BofA Crashes The “Transitory” Party: Sees Up To 4 Years Of “Hyperinflation”

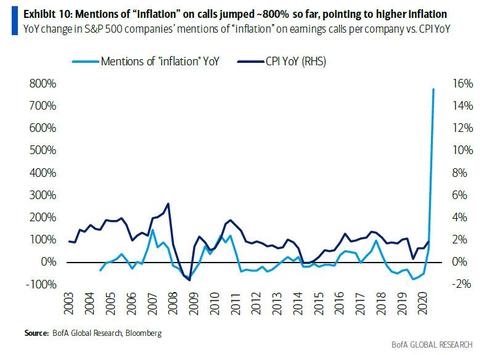

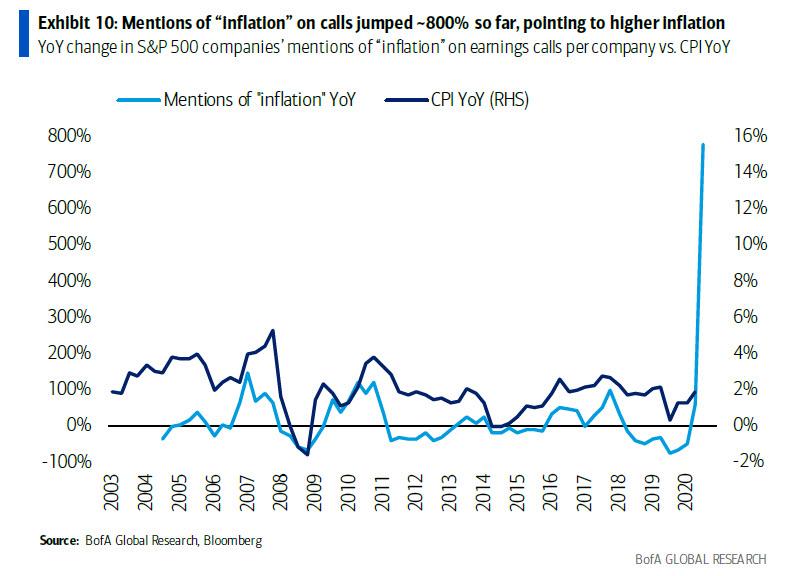

At the start of May, when observing the avalanche of “higher inflation” mentions on Q1 earnings calls, which had quadrupled YoY; and jumped by a record 800% YoY…

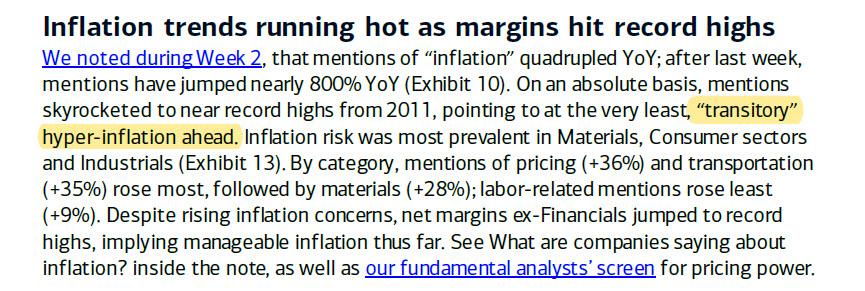

… BofA chief equity strategist Savita Subramanian summarized the current state of affairs as follows: “On an absolute basis, [inflation] mentions skyrocketed to near record highs from 2011, pointing to at the very least, “transitory” hyper-inflation ahead.“

Needless to say, a “serious” bank warning of hyperinflation – transitory or otherwise – was enough to spark very serious concerns that the Fed was losing control of prices, a panic which only grew after Deutsche Bank joined the chorus, earlier this month when it warned that inflation was about to explode “Leaving Global Economies Sitting On A Time Bomb.“

Of course, BofA had left itself a loophole, the same loophole used so generous by the Fed as often as several times each day: after all the definition of transitory is fluid, and could be as short as just a few weeks, making the coming period of pain somewhat manageable.

Not so fast.

