With this banking crisis, which has serious Lehman vibes, it is a good time to revisit my article, Is This The End of The End of History, from March of last year. The article delt with the theme of collapse vs stagnation, and historical cycles, in light of the Ukraine war, the post-pandemic climate, the onset of inflation, and speculation about economic collapse. A point of mine, that has especially been vindicated, is that “a delay in the Fed raising interest rates, could cause a short term rally in stocks, further expanding the bubble. The bigger the bubble, the worse inflation gets, and the longer the Fed keeps delaying raising rates, the worse the crash will be down the road.” For the most part, most of my geopolitical and economic forecasts have come true, though I actually predicted an economic collapse to occur sooner, which actually vindicates that point, that kicking the can down the road will just create a much worse crisis.

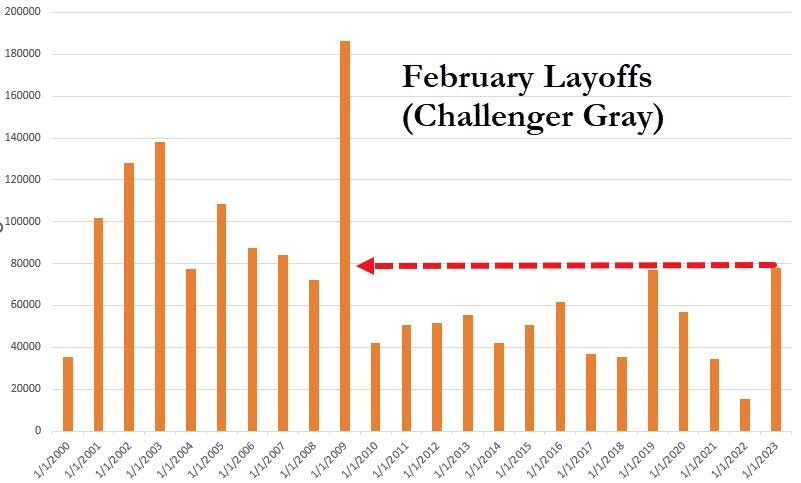

Despite countless signs of economic volatility, the recent bank failures, with shockwaves to the entire financial system, are a turning point, where it is clear that there is going to be a severe economic downturn. For instance, Elon Musk recently said, lot of current year similarities to 1929, and Moody’s cut the outlook on the entire U.S. banking system to negative from stable, citing a “rapidly deteriorating operating environment.” Even the perma bulls, mainstream media, and financial “experts,” can no longer deny the obvious signs of economic peril. However, the bullish propaganda was still strong as recently as January, which was really the bulls’ last gasp, with the monkey rally, in response to the Fed only raising interest rates by .25 points, plus economic data showing record low unemployment plus a dip in inflation.

It has always been the case with bubbles, that the greater the size of the bubble, the more copes to deny reality, and the more vested interests there are in preventing the inevitable crash. Certainly many corporations and banks have made economic decisions based upon an assumption of a soft landing or Fed pivot. This also explains the gaslighting to justify that the 2010s economic boom, especially in tech, was based upon productivity and innovation, when it was primary due to Fed monetary policy, plus data mining in the case of Big Tech. While it is silly for conservatives to blame wokeness as the primary culprit of bank failures, wokeness and bullshit DEI jobs, are a symptom of the corruption that Fed policy enabled.

