“It’s Never Different This Time” – Creator Of Bond Volatility Gauge Warns Selloff Isn’t Over

Ever since the 10-year yield eclipsed 1.25% last month, the market has been eying the steady ascent in yields with trepidation. Last week, the selloff in Treasuries finally forced Jerome Powell to acknowledge the growing inflationary pressures facing the US economy.

Although tech stocks and the Nasdaq rallied back on Tuesday following a reflation-inspired rotation into ‘real economy’ stocks, many investors are bracing for bonds and stocks to continue to move lower in tandem. With volatility in equities and fixed income on the rise, RealVision invited the Convexity Maven himself, Harley Bassman, the creator of the MOVE index (a volatility gauge for bonds similar to the equity-focused VIX), to discuss Bassman’s outlook for rates and markets. Unsurprisingly, he sees more volatility, and higher convexity, ahead.

During the interview, which was conducted by Logica Capital Advisors portfolio manager and chief strategist Mike Green, Bassman explained why he feels interest rates will continue their recent trend higher as markets move recover from Fed-induced mispricing.

MIKE GREEN: Mike Green. As usual, coming from Marin County these days. Incredibly excited to have my good friend Harley Bassman back on Real Vision for– it’s been forever since you and I have had a chance to talk. Basically, the last time we talked was probably in the EQ Derivatives Conference in 2018, 2019? It’s been a long time.

Let’s talk interest rates. You are known as Mr. Convexity, you are the inventor of the MOVE index, the equivalent of the VIX for the fixed income space. In an environment in which chaos and drama dominate the interest rates space, there’s nobody that I’d rather talk to than Harley Bassman. Harley, what the hell is going on with interest rates?

HARLEY BASSMAN: Well, that’s a good question. I would say that this notion that rates are exploding higher and bad things are happening, it’s not quite the case. I would say that when 10-years were at 0.75, that was the wrong price. All we’re doing now is going to the right price as opposed to where we were before, which is the wrong price. I would push back at you. We’ve seen a significant curve steepening. I’m quite certain we’re going to talk about that today quite a bit.

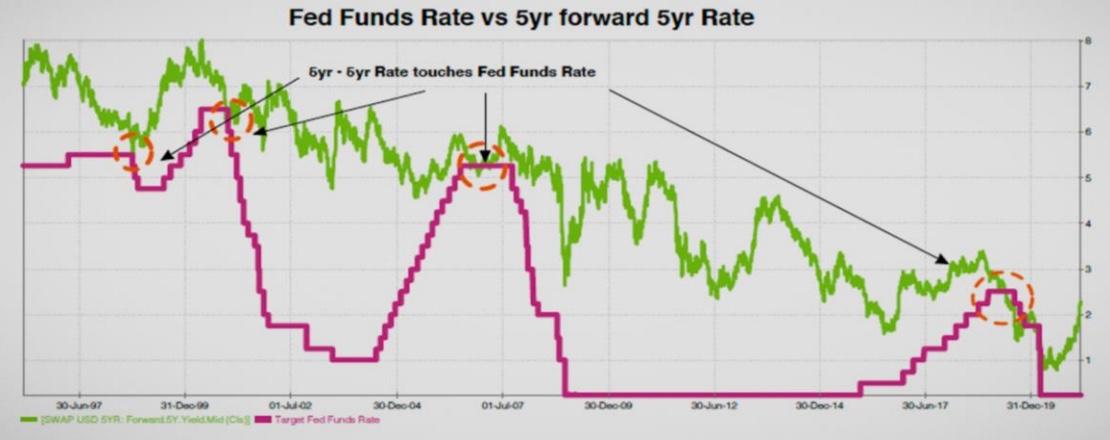

To illustrate this mis-pricing in rates, Bassman pointed to the historical relationship between the fed funds rate and a popular gauge of inflation expectations five years out.

Looking back to the period before the pandemic, Bassman and Green mused about the brief yield curve inversions that surfaced in 2019, and the fact that, as it would happen, the coronavirus-inspired recession came about less than one year later. Many economists dismissed these kinks in the yield curve as temporary phenomena, arguing that the predictive power of the yield curve only applies when inversions persist for weeks or a month or longer.

The big question, as Bassman put it: does the coronavirus-inspired global recession validate the predictive powers of the yield curve? Bassman believes the answer is yes.