While the Fed has bet what little credibility it has left on the benign meaning of “transitory” in setting its monetary policy (no rate hikes until 2023 by which point inflation will be in the double digits) and today’s UMichigan commentary echoed the Fed’s cheerful sentiment, predicting that soaring inflation won’t last long, with Consumer Survey economist Richard Curtin writing that “year-ahead inflation expectations fall slightly to 4.2% in June from May’s decade peak of 4.6%, [as] consumers believed that the price surges will mostly be temporary”, one of the most respected Bank of America strategists just crashed the “transitory” party, and in a note published today, BofA Chief Investment Strategist Michael Hartnett wrote that, far from transitory, soaring US prices may last up to 4 years.

Observing that US inflation averaged 3% in the past 100 years, 2% in 2010s, 1% in 2020, and is “annualizing 8% thus far in 2021”, Hartnett writes that it is ” so fascinating so many deem inflation as transitory when stimulus, economic growth, asset/commodity/housing inflations (are) deemed permanent.”

As a result, Bank of America sees “US inflation firmly in 2-4% range next 2-4 years” consisting of “asset, commodity, and housing inflation.” And even though the Fed may have staked its reputation and credibility on keeping the current ultra-loose regime until well into 2023, Hartnett predicts that “only a market crash will prevent global central banks tightening next 6 months.”

Hartnett then lists the various factors that form his hawkish view starting with the fiscal policy bubble, writing that the latest Biden infrastructure plan ($600bn new spend) “takes running tally of global monetary & fiscal stimulus to $30.5tn past 15 months, an amount equivalent to entire Chinese & European GDP’s.” Just in case there is any confusion why despite millions still unemployed, consumer spending is now far higher than it was before the covid pandemic.

