On March 15, 2022, the IMF published an article written by a group of authors stating that the impact will be carried out through three main channels. Firstly, higher prices for commodities such as food and energy will lead to a further increase in inflation, which in turn will reduce the cost of income and put pressure on demand.

Secondly, neighbouring economies, in particular, will face disruptions in trade, supply chains and money transfers, as well as a historic increase in the flow of refugees. And thirdly, lower business confidence and increased investor uncertainty will put pressure on asset prices, tightening financial conditions and potentially encouraging capital outflows from emerging markets. [i]

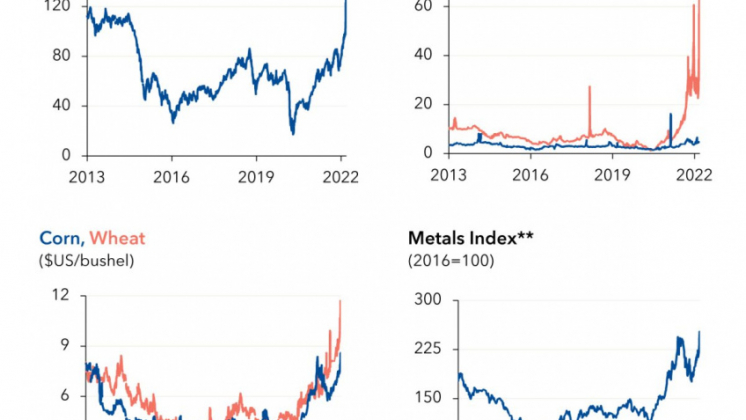

It was pointed out that Russia and Ukraine are the main producers of raw materials, and disruptions have led to a sharp increase in world prices, especially for oil and natural gas. Food prices jumped, and wheat reached a record high.

In addition to the global spillover effects, countries with direct trade, tourism and financial risks will experience additional pressure. Economies dependent on oil imports will face wider fiscal and trade deficits and increased inflationary pressures, although some exporters, such as those in the Middle East and Africa, may benefit from higher prices.

More dramatic increases in food and fuel prices may increase the risk of unrest in some regions, from sub-Saharan Africa and Latin America to the Caucasus and Central Asia, while food insecurity is likely to worsen further in parts of Africa and the Middle East.

In the long run, conflict can fundamentally change the global economic and geopolitical order if energy trade changes, supply chains change, payment networks break down, and countries rethink their reserve currency reserves. Increased geopolitical tensions further increase the risks of economic fragmentation, especially in the areas of trade and technology.

Another report said that food prices had already risen by 23.1% last year, the fastest pace in more than a decade, according to United Nations data adjusted for inflation. February’s reading was the highest since 1961 for an indicator that tracks the prices of meat, dairy products, cereals, oils and sugar.

Now, the conflict in Ukraine and sanctions on Russia are undermining supplies and possibly production for the world’s two largest agricultural producers. The two countries account for almost 30% of global wheat exports and 18% of maize, most of which is delivered through the Black Sea ports, which are now closed. [ii]

The main buyers of Ukrainian grain in 2021 were Indonesia, Egypt, Turkey, Pakistan, Saudi Arabia and Bangladesh. It is likely that they will have to urgently look for an alternative source of supply, since the sowing campaign in Ukraine this season is likely to be disrupted.

Over the past three weeks, we have received news about various sectors that are related to production in Ukraine.

A number of automobile companies (and not only) in Europe buy electric cables from Ukrainian companies. Now deliveries have stopped, which threatens to disrupt the entire production process. Electric cable in the rating of Ukrainian goods for export is technologically the most complex, so its further production will depend on the availability of the necessary components, and on the maintenance in proper condition of enterprises that are able to provide the entire technological cycle.

Semiconductor production around the world has also suffered, as the main suppliers of neon gas used in this high-tech production are Russia and Ukraine. [iii]

The “Cryoin” plant is located near Odessa and was engaged in the production and supply of such rare gases as neon, isotopes 20Ne, 21Ne and 22Ne, helium, xenon, krypton. [iv]

Another company specialising in such production, “Ingaz”, is located in Mariupol. [v] Now the production process of both is completely stopped.

Mariupol also has a concentrated metallurgical industry, whose products were supplied to many countries-pipes, rolled products, rebar, cast iron, etc. Now they are not shipped either to Europe or to other regions of the world where there were customers, and because of this, a number of infrastructure and construction projects were on the verge of failure or freezing.

Iron and other types of ore in terms of sales volumes abroad were at the approximate level of revenues with corn and wheat. Now their production and transportation are stopped.

