatile asset classes over the past year, with supply chain disruptions and surging inflation sending prices into the stratosphere. Rising commodity prices, particularly energy, have been as much a reflection of soaring demand as a lack of supply.

Here were the best-performing commodities in 2021.

- Lithium

52-Week Change (2021) : 477%

Price (Dec 31): $42,256 per tonne

The transition from ICE vehicles to EVs has become a focal point of the global electrification drive. In 2020, global sales of EVs increased a robust 39% year on year to 3.1 million units, an impressive feat right in the midst of a major health crisis. Bloomberg New Energy Finance(BNEF), however, says 2021 is “yet another record year for EV sales globally,” with an estimated 5.6 million units sold, good for 83% Y/Y growth and a 168% increase over 2019 sales.

That’s a big reason to be bullish about one of the most important commodities that go into those EV batteries: Lithium.

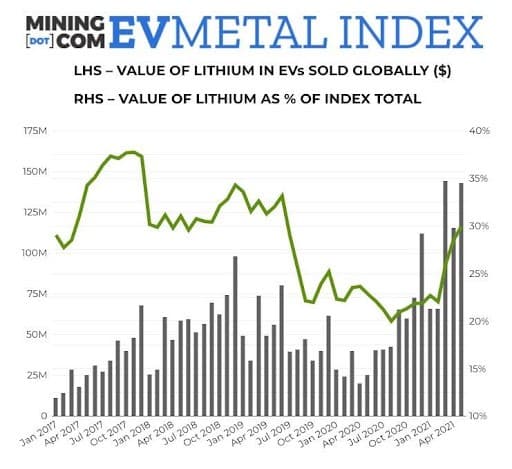

Last year, Mining.com launched the EV Battery Metals Index, a tool that tracks the value of lithium, cobalt, nickel, and other battery metals flowing into the global EV industry at any given point in time. The index combines two main sets of data: prices paid for the mined minerals at the point of entry into the global battery supply chain and the sales-weighted volume of the raw materials in electric and hybrid passenger car batteries sold around the world.

That index has quadrupled from May 2020, indicating an industry that’s been expanding at breakneck speed this year–even despite challenges such as the ongoing pandemic, supply chain constraints and rising raw materials costs.

Back in 2009, around the time when Tesla’s first Roadsters hit the road, electric and hybrid cars sold around the world contained a paltry 31 tonnes of lithium in their batteries worth a combined $182,000. Fast forward to the present, and the industry has grown 3,330-fold for a value of $609 million. Over the past five years alone, the annualized value of lithium in EVs has gone up more than 1,000%.

Source: Mining.com

The average value of lithium on a per-vehicle basis climbed 20% year over year in 2021, while total material deployed jumped 196% over last year, with lithium carbonate making up roughly half of the total vs. lithium hydroxide, with the latter favored in the manufacture of high-nickel content batteries. Lithium carbonate prices are up 91.4% in the year-to-date to $13,769.20 per ton, a massive jump compared to the situation in 2020 when prices spent several months under $7,000 a tonne.

Despite the impressive rally, lithium could remain bullish for years.

Supply shortages

Last year, Chile’s second-largest lithium producer, Albemarle Corp. (NYSE:ALB), warned that global supplies of lithium were on course for a major shortfall in a few years’ time if prices continued to fail to reflect the costs of funding massive expansions amid the EV boom. Specifically, ALB highlighted the chasm between discount-hunting EV manufacturers and lithium producers who were unable to meet growing demand at persistently low prices.

Related: Saudis Arabia Reserves $10 Billion To Buy The Stock Market Dip

But maybe Eric Norris, operations manager for Albermale’s lithium business, rushed his fences: lithium carbonate prices have nearly doubled since then.

Despite lithium carbonate prices doubling from those lows, another giant lithium producer has been singing the same tune.

Jiangxi Ganfeng Lithium, the world’s largest lithium mining company with a market capitalization of $19 billion, is saying that lithium prices will continue to rally as lithium production struggles to keep up with massive demand for EVs. The Chinese company has some decent street cred–after all, it counts leading EV automakers such as Tesla Inc. (NASDAQ:TSLA) and BMW (OTCPK:BMWYY) among its customers.

Ganfeng Lithium has gone into an acquisition spree as it anticipates an extended lithium boom, as reported by Bloomberg, thanks to a global supply squeeze.

Another reason to be bullish: prices for copper, nickel, cobalt, and lithium could reach historical peaks for an unprecedented, sustained period in a net-zero emissions scenario, with the total value of production rising more than four-fold for the period 2021-2040, and even rivaling the total value of crude oil production.

