House of Cards

The data that got some heads, and markets, turning yesterday was US new home sales, which slumped 16.6% m-o-m and 26.9% y-o-y to a seasonally adjusted annual rate of 591,000 in April, the lowest level since April 2020. Economists had expected a figure of 748,000. Yes, this is always a very choppy series, but the drop was widespread: -5.9% in the Northeast, -15.1% in the Midwest, -19.8% in the South, and -13.8% in the West.

That’s synchronicity which takes me back to a conversation I had with a Russian-American in mid-2006 when working at another bank, who explained why the US housing market was so vast that it was mathematically impossible for all homes to ever do anything –bad!– at the same time, and so US mortgage-backed securities were the safest of investments. I kept up a rictus grin, as at that time I had been writing for years about a looming US housing crash, the Western replay of Asia’s 1997 crisis, which the traders around me were disinterested in hearing about: they had brought the guy in to explain how to profit from MBS sales.

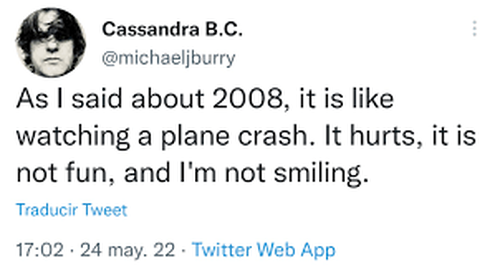

Relatedly, today has seen Michael Burry, of ‘The Big Short’ fame, tweet: ‘As I said about 2008, it is like watching a plane crash. It hurts, it is not fun, and I’m not smiling.’ Once again I agree with him.

Of course, there was no sign of a property slump in the April sales report – quite the opposite. Prices soared yet again, reaching a median of $450,600 vs. $435,000 in the prior month. That is 3.6% m-o-m, which is 43% y-o-y if you annualized(!) That is a trend that has been going on for some time: according to First American’s chief economist, in April 2021, 25% of new-home sales were priced below $300,000, but in April 2022, only 10% of new home sales were. This is part of ‘the strong economy’ the Fed keeps talking about, which is very 1997/2008 redux – as is their inability to understand what is actually going on (again). Let’s see what their minutes say much later today.

However, we are certainly not seeing the same supply and price surge as before the last US housing crash. Inventory of homes for sale rose to 9 from 6.9 months on the back of that April sales fall, but there is not anywhere near the same scale of construction being seen as before the last crash. Lessons have been learned on that front, perhaps.

Regardless, this does not mean good things for home buyers. Business Insider quotes a TD Bank survey of more than 1,000 hopeful buyers which found 29% were uncertain whether now was a good time to purchase a home, with affordability (67%) and down-payments (46%) the biggest concerns. Only 36% of this year’s prospective homebuyers believed now was a good time to buy vs. 59% in 2021 and 68% in 2020. Likewise, the 30-year US fixed-rate mortgage jumped above 5% in April for the first time since February 2011, and averaged 5.25% in the week ending May 19.

So, the logical economist forecast must be that prices have to come down – right? Except they can’t.

There is massive supply-side inflation in almost everything involved in building a home, and outright limits on availability of some items regardless of price. That trend is not reversing any time soon and could get worse depending on energy prices and Chinese lock downs. Meanwhile, all those would-be home buyers have to rent. That pushes up rents, which are by definition rent-seeking; and that pushes up US inflation because of how the CPI basket is calculated.

So, the next logical economist forecast must be that interest rates have to come down – right? Except they can’t either.

If they do, they will try to shift the demand curve to the right just as the supply curve remains shifted to the left, with inflation already far too high. Crucially, the ceiling for rates may be far lower than 7.5%, 8.3%, or 10% y-o-y headline inflation suggests should be the case because of the demand side; but the floor for where rates will go is also far higher because of the supply side. If one is presuming rates can fall far and fast, then the implied collapse in demand is so bad one should be making those calls from a bunker – which, full disclosure, is not something I am opposed to in principle. I think Burry would concur.

Moreover, as I keep repeating, governments will not just sit there and do nothing: but their actions will shift supply curves to the left, and demand curves to the right.