MIKE GREEN: Now, this required you to develop a virus from bats and release it into China and then release it to the United States, but you managed to get the recession.

HARLEY BASSMAN: Well, what I want to ask you is, do you think this counts? I’ll go first. I say it does. Because I say whenever you get some event, especially a recession, that it’s always a surprise. By definition, a surprise is unknown. Otherwise, it wouldn’t be a surprise. Therefore, since the warning came, we could not predict what it would be, but we did get it. You’re saying that a bad virus doesn’t count. Well, I would say maybe a housing crisis doesn’t count from the last recession we had. Does this count, Mike?

Green agreed with Bassman, adding that slowing home and auto sales in the runup to the pandemic suggested that a recession was likely in the offing anyway. But was last year’s economic chaos enough to “cleanse” this dynamic? Or did the Fed only succeed in delaying the inevitable?

Following a brief discussion of convexity hedging and the Fed’s impact on the mortgage-bond market, Green and Bassman turned their attention to the outlook for Fed policy, and whether the central bank will move to cap long-term rates via yield curve control to try and prevent any harmful market ructions. In the coming months and years, Bassman believes the Fed will strive to keep front-end rates anchored as promised, while allowing long-term rates to move higher, alleviating the stress on the banking system, pension funds and other savers.

[HARLEY BASSMAN]…Certainly, volatility reduction has been a specific policy that they’ve been using. I actually think that they’re not going to do yield curve control the back end. My feeling is they’re going to hold the front end, overnight rate stays where it is, as promised, the next two years no matter the inflation number, maybe they hold 2s, maybe 5s. I think they’ll let 10s and 30s go, or at least move up. That’s not a bad thing. The government can move their funding to the front end, and the Fed could absorb it through either money printing, and we could discuss whether it’s money printing or not, what I think.

The back end going up is public policy good. A steeper curve helps the baking system. For good or for ill, we no longer do barter. We don’t use gold. We are a financial economy, and we’re highly levered. The banking system, maybe there’s bad guys in there and certainly there were villains 10 years ago who should have gone to jail, and didn’t, but the banking system is the plumbing of our financial economy, and we need to maintain it. Therefore steeper curve helps that plumbing system, so the government can do it. The Fed and fiscal policy can be more efficient.

Having a good plumbing system is good. Number two is taking the whole curve down has not been at zero cost. You’ve taken money from the lenders and given them to the borrowers. Is that a good thing? No, you’ve done a few shows on pension fund instability. If we take the back end up, that helps pension funds, that helps insurance companies. That’s a public policy good. Steepen the curve out, I’m not saying rates going from zero on the front end to 10 on the back but putting the back end at three, four or five is not a disaster, I don’t think, for the overall macro economy.