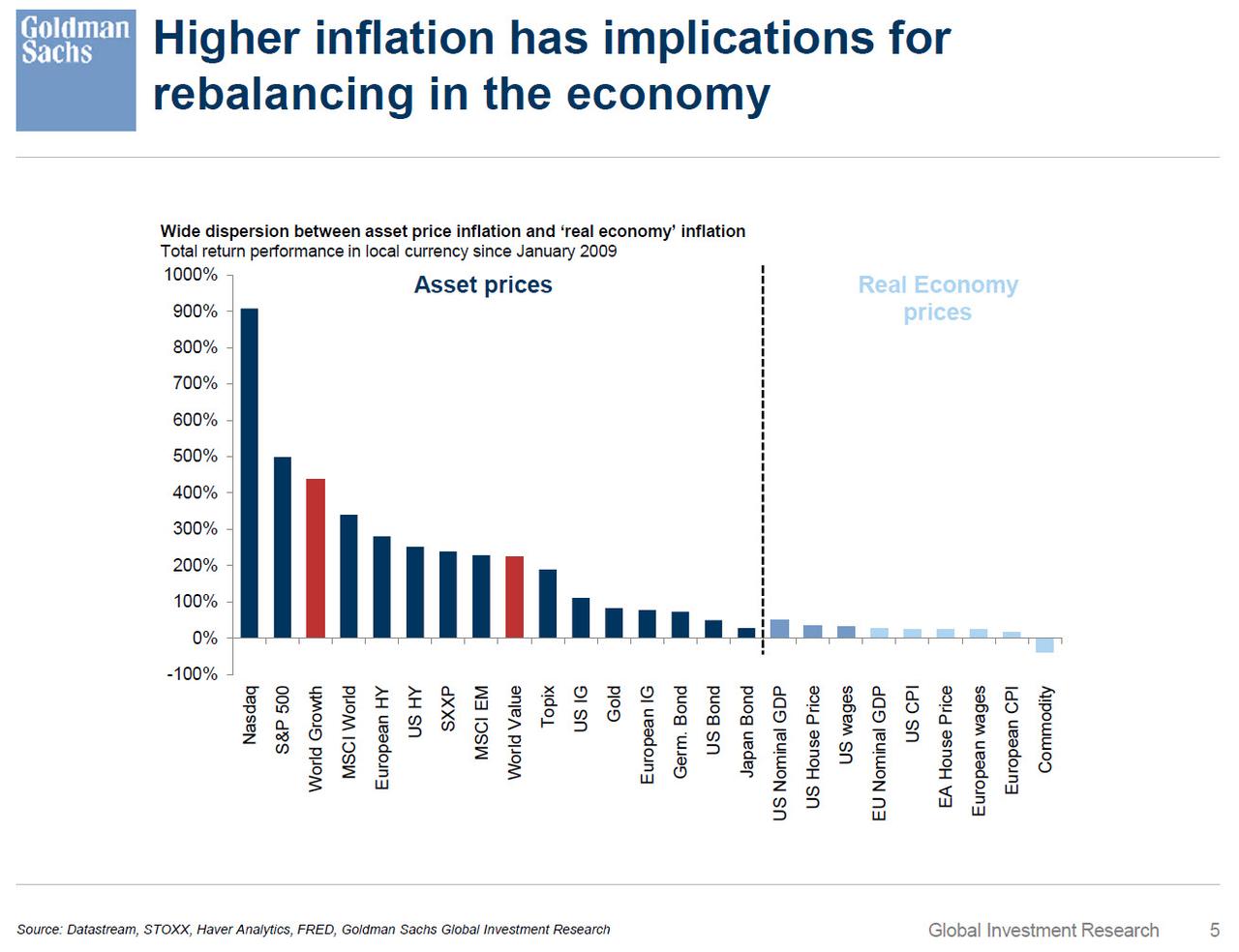

The BofA CIO then looks at asset inflation, which as even Goldman has shown is hyperinflating compared to the more dormant economic inflation (which however is also starting to move)…

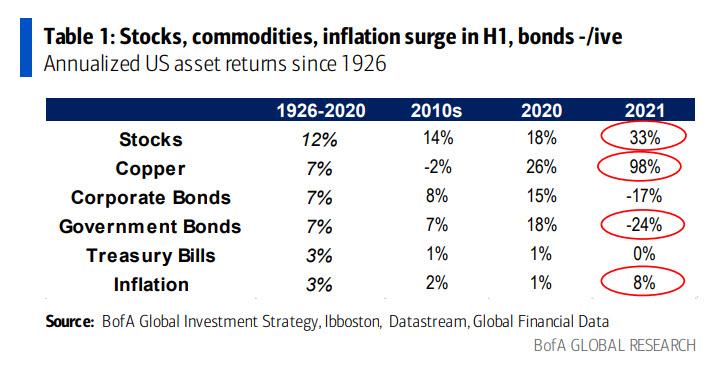

… and pointing out that central banks have bought $900 million of financial assets every hour in past 15 months leading to “epic gains in stocks & commodities past 15 months relative to 100-year history (Table 1)” and pushing the global equity market cap up staggering $54 trillion over this period.

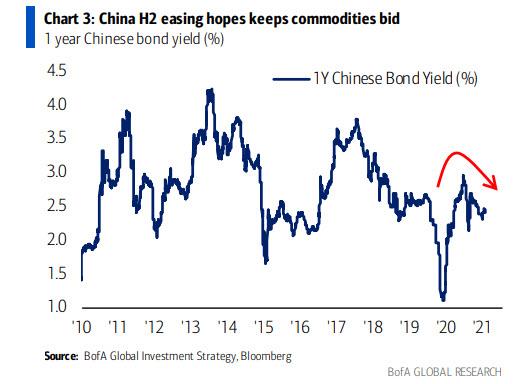

There’s more: after soaring for much of the past 6 months, commodity inflation has continued to rise, driven by hopes that China will ease further in the second half (China 1-year rates down 50bps past 6 months)…

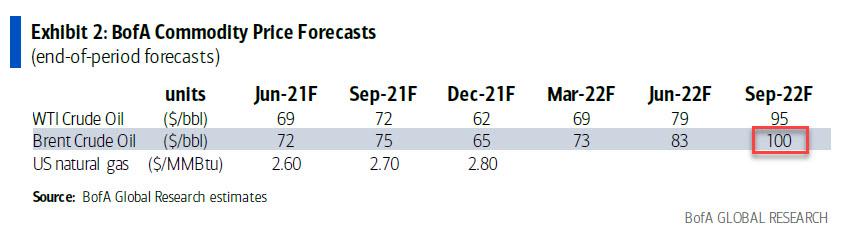

… despite recent Fed hawkish practice run; note that recently another BofA strategist said he expects oil to hit $100/bbl in 2022.

