Luongo: Capital Is Sensing “This Central Bank Impotency”

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

I don’t know what’s more ludicrous at this point, the amount of central bank intervention or the whining from the markets that there isn’t enough.

We’re headed for the mother of all financial crises and from my chair I can’t for the life of me understand how so many smart market analysts can’t see the way it’s being engineered right in front of their eyes.

Despite the headlines and the ocean of money beginning to flood the landscape from the Fed and the Treasury dept. the Fed wasn’t “uber-dovish” on Wednesday. If anything, FOMC Chair Jerome Powell didn’t give the markets what it wanted at all.

All the Fed did was say we’re going to keep doing what isn’t working until 2023 despite what the bond market thinks we should do. Oh, and we’ll make potential credit lines to the banks deeper.

The response was typical. Everything was golden. Taco Tuesday’s are back on the menu and the Fed has our backs.

Because for a brief few hours the algorithms scanned the headlines and reacted accordingly. The weak dollar is here.

It’s like McDonald’s brought back the McRib for and extra two months or something.

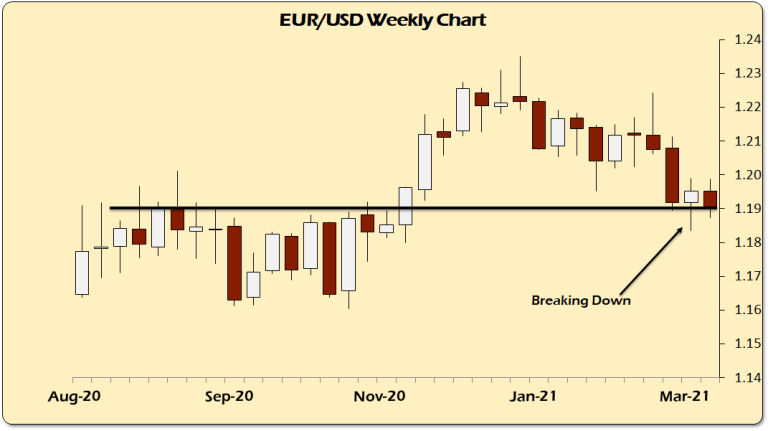

But then Thursday happened and reality took over. The euro dumped, gold gave back its gains. The 10-year treasury note spiked to 1.75%. German 10-year bunds pushed back to -0.265% very much against the will of the ECB and President Christine Lagarde who tried to quell the panic brewing in Europe with talk of more bond buying.

Do you think it worked?

In my opinion Lagarde panicked last week. There was nothing really spooking the bond markets at that point but she went there anyway because of the downward pressure on the euro, which is also tied to the falling Japanese yen.

Lagarde was hoping that the ninetieth time would be the charm, I guess. That’s the typical ECB move, announce an expansion of its alphabet soup mattress stuffing programs for worthless eurobond debt and let the momo-monkeys front run the trade to pick up nickels in front of a freight train.

But that didn’t happen (see chart of German bunds above). That trade lasted about an hour or two. And this week we get a close above last week’s high. Higher yields are incoming quick in Europe and Lagarde just shot her wad.

The yen fell further prompting Bank of Japan President Kuroda to bang his shoe on the table and whine about more YCC — Yield Curve Control.

“We won’t tolerate yield fluctuations that would have an impact on our monetary easing,”

Bad markets, no sushi.

This is the problem with central planners. Hubris. Kuroda can no more control the yield curve indefinitely than I can leap tall buildings in a single bound. And the impotent rage carried by Kuroda’s statement is something you better get used to in the coming months, because there’s going to be a lot of that in the halls of the central banks.

Does that statement inspire confidence in you?

Because that’s the heart of the entire central bank two-step, confidence. Confidence that they have the tools and the power to hold back the forces of a chaotic-dynamic market. The problem is they are like Aquaman in the Snyder Cut, holding back a flood that is rapidily enveloping them.

Lagarde and company are desperately trying to hold the euro up. Only a big intervention Friday morning kept the close above $1.19, but just barely.

All of this is pointing towards a much stronger dollar not a weaker one. The central banks keep trying to reflate an economy that is deflating. Inflation is roaring back in base commodities. You know, those things people actually need to survive – food, energy, etc.

As Zerohedge and BofA point out inflation is here and supply chains are breaking down all over the economy and the central banks are terrified of runaway inflation, apparently. But the problem is it’s the wrong kind of inflation!