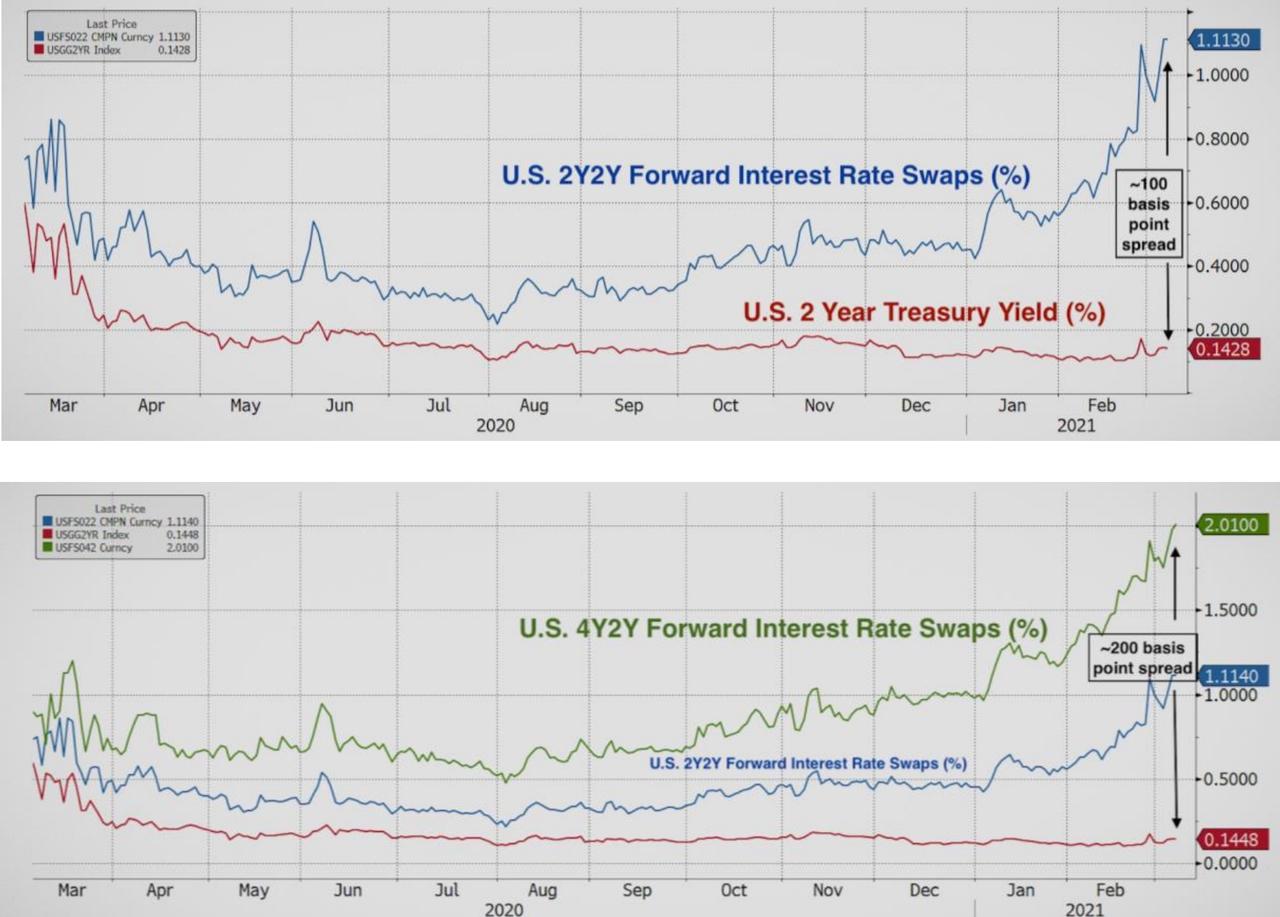

A quick look at what forward rates are doing clearly shows that, at this point, Fed tightening is already being built into the system.

But does that mean the Fed will be raising the Fed funds rate two years from now? No – in fact, Bassman believes the smarter policy would be to taper first. This would allow the curve to steepen while still keeping front-end rates anchored, which is a “better way to bring the world into line, rather than taking the front end up”, Bassman said.

As the conversation moved toward an analysis of the risks introduced by the Fed’s policy of “financial repression” – as Green termed it – the two men came to their first disagreement of the evening: whether the inevitable inflationary fallout from the Fed’s policy decisions would be “worth it.” As Bassman acknowledged that his mantra is “it’s never different this time” – a sign he has no illusions about where all of this is headed.

HARLEY BASSMAN: Circling back to our first two sentences here, it’s never different this time. That’s my mantra. It’s never different this time. I can’t explain why or how but I just do not think that we’ve reinvented human tragedy. Hubris, greed, ego. We wrote about it, the Greeks wrote about it, Shakespeare wrote about it. It just hasn’t changed, and it’s this idea that we’ve invented a new paradigm I just don’t believe it. It’s a different song, but it’s still music and I think that we’ll find some way to go and cause trouble, which is why I believe in inflation ultimately.

Is it next year? No. Is it in 20 years? I don’t know. What I do think, it’s going to happen in two to four years when the demographic bubble rolls over. We could do that later on. I think we’re going to get it because I don’t think you could print the coin of the realm at a faster pace than the overall growth of the economy without inflation at some point. Now, could it take 20 years? Why not? It took 400 years for the Roman Empire collapsed, so in the grand scheme of things, maybe not.

This policy of money printing is not going to end well. That doesn’t mean it was a bad public policy, by the way, because having the economy totally collapse either in 2009 or last year is certainly a bad idea, so maybe deferring the pain or spreading the pain out. I think that inflation is the ultimate solution. Because inflation is a beautiful tax. It taxes, everybody. It taxes them silently, and the politicians dumped a vote on it. As a tax, everyone — well, I wasn’t happy, but it’s the easiest one to live with in a democracy.

While that’s certainly one way to look at it, some listeners were put off by Bassman’s take.

I wanted to like this.

Good thing I wasn’t driving when Mr. Bassman completely lost me with these paragraphs.