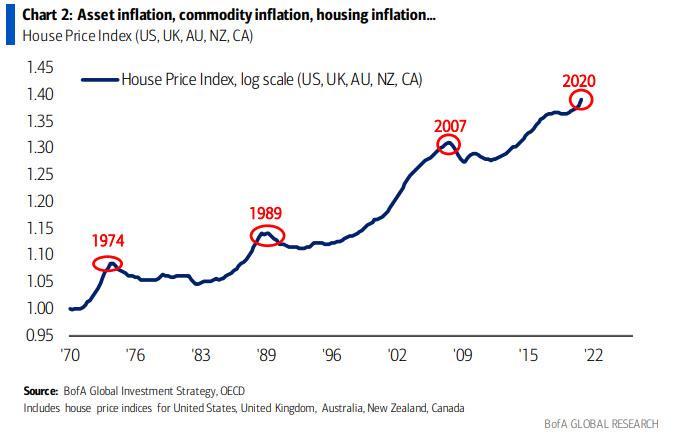

Last but not least, there is the housing inflation (or “hyperinflation” according to Ivy Zelman), with Hartnett writing that surging house prices across US, UK, Scandanavia, Canada, Australia, NZ (up almost 30% YoY), mark the 4th housing boom of past 50-years ).

This has forced central banks in in Norway, Denmark, New Zealand, Australia, and Canada – but not the Fed of course – to tilt toward “macro-prudential” measures, i.e. to consider surging home prices when making policy decisions.

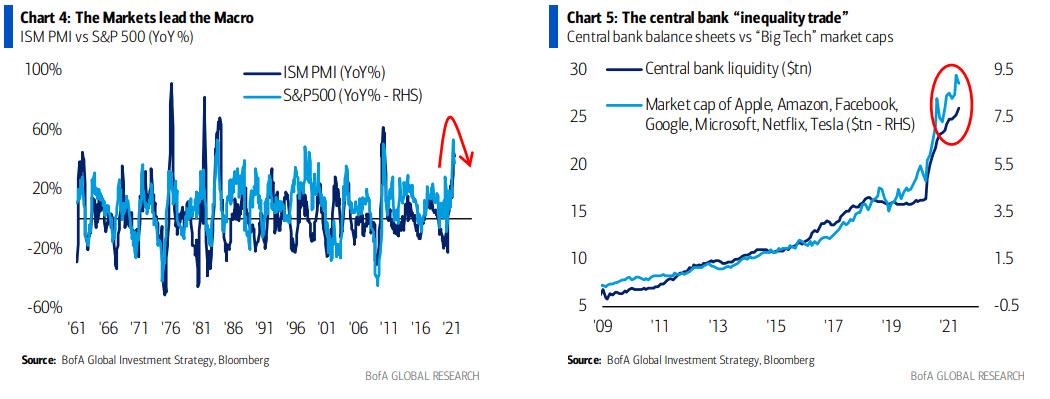

Needless to say, all these asset bubbles generously created by the Fed and other central banks continue to widen the record inequality rift. And while central banks will never admit it, Hartnett writes that markets almost always lead macro (stocks excellent lead indicator of economic growth – Chart 4), and since the Fed knows it can only impact business & consumer behavior via credit spreads & stock prices (Chart 5)…

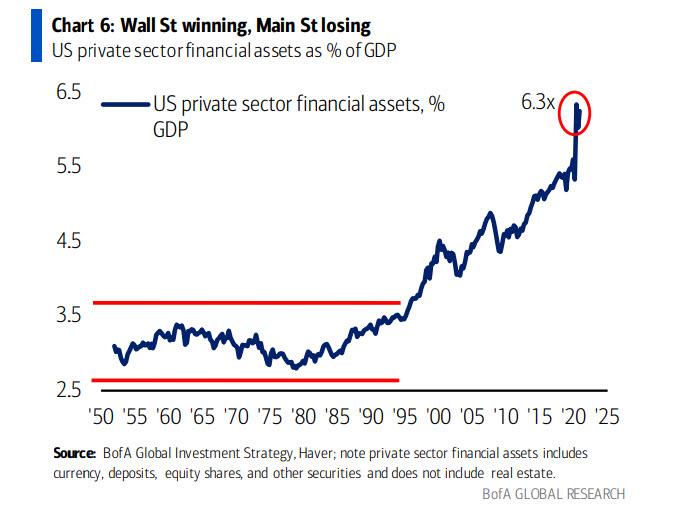

… its policy is totally directed at Wall Street. But the problem is that the Wall Street boom, built up ever since the LTCM “fed put” bailout and the Greenspan days, is enormous relative to Main Street and as the familiar chart below shows, US financial assets are now 6.3x GDP…

… and for context, US stocks are up $27 trillion higher compared to pre-COVID levels while US payrolls are 8 million below Feb’20 level.