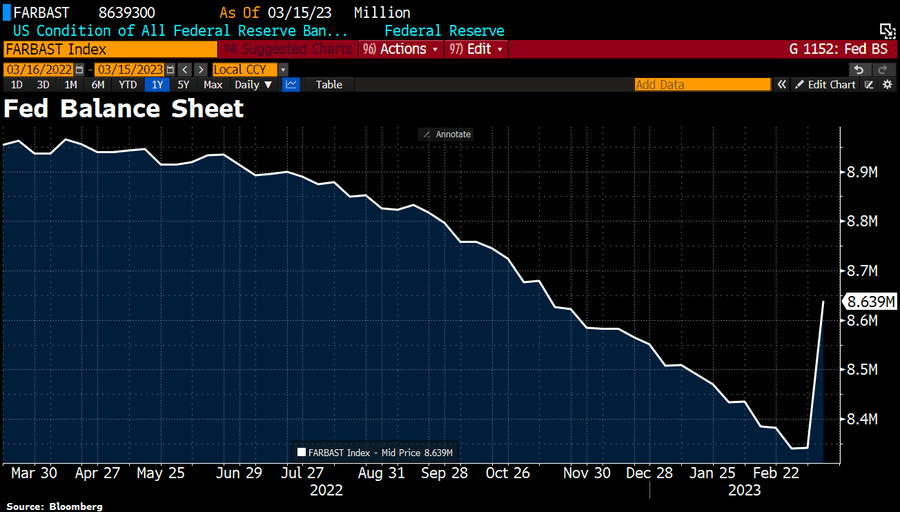

Fed Balance Sheet: Return to QE

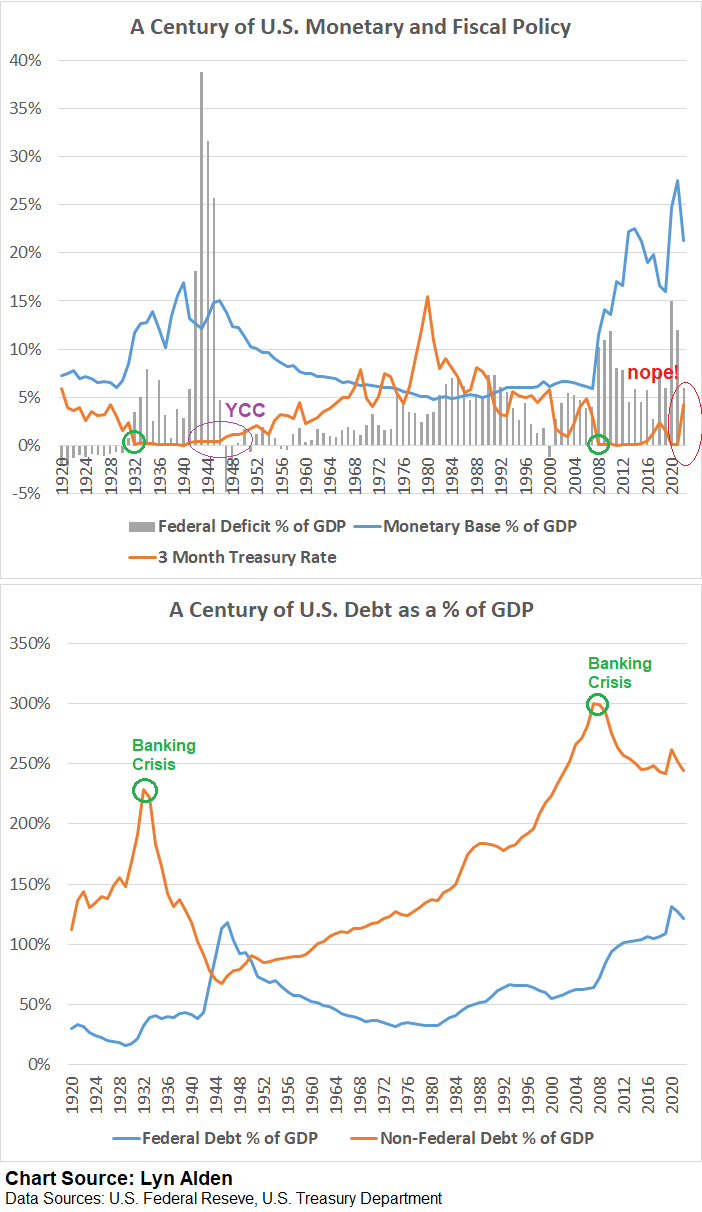

The current banking crisis is triggering more stock buybacks, and a return to Quantitative Easing with the bank bailouts, including plans to inject another $2 Trillion into the banking system, on top of the $300 billion increase in the Fed’s Balance Sheet, in just the last week. This seems counter intuitive, as QE caused inflation, but the economy is so addicted to the “Cocaine,” that is cheap money. So basically quantitative tightening is being implemented and interest rates raised to stop inflation, but as soon as the first major economic disruption of raising rates is felt, then a return to financial policies to further prop up the bubble, causing more inflation. Now the Fed is trapped with two bad options, raise rates or pivot, both of which will lead to inevitable economic doom.

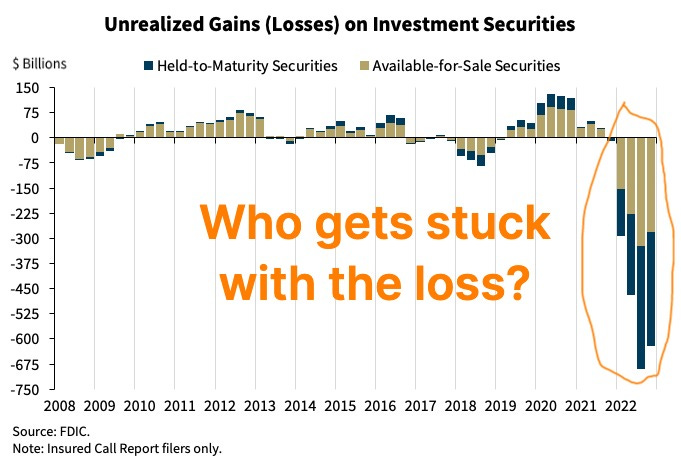

Populists can talk about nationalizing the banks into public debt free banking, and Austrian School libertarians can call for ending the Fed, and returning to a gold standard. While it is true that the Federal Reserve is a corrupt system, that is quasi private in how private banks own shares, the reality is that we are stuck with this system of relying upon the Fed’s interest rates, for the incoming economic crisis. If the Fed continues raising rates, there will be a liquidity crisis, with more bank failures. While interest rates were close to zero, banks used uninsured deposits to both invest in securities and purchase bonds, and thanks to fractional reserve banking, banks are only required to hold a fraction of deposits. So when rates rose, bonds fell in value and unrealized losses surged, so the banks were not able to pay off their depositors.

