There has been a steady migration of gold from West to East over the last three decades.

When the World Gold Council published its first Gold Demand Trends report 30 years ago, Asian demand made up 45% of the world’s total. Today, the Asian share of global gold demand is approaching 60%.

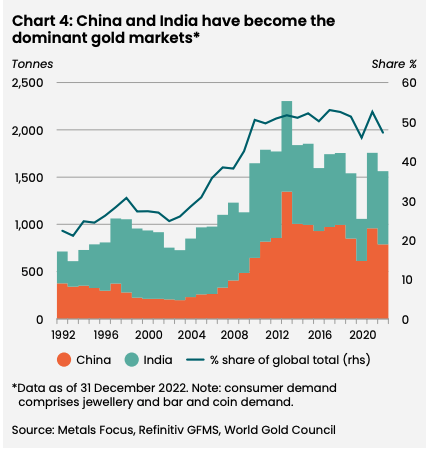

China and India have driven this migration of gold East. The World Gold Council describes the two countries as “super consumers” of gold. Thirty years ago, China and India accounted for about 20% of annual consumer gold demand. Today, the two countries make up nearly 50% of gold demand.

The Indian gold revolution started in the early to mid-1990s when government policy changes freed up the market. In 1992, gold demand in India accounted for 340 tons. In 2022, that had more than doubled to 742 tons.

India now ranks as the second-largest gold-consuming country in the world behind China.

Gold is not just a luxury in India. Even poor people buy gold in the Asian nation. According to an ICE 360 survey in 2018, one in every two households in India purchased gold within the last five years. Overall, 87% of households in the country own some amount of the yellow metal. Even households at the lowest income levels in India own some gold. According to the survey, more than 75% of families in the bottom 10% had managed to buy gold.

Indians traditionally buy and hold gold. Collectively, Indian households own an estimated 25,000 tons of gold and that number may be higher given the large black market in the country. The yellow metal is interwoven into the country’s marriage ceremonies and cultural rites. Indians also value gold as a store of wealth, especially in poor rural regions. Two-thirds of India’s gold demand comes from these areas, where most people live outside the official tax system.

We’ve seen a similar trajectory in China. The country also has played a significant cultural role in China, but through the last half of the 1900s, Chinese individuals were banned from buying gold. The government eased restrictions in the 1990s, and in 2002, the Shanghai Gold Exchange. Within two years, the market was completely liberalized.

China’s annual gold consumption rose fivefold from just over 375 tons in the early 1990s to a record high of 1,347 tons in 2013. Since then, China has ranked as the world’s largest gold-consuming country.

Economic growth has helped spur demand for gold in the East. As the World Gold Council explained, “This surge in demand was not just an expression of exuberance by Chinese investors free to buy gold. It was also driven by explosive economic growth, rapid urbanization and the desire for a simple alternative to the limited range of investments available domestically. The industry, acknowledging this desire for gold investment products, responded with innovation and speed.”

In other words, rising affluence is intersecting with the East’s traditional affinity for gold.

Turkey, Thailand and Saudi Arabia have also reported increased imports of gold in recent years.

We also see the eastward shift of gold in central bank gold buying. The biggest buyers in recent years have all been in the East. Countries steadily increasing gold reserves include China, India, Turkey, and Singapore.

We saw the migration of gold from West to East on a micro level in late 2022. Many Western investors – particularly at the institutional level – were dumping bullion. Meanwhile, Asian buyers took advantage of lower prices to snap up less expensive jewelry, coins, and bars.

According to a fall 2022 Bloomberg report, “large volumes of metal are being drawn out of vaults in financial centers like New York and heading east to meet demand in Shanghai’s gold market or Istanbul’s Grand Bazaar.”

New York and London vaults reported an exodus of more than 527 tons of gold between April and October 2022, according to data from the CME Group and the London Bullion Market Association. At the same time, gold imports into China hit a four-year high in August 2022.

In the East, many people use gold as their primary form of savings and wealth preservation. An article published by Seeking Alpha summarizes this dynamic.

For millions of people in Asia gold still is the ‘basic form of saving.’ In contrast to the West, where financialization started decades ago, and gold has slowly been removed from people their day-to-day lives. Until a financial crisis emerges, that is. In the West, people own little or no physical gold when they feel financially confident. People in the East have retained a long-term view concerning gold. Their ancestors saved in gold, and so have they been taught. With the knowledge that ultimately, gold doesn’t lose its purchasing power.”

Trying to get gold when a crisis rears its ugly head is a little like trying to get insurance when your house is on fire.

Western investors spurn gold to their own detriment.

By Michael Maharrey