As the head BofA strategist concludes, it is “tough to solve inequality with QE.” If only anyone at the Fed had this degree of clarity.

Putting all of the above together, Hartnett concludes that while stocks are hitting daily all time highs, the party is ending with higher inflation, hawkish central banks, weaker growth; combo of rising Rates, Regulation, Redistribution (3Rs) & peak Positioning, Policy, Profits (3Ps), leading to low/negative stock/credit H2 returns, and the resulting optimal “barbell” trade is long inflation assets & defensive/quality assets.

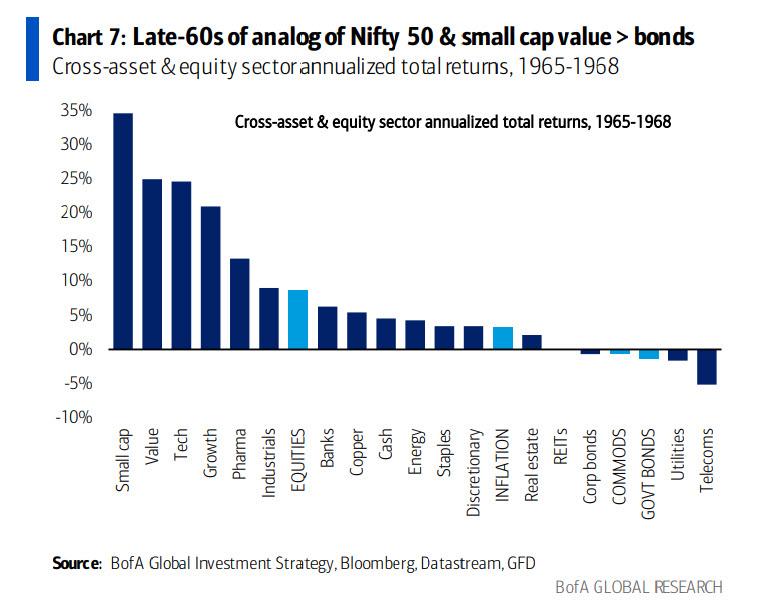

Why? Because to Hartnett, the proper analog to the current buying frenzy is the late-60s “when inflation & interest rates became unanchored on back of fiscal excess and subservient Fed caused barbell of Nifty 50 & small cap value stocks to significantly outperform bonds.”

And speaking of 1960s parallels, Hartnett sees the iconic Nifty 50 as the analogue to today’s FANGs: “note best performance from Nifty 50 was 1966-70 period on 1st rise in inflation (Chart 8); 2nd surge in inflation in early-70s saw Nifty 50 hit secular peak…

… which was followed by a decade of underperformance. In other words, the days of FAAMGs outperformance are almost over.

Tyler Durden

Fri, 06/25/2021 – 13:45

BofA Crashes The “Transitory” Party: Sees Up To 4 Years Of “Hyperinflation”

At the start of May, when observing the avalanche of “higher inflation” mentions on Q1 earnings calls, which had quadrupled YoY; and jumped by a record 800% YoY…

… BofA chief equity strategist Savita Subramanian summarized the current state of affairs as follows: “On an absolute basis, [inflation] mentions skyrocketed to near record highs from 2011, pointing to at the very least, “transitory” hyper-inflation ahead.”

Needless to say, a “serious” bank warning of hyperinflation – transitory or otherwise – was enough to spark very serious concerns that the Fed was losing control of prices, a panic which only grew after Deutsche Bank joined the chorus, earlier this month when it warned that inflation was about to explode “Leaving Global Economies Sitting On A Time Bomb.”

Of course, BofA had left itself a loophole, the same loophole used so generous by the Fed as often as several times each day: after all the definition of transitory is fluid, and could be as short as just a few weeks, making the coming period of pain somewhat manageable.

Not so fast.

While the Fed has bet what little credibility it has left on the benign meaning of “transitory” in setting its monetary policy (no rate hikes until 2023 by which point inflation will be in the double digits) and today’s UMichigan commentary echoed the Fed’s cheerful sentiment, predicting that soaring inflation won’t last long, with Consumer Survey economist Richard Curtin writing that “year-ahead inflation expectations fall slightly to 4.2% in June from May’s decade peak of 4.6%, [as] consumers believed that the price surges will mostly be temporary”, one of the most respected Bank of America strategists just crashed the “transitory” party, and in a note published today, BofA Chief Investment Strategist Michael Hartnett wrote that, far from transitory, soaring US prices may last up to 4 years.

