Oil To $300?

“We see a shift from stigmatization toward criminalization of investing in higher oil production.” – Bob McNally, former White House official, “This Time Is Different” Bloomberg May 30, 2021

“From today, halt all investment in new fossil fuel supply projects and make no further final investment decisions for new unabated coal plants.” – IEA Roadmap to Net Zero by 2050

Whether you think global warming is a hoax and no technology has done more to uplift billions of people out of abject poverty than the harnessing of fossil fuels, or you think the burning of fossil fuels is irreversibly destroying the planet and urgent action to halt their use should be the top priority of humankind, or even if you think both of these things, this article is for you.

I can assure all sides the following: unless something substantial changes – and soon – the price of oil is going way higher. Is $300 oil probable? Perhaps not, but it makes for excellent clickbait. Is $300 oil impossible? Absolutely not.

Consider some history.

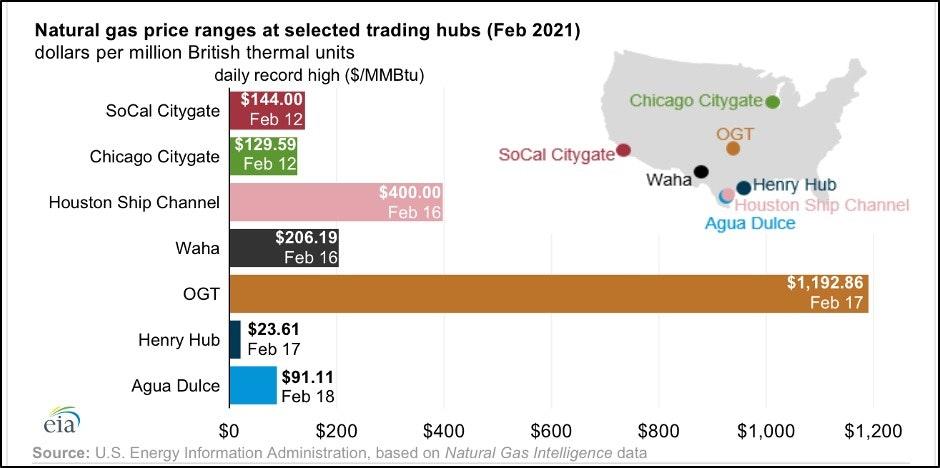

In the third week of February, 2021, a massive cold snap impacted much of the Lower 48 states. The power grid in Texas nearly collapsed. Just as demand for heating and power was reaching its most desperate apex, the supply of natural gas collapsed. The infrastructure simply couldn’t handle the depths of the freeze. The result? Prices of natural gas at several large trading hubs across the US skyrocketed to unthinkable levels. This chart from the US Energy Information Administration captures it well:

So how can we compare these prices to the price of oil? One of the problems with comparing quoted prices for different sources of energy is they are priced in different units, which is mostly an accident of history. For example, natural gas is priced in dollars per million British thermal units (BTUs), whereas oil is priced in dollars per barrel (a barrel being 42 gallons), and gasoline is priced in dollars per gallon (a gallon being a gallon). Habits are hard to break.

To create an apples-to-apples comparison of what these prices mean, a useful trick is to first levelize everything to millions of BTUs, which is how natural gas is sold anyway, and it just happens to be a direct measure of the inherent energy content embedded in a fuel. A standard barrel of oil contains 5.8 million BTUs. If you take the current price of oil (in dollars per barrel) and divide it by the current price of natural gas (in million BTUs), you’ll almost always get a number higher than 5.8, which makes sense because oil is generally more useful than natural gas and natural gas is often a byproduct of oil production. But on an energy-content-equivalency basis, 5.8 is the number. To put natural gas prices into an energy-contained-in-oil-equivalency basis, we simply do the reverse and multiply the price of natural gas, expressed in millions of BTUs, by 5.8.

We are now ready to put the prices for natural gas in the chart above into shocking context. On an energy-contained-in-oil-equivalency basis, natural gas prices reached the following levels in February:

SoCal Citygate: $835 per barrel

Chicago Citygate: $752 per barrel

Houston Ship Channel: $2,320 per barrel

Waha: $1,196 per barrel

OGT: $6,919 per barrel

Henry Hub: $137 per barrel

Agua Dulce: $528 per barrel

Do I have your attention?

Sure, the price of natural gas didn’t stay there, but it went there. I use this extreme example to illustrate an important point. Fossil fuels are hugely inelastic commodities. Shortages send prices soaring because they are needed and there are not yet fungible substitutes. Society might hate fossil fuels, it might even hate them for very good reasons, but society is trapped in its need for fossil fuels, at least for the time being.

We can’t escape fossil fuels without significantly higher prices. Higher prices will level the playing field for alternative technologies by making them more competitive. Higher prices will spur significant investment in new energy R&D. Higher prices will also be the only way to motivate society to cut fossil fuel use. Said another way, fossil fuels are so useful for humankind that they will never be substituted unless prices skyrocket. Higher prices it shall be. The only way out is through.