On the demand side, will Australia’s new government do what every other one has done, and try to shoehorn people into unaffordable houses – perhaps with another cash giveaway from all taxpayers, including renters, directly to home buyers (which actually means home sellers)?

On the demand side, China just agreed to buy Brazilian corn for the first time; hooray for Brazil, and welcome to higher corn prices for former buyers of that crop if China does what it usually does and stocks up aggressively (for whatever political or geopolitical reason).

On the supply side, India just banned the export of sugar following the same on wheat, complicating global agri trading even more, and helping to push up prices elsewhere. There is likely to be much more of this to come all over – high prices now create incentives to hoard, not export, inverting usual economic logic.

On the supply side, US shale firms are using profits to pay down debt or buy back shares rather than drill, baby, drill because of the White House’s aversion to fossil fuels. The Saudis insist on keeping Russia as a member of OPEC+ and are refusing their role as swing producer for the US in time of need (though talks over the Straits of Tiran and President Biden killing off the Iran Deal by refusing to delist the IRGC as terrorists might indicate a belated diplomatic pivot by the States). Anyway, a supply-side lack of refineries is a pressing structural problem there is simply no short or medium-term solution to.

On the demand side, the EU *may* be closer to a Russian oil embargo – although it is unclear if Hungary declaring a state of emergency overnight, allowing PM Orban to rule by decree, is a sign that this is closer or much, much further away, and/or if the EU is in trouble.

Yes, the real-world impact of this is simply shattering on demand. UK consumers, already facing surging energy bills, have just been told the cap on what they can pay is to rise again this autumn, with expectations the average household bill could hit a staggering £2,800, up another £800, pushing millions more into fuel poverty. Totally unrelated to fresh images of PM Johnson quaffing alcohol at lockdown parties in No 10 Downing Street, the UK Chancellor is expected to introduce a windfall tax on energy companies and energy subsidies for households as soon as tomorrow. That is welcome – but means higher inflation, not only in the short term, but in terms of the shift in psychology towards expectations of such interventions.

As someone who has lived in emerging markets and their crashes for years, not just the 2008 western one, the simple message is that there are times when demand collapses and interest rates have to be high anyway. (The RBNZ meet today, and the market suspects we will see another 50bp hike.) There are also times when the government steps in and makes things better,… and times when it steps in and makes things worse.

One can have recession, high inflation, a weak currency, and high interest rates all at the same time. One can see stocks collapse and bonds yield massively negative real returns, and cash lose its value due to inflation. And crypto do a ‘Luna’. And gold do nothing versus the US dollar.

In such times, think not of pyramid schemes, but of Maslow’s pyramid. Which is what commodity hoarders and subsidizing governments are doing.

Meanwhile, along similar lines, as China and Russia carry out joint air-force patrols, George “Emmanuel Goldstein” Soros, looking even more like a walnut than Henry “Give Russia and China all of the things” Kissinger, warns Davos of the risks of ‘World War Three’ on one stage… as New York Stock Exchange executives boast of how many more Chinese firms they expect to list there in the future on another. ¯_(ツ)_/¯

The BBC carries another explosive expose on China’s alleged treatment of its Uighur minority just as the UN human rights chief Bachelet visits Xinjiang, prompting the US to lash out… at the UN.

The Quad, meeting yesterday, initiated further measures to address Indo-Pacific economic security, including joint action to track illegal Chinese fishing, as China’s diplomats are on a whistle-stop tour through Pacific nations to see which of them might like a shiny new air or naval base.

As flagged, US Trade Representative Tai also pointed out after the Biden tariffs hullabaloo that it was in the US interest to be “strategic” over removing tariffs – even if it sounds like she was lobbying her own government. Relatedly, we get US Secretary of State Blinken speaking on US China policy tomorrow, with early suggestions there will be no new developments – which is already seeing Congress lobby their own government for more hawkish action.

None of these developments ease global tensions, suggest a rapid move back to ‘normal’ economics and lower inflation, or a true return to the pre-Covid market ‘new normal’, even if we get awful economic data. They collectively look a lot like ‘House of Cards’. Just as much as the economy, as Burry implies.

Michael Every of Rabobank