Sunflower oil is also on the list of products that create a domino effect. In previous years, Ukraine has achieved record exports of this type of product. The top five buyers were India, China, the Netherlands, Iraq and Spain. And in Russia, it is planned to introduce an export duty on sunflower oil, which will also affect world prices.

Pomace, that is, the remains of cereals after squeezing oil from them, also made it possible to receive about $1 billion a year in the country’s budget. Approximately the same amount of money Ukraine managed to get for the sale of rapeseed.

Fuelwood is also among the top products that are exported from Ukraine. In recent years, it has accounted for more than 10% of the global market for this specific category. Probably, shipments from the western regions are still continuing, but soon they will also be stopped.

A small segment of exports was also occupied by mushrooms (champignons), mainly for Romania, Moldova and Belarus, but also to other countries.

For many years, an important element of the engine of the Ukrainian economy was also gastarbeiters. For example, in 2019, according to the National Bank of Ukraine, foreign workers transferred $12 billion there, while at the same time, the inflow of foreign direct investment amounted to $ 2.5 billion. [vi]

Now the banking system of Ukraine does not function, so this segment of the economy simply fell off. And who to send money to if millions of citizens have already left the country?

The burden due to the influx of refugees now falls on the countries of the European Union. Let’s add to this the collapse of the Ukrainian law enforcement system, in which criminal elements, including representatives of international groups, begin to actively manifest themselves. This also applies to the EU, where in a number of cities indigenous people already feel uncomfortable and experience all sorts of inconveniences, from theft and damage to property to manifestations of open aggression.

It is also quite natural to talk about the stock market of Ukraine, where stock prices of almost all national companies crept down on February 22 after the recognition of the DPR and LPR by Russia. For example, shares of “Ukrnafta” fell by 9%, and “Ukrtelekom” by 12%. But now the stock exchange of Ukraine practically does not work.

As for Russia, the sanctions imposed and measures taken by the Russian government to counter them are also reshaping the global economy. But if the voice of the people in the United States and the EU is already heard about unreasonably high prices for fuel and electricity, then Russia is not in danger. Just as there is no threat of a food crisis and some serious costs. But Moscow can tighten the screws even more for the West and those who support anti-Russian sanctions.

The recent discussion at the Council on Foreign Relations (USA) is indicative. [vii] Karen Karniol-Tambour of Bridgewater Associates noted that “Russia, I think, is well-aware of its power. It well-aware of what are the commodities that are small deal for its income balance, they don’t make a lot of money from them, but a big deal for the world because they’re a major supplier of a small piece.

Then kind of they can jam up a whole supply chain that way. And then you go to oil markets, which are just very politically sensitive in countries like our own because just having higher oil prices is extremely regressive. So we’ve already been living with the highest inflation we’ve seen in forty years or so.”

Isabelle Mateos y Lago of BlackRock, who also participated in the discussion, noted some of the nuances that affect the global financial and economic system, saying that “we’re in a new environment where things that were considered unthinkable now we know can happen. And it’s not clear to me that as of today there are meaningfully better alternatives to the existing set of reserve currencies.

And by the way, for the world’s largest reserve holders, which is China, the renminbi, of course, is not an option because it’s not an FX reserve. And so that central bank has an even bigger problem on its hands than everybody else in terms of funding new reserve assets.

But I would say the overwhelming point of feedback that I’m hearing right now from reserve monitors is, you know, there’s this old mantra of safety. Liquidity, return is what they’re looking for in FX reserves.

Recently there had been a bit more emphasis on the return because, you know, bond yields being so low everywhere. And I think all of a sudden people realised that actually safety and liquidity really matter and are going to look much more carefully at what they’re holding in their balance sheets.”

Although Lago is clearly misleading about the renminbi, as it has been in the IMF basket since 2016, her words about the unthinkable indicate the collapse of unipolar US hegemony. Therefore, any measures taken by Russia, including the temporary suspension of gas and oil supplies, if this helps to dominate the dollar and “cure” European politicians, would be very useful.

[I] https://blogs.imf.org/2022/03/15/how-war-in-ukraine-is-reverberating-across-worlds-regions/

[ii] https://blogs.imf.org/2022/03/16/war-fueled-surge-in-food-prices-to-hit-poorer-nations-hardest/

[iii] https://www.cnews.ru/news/top/2022-03-11_rossiya_obrushila_mirovoe

[iv] https://krioin-inzhiniring.prom.ua/

[vi] https://ukraina.ru/exclusive/20200630/1028130398.html

[vii] https://www.cfr.org/event/world-economic-update-inflation-sanctions-and-russia-ukraine-war