There are at least four forces aligning as huge tail winds for fossil fuel prices. First, and most important, the ESG/progressive crowd has utterly and totally won the narrative war and they will press the consequence of their undeniable victory to the maximum by attacking supply at every opportunity. Second, the fossil fuel industry is coming off a period of extended underinvestment in capital projects already, which was exacerbated by the fallout from the COVID-19 crisis. Third, massive monetary and fiscal stimulus is stoking demand for commodities globally, and fossil fuels will not be exempt (on the contrary, since fossil fuels are critical to the production of other commodities, they will feel an amplified effect of this phenomenon). Finally, and related to the third force, fiat currencies are being debased at an unprecedented rate.

In this post, I’ll only focus on the first. Larry Fink, chairman and CEO of Blackrock, is not a trained scientist. He has no particular expertise in environmental issues. He holds a BA in political science and an MBA in real estate, both from UCLA. There’s nothing wrong with these degrees, and he has parlayed them into astonishing business success. But Larry is now in charge of global oil policy. There shall be less drilling, less exploring, less permitting, and less capital spending, period. Larry has decided to make it so, and it shall be.

You can celebrate this (yay!) or bemoan this (boo!), but the one thing you can’t do is deny it. Don’t believe me? Ask the CEO of Exxon Mobil. Memo to Darren Woods: You now work for Larry, and Larry is calling the shots – his shots. Larry wouldn’t really mind $10 gasoline. It’s not like he has driven himself in decades, nor is he up for reelection, at least I don’t think he is. I certainly don’t remember voting for him. Oh – and don’t feel too bad for Darren, he is about to go from stupid rich to crazy stupid rich. Not quite Larry crazy stupid rich, but close enough for you and me.

Now for the fun part. How high can oil go?

Clearly, this chicken strongly believes all the pieces are in place for oil to make new all-time high. But what does this mean? In July 2008, the price of oil peaked at $145 a barrel, but that’s in nominal terms. A dollar today, 13 years later, does not have the same purchasing power as a dollar then. If we use the official Consumer Price Index (CPI) inflation rate of approximately 2%, the actual all-time high for oil in today’s dollars is closer to $190 a barrel. What if, as most sound-minded people believe, the government has been systematically underestimating inflation in the official numbers for decades? If you believe the real inflation rate has been 4% since 2008, the new peak oil price becomes $240 a barrel. At 6%, it becomes $310 a barrel.

Have we experienced 6% inflation per year since 2008? According to shadowstats.com, if you merely calculate CPI the way the government used to in 1990, you get an average inflation rate over this period near that number. If you calculate CPI the way the government used to in 1980, it approaches 10%. It should be noted that when the US government changes its inflation calculation methodologies, it never seems to lead to higher reported numbers. I wonder why that is?

Let’s look at it another way. Assume you believe, like I do, that gold is the only real money. How much gold buys you a barrel of oil? Today, it is a shockingly low amount – only 0.036 ounces. Yes, you read that correctly. Roughly 1 gram of gold does the trick. When oil was trading at $145 in mid-2008, its price in gold was 0.15 ounces. With gold now trading at $1,900 an ounce, that works out to about $285 a barrel oil.

Does $300 seem like clickbait now?

Look, I know what you are thinking. “On the one hand, this chicken is making a lot of sense. On the other hand, I’m reading a blog written by a chicken on Substack. How seriously can I take this stuff?”

I’ll leave you with this. If Bloomberg is flippantly dropping criminalization quotes in above-the-fold news articles detailing a sea change in how people with the real power in our society are viewing the fossil fuel industry, it’s best you sit up, pay attention, and prepare accordingly.

Tyler Durden

Fri, 06/04/2021 – 13:15

Oil To $300?

By Doomsberg Substack

“We see a shift from stigmatization toward criminalization of investing in higher oil production.” – Bob McNally, former White House official, “This Time Is Different” Bloomberg May 30, 2021

“From today, halt all investment in new fossil fuel supply projects and make no further final investment decisions for new unabated coal plants.” – IEA Roadmap to Net Zero by 2050

Whether you think global warming is a hoax and no technology has done more to uplift billions of people out of abject poverty than the harnessing of fossil fuels, or you think the burning of fossil fuels is irreversibly destroying the planet and urgent action to halt their use should be the top priority of humankind, or even if you think both of these things, this article is for you.

I can assure all sides the following: unless something substantial changes – and soon – the price of oil is going way higher. Is $300 oil probable? Perhaps not, but it makes for excellent clickbait. Is $300 oil impossible? Absolutely not.

Consider some history.