The central bankers always want to pat themselves on their post-Keynesian backs about how they’ve stimulated aggregate demand. That they’re creating demand-pull inflation. That’s great. But it’s not true. Aggregate demand is a chimera. It doesn’t exist. Aggregate demand of what? Money? Oil? Labor? Porn?

The economy is trillions of transactions sending signals of time preference by humans acting in the moment.

And in all the verbiage about the central bank response to this no one wants to admit that we don’t have rising aggregate demand pulling prices higher, we have more money chasing fewer goods which can’t be produced and delivered economically.

Those costs, which are rising from the bottom up, are pushing prices higher.

And if anyone admits this confidence in the central banks collapses overnight. And the key to the Great Reset is maintaining the credibility of the central banks while sacrificing the commercial banks on the altar of debt forgiveness.

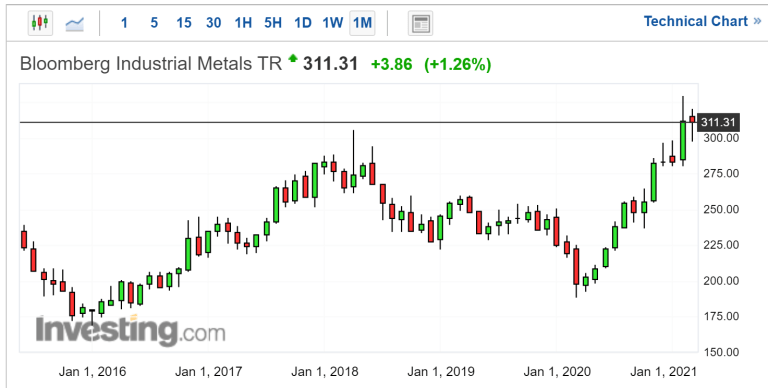

The industrial metals markets have been on fire for nearly a year now. Wholesale gasoline has more than doubled since Biden was declared the winner of the election. Does anyone wonder why copper is steadfastly over $4/lb? Or is that just a glitch in the Matrix? What about Nickel? Lumber? Iron Ore? Lead?

In case you’re too lazy to look these prices up here’s your sign:

Ye gods I hate to sound like a broken record here but the situation is obvious. There is no reflation trade. There’s just a bunch of credit sloshing around trying to figure out where to go.

And the question I have for all of you today is, “Has this been deliberate?”

Powell knew what he was doing with his last two missed opportunities to intervene as the bond markets were screaming at him to do. I don’t think he’ll move until the 10 year crosses 2% with vigor. But, he’s laid the groundwork in anticipation of the banks refusing to lend to each other.

He also couldn’t do anything here or he would have looked as spooked as Lagarde did last week. For now he has to let Europe, Japan and emerging markets flounder.

I don’t know that Lagarde understands she’s panicking the Eurobond markets with increased QE while the European Union dithers over COVID-19 relief spending that may make it out of the bureaucratic maze by the end of the year. But I can tell you she doesn’t give a rat’s ass.

Kuroda knows that everything about Japan’s macroeconomy is dead.

The world is biblically short U.S. dollars still and Joe Biden’s diplomatic corps, to be undeservedly generous, looks like it is deliberately inviting a confrontation with Russia and China. I mean, in all my years of watching foreign policy I never thought I’d pine for the days of Mike “The Buffet King” Pompeo and John “Legal Pad Bombardier” Bolton.

But here we are.

By the way, do you think this type of sabre rattling is dollar negative or positive? Askin’ for a friend.

So, if the whole thing is going to crash, why not just let it while trying to salvage as much credibility as possible?

And it seems to me that capital is sensing this central bank impotency (feigned or otherwise) and is testing them while shoring up their dollar reserves now.

At the same time money is flooding into the crypto-space as a real safe-haven asset. Those trying to protect themselves are running into Bitcoin and Ethereum parking capital for yield in a yield-free world thanks to the explosion in DeFi.

Bitcoin rallied on Powell’s punt which if it is an anti-dollar asset like gold it should have sold off further. That it didn’t and rallied back towards $60,000 is your clue that there is real fear and the headlines can’t control it.

Honestly, the speed at which the Non-Fungible Token market has captured people’s attention is about the only real evidence I can find of bubble-like behavior in crypto that reminds me of the ICO Rush of 2017.

You can’t Build everything Back Better if you don’t first destroy everything. And you can’t destroy everything financially if you don’t first create the mother of all dollar short squeezes. To underscore just how bad things are the IRS extended tax day out to May 17th because the stimmy checks haven’t shown up yet for people to pay their taxes with.

I’d say that was the most ludicrous thing I’ve heard this week, but then I checked Twitter to see #RootinForPutin trending. If this is the acme of U.S. political strategic decision making right now then I don’t see how we avoid the crash that’s coming.