Observing that US inflation averaged 3% in the past 100 years, 2% in 2010s, 1% in 2020, and is “annualizing 8% thus far in 2021″, Hartnett writes that it is ” so fascinating so many deem inflation as transitory when stimulus, economic growth, asset/commodity/housing inflations (are) deemed permanent.”

As a result, Bank of America sees “US inflation firmly in 2-4% range next 2-4 years” consisting of “asset, commodity, and housing inflation.” And even though the Fed may have staked its reputation and credibility on keeping the current ultra-loose regime until well into 2023, Hartnett predicts that “only a market crash will prevent global central banks tightening next 6 months.”

Hartnett then lists the various factors that form his hawkish view starting with the fiscal policy bubble, writing that the latest Biden infrastructure plan ($600bn new spend) “takes running tally of global monetary & fiscal stimulus to $30.5tn past 15 months, an amount equivalent to entire Chinese & European GDP’s.” Just in case there is any confusion why despite millions still unemployed, consumer spending is now far higher than it was before the covid pandemic.

The BofA CIO then looks at asset inflation, which as even Goldman has shown is hyperinflating compared to the more dormant economic inflation (which however is also starting to move)…

… and pointing out that central banks have bought $900 million of financial assets every hour in past 15 months leading to “epic gains in stocks & commodities past 15 months relative to 100-year history (Table 1)” and pushing the global equity market cap up staggering $54 trillion over this period.

There’s more: after soaring for much of the past 6 months, commodity inflation has continued to rise, driven by hopes that China will ease further in the second half (China 1-year rates down 50bps past 6 months)…

… despite recent Fed hawkish practice run; note that recently another BofA strategist said he expects oil to hit $100/bbl in 2022.

Last but not least, there is the housing inflation (or “hyperinflation” according to Ivy Zelman), with Hartnett writing that surging house prices across US, UK, Scandanavia, Canada, Australia, NZ (up almost 30% YoY), mark the 4th housing boom of past 50-years ).

This has forced central banks in in Norway, Denmark, New Zealand, Australia, and Canada – but not the Fed of course – to tilt toward “macro-prudential” measures, i.e. to consider surging home prices when making policy decisions.

Needless to say, all these asset bubbles generously created by the Fed and other central banks continue to widen the record inequality rift. And while central banks will never admit it, Hartnett writes that markets almost always lead macro (stocks excellent lead indicator of economic growth – Chart 4), and since the Fed knows it can only impact business & consumer behavior via credit spreads & stock prices (Chart 5)…

… its policy is totally directed at Wall Street. But the problem is that the Wall Street boom, built up ever since the LTCM “fed put” bailout and the Greenspan days, is enormous relative to Main Street and as the familiar chart below shows, US financial assets are now 6.3x GDP…

… and for context, US stocks are up $27 trillion higher compared to pre-COVID levels while US payrolls are 8 million below Feb’20 level.

As the head BofA strategist concludes, it is “tough to solve inequality with QE.” If only anyone at the Fed had this degree of clarity.

Putting all of the above together, Hartnett concludes that while stocks are hitting daily all time highs, the party is ending with higher inflation, hawkish central banks, weaker growth; combo of rising Rates, Regulation, Redistribution (3Rs) & peak Positioning, Policy, Profits (3Ps), leading to low/negative stock/credit H2 returns, and the resulting optimal “barbell” trade is long inflation assets & defensive/quality assets.

Why? Because to Hartnett, the proper analog to the current buying frenzy is the late-60s “when inflation & interest rates became unanchored on back of fiscal excess and subservient Fed caused barbell of Nifty 50 & small cap value stocks to significantly outperform bonds.”

And speaking of 1960s parallels, Hartnett sees the iconic Nifty 50 as the analogue to today’s FANGs: “note best performance from Nifty 50 was 1966-70 period on 1st rise in inflation (Chart 8); 2nd surge in inflation in early-70s saw Nifty 50 hit secular peak…

… which was followed by a decade of underperformance. In other words, the days of FAAMGs outperformance are almost over.

Tyler Durden

Fri, 06/25/2021 – 13:45

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}