According to Eurasia Review analyst, in a net-zero emissions scenario, the metals demand boom could lead to a more than fourfold increase in the value of metals production–totaling $13 trillion accumulated over the next two decades for the four metals alone. This could rival the estimated value of oil production in a net-zero emissions scenario over that same period, making the four metals macro-relevant for inflation, trade, and output, and providing significant windfalls to commodity producers.

- Ethanol

52-Week Change (2021): 125%

Price (Dec 30): $3 per gallon

According to a report published by a market research firm IndexBox, U.S. ethanol prices climbed sharply in 2021. Based on data from USDA, the average ethanol price grew from $1.4 per gallon in January to more than $3.2 per gallon in November 2021, with the biggest gains coming in November when prices for alcohol leaped up by more than 30%. Ethanol prices have been on a tear on strong demand for biofuels as more and more drivers hit the road and climate awareness increases.

U.S. ethanol fuel production has rebounded after a downturn in 2020, with 3.9M barrels of ethyl alcohol produced through the first eight months of 2021 compared to 3.7M barrels and 4.0M barrels manufactured in similar timeframes in 2020 and 2019, respectively.

Despite the growth in demand and increased prices in 2021, the last synthetic ethanol facility in the U.S., Tuscola Plant, owned by petrochemical giant LyondellBasell (NYSE:LYB) announced that it would close at the end of 2021 thanks to ballooning energy and production costs making it increasingly difficult for synthetic ethanol to compete with bioethanol. Meanwhile, prices for corn, which is widely used to produce alcohol, have gone down this year: Eastern Cornbelt average corn price decreased from $7.60 per bushel in May to $5.60 in November, giving bioethanol plants an edge. Fuel-ethanol prices have steadily declined over the past decade.

Industry experts have predicted that government policies will continue to support the development of the bioethanol market. The U.S. Department of Agriculture (USDA) has announced that it will invest $26M into building biofuel infrastructure in 23 states as part of the ‘Higher Blends’ program. The subsidies will facilitate replacing old-style fuel pumps and storage tanks with blended pumps and tanks suitable for E15 and E85 fuels, as well as biodiesel. The USDA projects that these grants will help increase potential sales for biofuels by 822M gallons per year. To-date, the USDA has invested $66.4 million in projects that are projected to increase biofuels sales by 1.2 billion gallons annually.

- Coal

52-Week Change (2021): 111%

Price (Dec 30): $170.10 per ton

A severe shortage of natural gas, declining wind power output, nuclear outages, and cold weather have conspired to hand Europe and the rest of the world one of the worst energy crises on record. This has been a major boon for ‘greener’ fossil fuels such as natural gas and LPG, but also for the out-of-favor coal sector.

For years, coal prices have fallen off a cliff as power companies continued closing down their coal plants in favor of natural gas generation. In 2020, the EIA reported that 121 coal-fired plants had been closed or replaced with natural gas, leading to nearly 80 GW of coal capacity being retired or plants repurposed to burn natural gas. But a massive spike in natural gas prices and huge shortages in 2021 tipped the balance in favor of coal, leading to a sharp increase in demand. Indeed, the EIA said coal-fired electricity generation was on track to increase for the first time since 2014, rising by 22% compared with 2020. Carbon dioxide emissions from the energy sector were estimated to increase 7% as a result.

Consequently, U.S. coal prices have jumped to their highest level since 2009 as miners attempt to keep pace with the surging demand for the fossil fuel.

A cross-section of U.S. miners remains bullish about the coal outlook in 2022, with some already having contracts to sell almost all of their expected output. Others are less sanguine, with Jeffires bullish about mining metals but less so on iron ore and coal.

“We are bullish on mining for 2022 based on fundamental factors and valuations,” Jefferies has said in a note entitled: “Same old song and dance for 2022″.”We are most constructive on the base metals, and especially copper and aluminum, while we are most cautious on iron ore and coal.”

Prices of most base metals have remained stubbornly high, with experts predicting more of the same in 2022.

- Oat

52-Week Change (2021): 90.4%

Price (Dec 31): $686.75 per bushel

- Coffee

52-Week Change (2021): 78.4%

Price (Dec 30): $228.85 per pound

- Gasoline

52-Week Change (2021): 61.7%

Price (Dec 31): $2.27 per gallon

- Naphtha

52-Week Change (2021): 61.5%

Price (Dec 31): $3 per ton

- Propane

52-Week Change (2021): 60.6%

Price (Dec 31): $1.04 per gallon

- Heating Oil

52-Week Change (2021): 60.4%

Price (Dec 31): $2.74 per gallon

- Crude Oil

52-Week Change (2021): 57.8%

Price (Dec 31): $76.54 per barrel

Alex Kimani is a veteran finance writer, investor, engineer and researcher for Safehaven.com