Regional banks make up about half of all US banking, so any contagion in the banking system, as people and businesses move their deposits to mega banks, deemed “too big to fail,” could trigger a Depression. One of the main reasons that the economy has not crashed sooner is because more people have been tapping into their savings and maxing out their credit cards. However, high interest rates will cause many people to default on their credit card debt, which will exacerbate the banking crisis. Not to mention Auto loans defaults wiping out credit unions, and the potential for another mortgage crisis, due to rising mortgage rates. There is a ripple effect, as far as rising interest rates being felt by debt holders, and now is just the tip of the iceberg. This could end up being a multifaceted debt crisis, in banking, corporate debt, personal debt, and government debt.

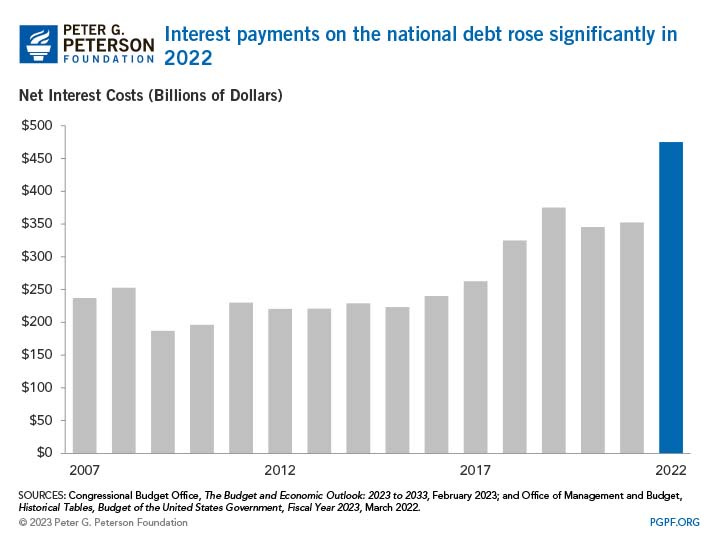

Besides the Fed likely pivoting soon due to the banking crisis, higher rates will make interest payments on the National Debt too expensive to pay off, risking a default on government debt. Overall levels of debt, both public and private, are much worse than when Fed Chair, Volcker, raised rates very high to successfully quell inflation. Any freeze in Federal spending or a default on the national debt, in response to the debt ceiling, will crash the economy, and any major extension in the debt ceiling will accelerate inflation. There is a good chance that inflation will be tolerated, with the dollar greatly devalued, to make government debt cheaper so that creditors eat the costs.

While bulls can say that this time is different from past crashes, all of the signs are pointing to this crisis being much worse than previous crashes. For instance, the economic recovery, after Volcker was done raising rates to fight inflation, was possible because of lower levels of debt, but the US has never entered a recession with debt/GDP at 125% and deficit/GDP at 7% in at least 85 years. Also the fallout of the 2008 crash was mitigated by a strong dollar, which also minimized the effects of inflation last year, but inflation will surge if the dollar is weakened. Despite signs of a pivot, the Fed has been moving much faster to fight inflation, then in the past, even with Volker. This crisis is also unique in that rates are being raised while entering a severe recession, and inflation could coincide mass layoffs. While the general assumption is that severe economic downturns are deflationary, financial commentator, Peter Schiff, makes a compelling case as for why an Inflationary Depression is a likelihood. Under this nightmare scenario, which would be much worse than even the Great Depression, inflation will negate any of the remedies that ended past crises, such as the New Deal, quantitative easing in 08, and the covid stimulus. Others signs of economic peril include, the steepest yield curve inversion since the early 80s recession, which is a barometer that has predicted just about every single recession, a major decline in ISM manufacturing sales, a big decline in savings rates, and Americans’ credit card debt approaching a record $1 Trillion.

This is the perfect storm with inflation, stagflation, recession, a potential debt crisis, as well as energy and supply chain issues. With this bubble to end all bubbles or too big to fail on steroids, the Fed has two choices, cause a liquidity crisis by shrinking the money supply, or letting inflation rip. While raising rates appears to be the least bad of these two options, further rate hikes are futile with the return of QE. A combo of QE plus interest rates having to remain high, is what could lead to that scenario of inflationary financial collapse, that Peter Schiff warned about. Though most likely it will either be long term stagflation or a deflationary Depression. This is not a hyperbole, nor clickbait, but a Depression is a very real possibility, especially if policy makers continue to kick the can down the road, to prop up the bubble.

By Robert Stark