* * *

Join my Patreon if you want to avoid the crashing tide destroying your boat

Donate via Crypto

BTC: 3GSkAe8PhENyMWQb7orjtnJK9VX8mMf7Zf

BCH: qq9pvwq26d8fjfk0f6k5mmnn09vzkmeh3sffxd6ryt

DCR: DsV2x4kJ4gWCPSpHmS4czbLz2fJNqms78oE

LTC: MWWdCHbMmn1yuyMSZX55ENJnQo8DXCFg5k

DASH: XjWQKXJuxYzaNV6WMC4zhuQ43uBw8mN4Va

XMR: 48Whbhyg8TNXiNV2LNkjeuJJU55CNt5m1XDtP3jWZK2xf5GNsbU2ZwHLDJTQ5oTU3uaJPN8oQooRpSQ2CPMJvX8pVTqthmu

Tyler Durden

Sun, 03/21/2021 – 10:00

Luongo: Capital Is Sensing “This Central Bank Impotency”

Authored by Tom Luongo via Gold, Goats, ‘n Guns blog,

I don’t know what’s more ludicrous at this point, the amount of central bank intervention or the whining from the markets that there isn’t enough.

We’re headed for the mother of all financial crises and from my chair I can’t for the life of me understand how so many smart market analysts can’t see the way it’s being engineered right in front of their eyes.

Despite the headlines and the ocean of money beginning to flood the landscape from the Fed and the Treasury dept. the Fed wasn’t “uber-dovish” on Wednesday. If anything, FOMC Chair Jerome Powell didn’t give the markets what it wanted at all.

All the Fed did was say we’re going to keep doing what isn’t working until 2023 despite what the bond market thinks we should do. Oh, and we’ll make potential credit lines to the banks deeper.

The response was typical. Everything was golden. Taco Tuesday’s are back on the menu and the Fed has our backs.

Because for a brief few hours the algorithms scanned the headlines and reacted accordingly. The weak dollar is here.

It’s like McDonald’s brought back the McRib for and extra two months or something.

But then Thursday happened and reality took over. The euro dumped, gold gave back its gains. The 10-year treasury note spiked to 1.75%. German 10-year bunds pushed back to -0.265% very much against the will of the ECB and President Christine Lagarde who tried to quell the panic brewing in Europe with talk of more bond buying.

Do you think it worked?

In my opinion Lagarde panicked last week. There was nothing really spooking the bond markets at that point but she went there anyway because of the downward pressure on the euro, which is also tied to the falling Japanese yen.

Lagarde was hoping that the ninetieth time would be the charm, I guess. That’s the typical ECB move, announce an expansion of its alphabet soup mattress stuffing programs for worthless eurobond debt and let the momo-monkeys front run the trade to pick up nickels in front of a freight train.

But that didn’t happen (see chart of German bunds above). That trade lasted about an hour or two. And this week we get a close above last week’s high. Higher yields are incoming quick in Europe and Lagarde just shot her wad.

The yen fell further prompting Bank of Japan President Kuroda to bang his shoe on the table and whine about more YCC — Yield Curve Control.

“We won’t tolerate yield fluctuations that would have an impact on our monetary easing,”

Bad markets, no sushi.

This is the problem with central planners. Hubris. Kuroda can no more control the yield curve indefinitely than I can leap tall buildings in a single bound. And the impotent rage carried by Kuroda’s statement is something you better get used to in the coming months, because there’s going to be a lot of that in the halls of the central banks.

Does that statement inspire confidence in you?

Because that’s the heart of the entire central bank two-step, confidence. Confidence that they have the tools and the power to hold back the forces of a chaotic-dynamic market. The problem is they are like Aquaman in the Snyder Cut, holding back a flood that is rapidily enveloping them.

Lagarde and company are desperately trying to hold the euro up. Only a big intervention Friday morning kept the close above $1.19, but just barely.

All of this is pointing towards a much stronger dollar not a weaker one. The central banks keep trying to reflate an economy that is deflating. Inflation is roaring back in base commodities. You know, those things people actually need to survive – food, energy, etc.

As Zerohedge and BofA point out inflation is here and supply chains are breaking down all over the economy and the central banks are terrified of runaway inflation, apparently. But the problem is it’s the wrong kind of inflation!

The central bankers always want to pat themselves on their post-Keynesian backs about how they’ve stimulated aggregate demand. That they’re creating demand-pull inflation. That’s great. But it’s not true. Aggregate demand is a chimera. It doesn’t exist. Aggregate demand of what? Money? Oil? Labor? Porn?