Rather than attempt to address problems before they’re hopeless, it’s all gonna blow up someday, so let’s get richer now!

I hate this.https://t.co/15Fpukhk4K pic.twitter.com/jzqWTFbkzI

— Rudy Havenstein, more inclusive. (@RudyHavenstein) March 8, 2021

At any rate, readers can read the transcript of the interview below, and decide for themselves. Anybody interested in watching or listening to the interview will need to subscribe.

Tyler Durden

Sat, 03/13/2021 – 15:00

“It’s Never Different This Time” – Creator Of Bond Volatility Gauge Warns Selloff Isn’t Over

Ever since the 10-year yield eclipsed 1.25% last month, the market has been eying the steady ascent in yields with trepidation. Last week, the selloff in Treasuries finally forced Jerome Powell to acknowledge the growing inflationary pressures facing the US economy.

Although tech stocks and the Nasdaq rallied back on Tuesday following a reflation-inspired rotation into ‘real economy’ stocks, many investors are bracing for bonds and stocks to continue to move lower in tandem. With volatility in equities and fixed income on the rise, RealVision invited the Convexity Maven himself, Harley Bassman, the creator of the MOVE index (a volatility gauge for bonds similar to the equity-focused VIX), to discuss Bassman’s outlook for rates and markets. Unsurprisingly, he sees more volatility, and higher convexity, ahead.

During the interview, which was conducted by Logica Capital Advisors portfolio manager and chief strategist Mike Green, Bassman explained why he feels interest rates will continue their recent trend higher as markets move recover from Fed-induced mispricing.

MIKE GREEN: Mike Green. As usual, coming from Marin County these days. Incredibly excited to have my good friend Harley Bassman back on Real Vision for– it’s been forever since you and I have had a chance to talk. Basically, the last time we talked was probably in the EQ Derivatives Conference in 2018, 2019? It’s been a long time.

Let’s talk interest rates. You are known as Mr. Convexity, you are the inventor of the MOVE index, the equivalent of the VIX for the fixed income space. In an environment in which chaos and drama dominate the interest rates space, there’s nobody that I’d rather talk to than Harley Bassman. Harley, what the hell is going on with interest rates?

HARLEY BASSMAN: Well, that’s a good question. I would say that this notion that rates are exploding higher and bad things are happening, it’s not quite the case. I would say that when 10-years were at 0.75, that was the wrong price. All we’re doing now is going to the right price as opposed to where we were before, which is the wrong price. I would push back at you. We’ve seen a significant curve steepening. I’m quite certain we’re going to talk about that today quite a bit.

To illustrate this mis-pricing in rates, Bassman pointed to the historical relationship between the fed funds rate and a popular gauge of inflation expectations five years out.

Looking back to the period before the pandemic, Bassman and Green mused about the brief yield curve inversions that surfaced in 2019, and the fact that, as it would happen, the coronavirus-inspired recession came about less than one year later. Many economists dismissed these kinks in the yield curve as temporary phenomena, arguing that the predictive power of the yield curve only applies when inversions persist for weeks or a month or longer.

The big question, as Bassman put it: does the coronavirus-inspired global recession validate the predictive powers of the yield curve? Bassman believes the answer is yes.

MIKE GREEN: Now, this required you to develop a virus from bats and release it into China and then release it to the United States, but you managed to get the recession.

HARLEY BASSMAN: Well, what I want to ask you is, do you think this counts? I’ll go first. I say it does. Because I say whenever you get some event, especially a recession, that it’s always a surprise. By definition, a surprise is unknown. Otherwise, it wouldn’t be a surprise. Therefore, since the warning came, we could not predict what it would be, but we did get it. You’re saying that a bad virus doesn’t count. Well, I would say maybe a housing crisis doesn’t count from the last recession we had. Does this count, Mike?

Green agreed with Bassman, adding that slowing home and auto sales in the runup to the pandemic suggested that a recession was likely in the offing anyway. But was last year’s economic chaos enough to “cleanse” this dynamic? Or did the Fed only succeed in delaying the inevitable?

Following a brief discussion of convexity hedging and the Fed’s impact on the mortgage-bond market, Green and Bassman turned their attention to the outlook for Fed policy, and whether the central bank will move to cap long-term rates via yield curve control to try and prevent any harmful market ructions. In the coming months and years, Bassman believes the Fed will strive to keep front-end rates anchored as promised, while allowing long-term rates to move higher, alleviating the stress on the banking system, pension funds and other savers.

[HARLEY BASSMAN]…Certainly, volatility reduction has been a specific policy that they’ve been using. I actually think that they’re not going to do yield curve control the back end. My feeling is they’re going to hold the front end, overnight rate stays where it is, as promised, the next two years no matter the inflation number, maybe they hold 2s, maybe 5s. I think they’ll let 10s and 30s go, or at least move up. That’s not a bad thing. The government can move their funding to the front end, and the Fed could absorb it through either money printing, and we could discuss whether it’s money printing or not, what I think.

The back end going up is public policy good. A steeper curve helps the baking system. For good or for ill, we no longer do barter. We don’t use gold. We are a financial economy, and we’re highly levered. The banking system, maybe there’s bad guys in there and certainly there were villains 10 years ago who should have gone to jail, and didn’t, but the banking system is the plumbing of our financial economy, and we need to maintain it. Therefore steeper curve helps that plumbing system, so the government can do it. The Fed and fiscal policy can be more efficient.

Having a good plumbing system is good. Number two is taking the whole curve down has not been at zero cost. You’ve taken money from the lenders and given them to the borrowers. Is that a good thing? No, you’ve done a few shows on pension fund instability. If we take the back end up, that helps pension funds, that helps insurance companies. That’s a public policy good. Steepen the curve out, I’m not saying rates going from zero on the front end to 10 on the back but putting the back end at three, four or five is not a disaster, I don’t think, for the overall macro economy.

A quick look at what forward rates are doing clearly shows that, at this point, Fed tightening is already being built into the system.

But does that mean the Fed will be raising the Fed funds rate two years from now? No – in fact, Bassman believes the smarter policy would be to taper first. This would allow the curve to steepen while still keeping front-end rates anchored, which is a “better way to bring the world into line, rather than taking the front end up”, Bassman said.

As the conversation moved toward an analysis of the risks introduced by the Fed’s policy of “financial repression” – as Green termed it – the two men came to their first disagreement of the evening: whether the inevitable inflationary fallout from the Fed’s policy decisions would be “worth it.” As Bassman acknowledged that his mantra is “it’s never different this time” – a sign he has no illusions about where all of this is headed.

HARLEY BASSMAN: Circling back to our first two sentences here, it’s never different this time. That’s my mantra. It’s never different this time. I can’t explain why or how but I just do not think that we’ve reinvented human tragedy. Hubris, greed, ego. We wrote about it, the Greeks wrote about it, Shakespeare wrote about it. It just hasn’t changed, and it’s this idea that we’ve invented a new paradigm I just don’t believe it. It’s a different song, but it’s still music and I think that we’ll find some way to go and cause trouble, which is why I believe in inflation ultimately.

Is it next year? No. Is it in 20 years? I don’t know. What I do think, it’s going to happen in two to four years when the demographic bubble rolls over. We could do that later on. I think we’re going to get it because I don’t think you could print the coin of the realm at a faster pace than the overall growth of the economy without inflation at some point. Now, could it take 20 years? Why not? It took 400 years for the Roman Empire collapsed, so in the grand scheme of things, maybe not.

This policy of money printing is not going to end well. That doesn’t mean it was a bad public policy, by the way, because having the economy totally collapse either in 2009 or last year is certainly a bad idea, so maybe deferring the pain or spreading the pain out. I think that inflation is the ultimate solution. Because inflation is a beautiful tax. It taxes, everybody. It taxes them silently, and the politicians dumped a vote on it. As a tax, everyone — well, I wasn’t happy, but it’s the easiest one to live with in a democracy.

While that’s certainly one way to look at it, some listeners were put off by Bassman’s take.

I wanted to like this.

Good thing I wasn’t driving when Mr. Bassman completely lost me with these paragraphs.

Rather than attempt to address problems before they’re hopeless, it’s all gonna blow up someday, so let’s get richer now!

I hate this.https://t.co/15Fpukhk4K pic.twitter.com/jzqWTFbkzI

— Rudy Havenstein, more inclusive. (@RudyHavenstein) March 8, 2021

At any rate, readers can read the transcript of the interview below, and decide for themselves. Anybody interested in watching or listening to the interview will need to subscribe.

Tyler Durden

Sat, 03/13/2021 – 15:00

Read More