The economy is trillions of transactions sending signals of time preference by humans acting in the moment.

And in all the verbiage about the central bank response to this no one wants to admit that we don’t have rising aggregate demand pulling prices higher, we have more money chasing fewer goods which can’t be produced and delivered economically.

Those costs, which are rising from the bottom up, are pushing prices higher.

And if anyone admits this confidence in the central banks collapses overnight. And the key to the Great Reset is maintaining the credibility of the central banks while sacrificing the commercial banks on the altar of debt forgiveness.

The industrial metals markets have been on fire for nearly a year now. Wholesale gasoline has more than doubled since Biden was declared the winner of the election. Does anyone wonder why copper is steadfastly over $4/lb? Or is that just a glitch in the Matrix? What about Nickel? Lumber? Iron Ore? Lead?

In case you’re too lazy to look these prices up here’s your sign:

Ye gods I hate to sound like a broken record here but the situation is obvious. There is no reflation trade. There’s just a bunch of credit sloshing around trying to figure out where to go.

And the question I have for all of you today is, “Has this been deliberate?”

Powell knew what he was doing with his last two missed opportunities to intervene as the bond markets were screaming at him to do. I don’t think he’ll move until the 10 year crosses 2% with vigor. But, he’s laid the groundwork in anticipation of the banks refusing to lend to each other.

He also couldn’t do anything here or he would have looked as spooked as Lagarde did last week. For now he has to let Europe, Japan and emerging markets flounder.

I don’t know that Lagarde understands she’s panicking the Eurobond markets with increased QE while the European Union dithers over COVID-19 relief spending that may make it out of the bureaucratic maze by the end of the year. But I can tell you she doesn’t give a rat’s ass.

Kuroda knows that everything about Japan’s macroeconomy is dead.

The world is biblically short U.S. dollars still and Joe Biden’s diplomatic corps, to be undeservedly generous, looks like it is deliberately inviting a confrontation with Russia and China. I mean, in all my years of watching foreign policy I never thought I’d pine for the days of Mike “The Buffet King” Pompeo and John “Legal Pad Bombardier” Bolton.

But here we are.

By the way, do you think this type of sabre rattling is dollar negative or positive? Askin’ for a friend.

So, if the whole thing is going to crash, why not just let it while trying to salvage as much credibility as possible?

And it seems to me that capital is sensing this central bank impotency (feigned or otherwise) and is testing them while shoring up their dollar reserves now.

At the same time money is flooding into the crypto-space as a real safe-haven asset. Those trying to protect themselves are running into Bitcoin and Ethereum parking capital for yield in a yield-free world thanks to the explosion in DeFi.

Bitcoin rallied on Powell’s punt which if it is an anti-dollar asset like gold it should have sold off further. That it didn’t and rallied back towards $60,000 is your clue that there is real fear and the headlines can’t control it.

Honestly, the speed at which the Non-Fungible Token market has captured people’s attention is about the only real evidence I can find of bubble-like behavior in crypto that reminds me of the ICO Rush of 2017.

You can’t Build everything Back Better if you don’t first destroy everything. And you can’t destroy everything financially if you don’t first create the mother of all dollar short squeezes. To underscore just how bad things are the IRS extended tax day out to May 17th because the stimmy checks haven’t shown up yet for people to pay their taxes with.

I’d say that was the most ludicrous thing I’ve heard this week, but then I checked Twitter to see #RootinForPutin trending. If this is the acme of U.S. political strategic decision making right now then I don’t see how we avoid the crash that’s coming.

* * *

Join my Patreon if you want to avoid the crashing tide destroying your boat

Donate via Crypto

BTC: 3GSkAe8PhENyMWQb7orjtnJK9VX8mMf7Zf

BCH: qq9pvwq26d8fjfk0f6k5mmnn09vzkmeh3sffxd6ryt

DCR: DsV2x4kJ4gWCPSpHmS4czbLz2fJNqms78oE

LTC: MWWdCHbMmn1yuyMSZX55ENJnQo8DXCFg5k

DASH: XjWQKXJuxYzaNV6WMC4zhuQ43uBw8mN4Va

XMR: 48Whbhyg8TNXiNV2LNkjeuJJU55CNt5m1XDtP3jWZK2xf5GNsbU2ZwHLDJTQ5oTU3uaJPN8oQooRpSQ2CPMJvX8pVTqthmu

Tyler Durden

Sun, 03/21/2021 – 10:00

Read More