In the third week of February, 2021, a massive cold snap impacted much of the Lower 48 states. The power grid in Texas nearly collapsed. Just as demand for heating and power was reaching its most desperate apex, the supply of natural gas collapsed. The infrastructure simply couldn’t handle the depths of the freeze. The result? Prices of natural gas at several large trading hubs across the US skyrocketed to unthinkable levels. This chart from the US Energy Information Administration captures it well:

So how can we compare these prices to the price of oil? One of the problems with comparing quoted prices for different sources of energy is they are priced in different units, which is mostly an accident of history. For example, natural gas is priced in dollars per million British thermal units (BTUs), whereas oil is priced in dollars per barrel (a barrel being 42 gallons), and gasoline is priced in dollars per gallon (a gallon being a gallon). Habits are hard to break.

To create an apples-to-apples comparison of what these prices mean, a useful trick is to first levelize everything to millions of BTUs, which is how natural gas is sold anyway, and it just happens to be a direct measure of the inherent energy content embedded in a fuel. A standard barrel of oil contains 5.8 million BTUs. If you take the current price of oil (in dollars per barrel) and divide it by the current price of natural gas (in million BTUs), you’ll almost always get a number higher than 5.8, which makes sense because oil is generally more useful than natural gas and natural gas is often a byproduct of oil production. But on an energy-content-equivalency basis, 5.8 is the number. To put natural gas prices into an energy-contained-in-oil-equivalency basis, we simply do the reverse and multiply the price of natural gas, expressed in millions of BTUs, by 5.8.

We are now ready to put the prices for natural gas in the chart above into shocking context. On an energy-contained-in-oil-equivalency basis, natural gas prices reached the following levels in February:

SoCal Citygate: $835 per barrel

Chicago Citygate: $752 per barrel

Houston Ship Channel: $2,320 per barrel

Waha: $1,196 per barrel

OGT: $6,919 per barrel

Henry Hub: $137 per barrel

Agua Dulce: $528 per barrel

Do I have your attention?

Sure, the price of natural gas didn’t stay there, but it went there. I use this extreme example to illustrate an important point. Fossil fuels are hugely inelastic commodities. Shortages send prices soaring because they are needed and there are not yet fungible substitutes. Society might hate fossil fuels, it might even hate them for very good reasons, but society is trapped in its need for fossil fuels, at least for the time being.

We can’t escape fossil fuels without significantly higher prices. Higher prices will level the playing field for alternative technologies by making them more competitive. Higher prices will spur significant investment in new energy R&D. Higher prices will also be the only way to motivate society to cut fossil fuel use. Said another way, fossil fuels are so useful for humankind that they will never be substituted unless prices skyrocket. Higher prices it shall be. The only way out is through.

There are at least four forces aligning as huge tail winds for fossil fuel prices. First, and most important, the ESG/progressive crowd has utterly and totally won the narrative war and they will press the consequence of their undeniable victory to the maximum by attacking supply at every opportunity. Second, the fossil fuel industry is coming off a period of extended underinvestment in capital projects already, which was exacerbated by the fallout from the COVID-19 crisis. Third, massive monetary and fiscal stimulus is stoking demand for commodities globally, and fossil fuels will not be exempt (on the contrary, since fossil fuels are critical to the production of other commodities, they will feel an amplified effect of this phenomenon). Finally, and related to the third force, fiat currencies are being debased at an unprecedented rate.

In this post, I’ll only focus on the first. Larry Fink, chairman and CEO of Blackrock, is not a trained scientist. He has no particular expertise in environmental issues. He holds a BA in political science and an MBA in real estate, both from UCLA. There’s nothing wrong with these degrees, and he has parlayed them into astonishing business success. But Larry is now in charge of global oil policy. There shall be less drilling, less exploring, less permitting, and less capital spending, period. Larry has decided to make it so, and it shall be.

You can celebrate this (yay!) or bemoan this (boo!), but the one thing you can’t do is deny it. Don’t believe me? Ask the CEO of Exxon Mobil. Memo to Darren Woods: You now work for Larry, and Larry is calling the shots – his shots. Larry wouldn’t really mind $10 gasoline. It’s not like he has driven himself in decades, nor is he up for reelection, at least I don’t think he is. I certainly don’t remember voting for him. Oh – and don’t feel too bad for Darren, he is about to go from stupid rich to crazy stupid rich. Not quite Larry crazy stupid rich, but close enough for you and me.

Now for the fun part. How high can oil go?

Clearly, this chicken strongly believes all the pieces are in place for oil to make new all-time high. But what does this mean? In July 2008, the price of oil peaked at $145 a barrel, but that’s in nominal terms. A dollar today, 13 years later, does not have the same purchasing power as a dollar then. If we use the official Consumer Price Index (CPI) inflation rate of approximately 2%, the actual all-time high for oil in today’s dollars is closer to $190 a barrel. What if, as most sound-minded people believe, the government has been systematically underestimating inflation in the official numbers for decades? If you believe the real inflation rate has been 4% since 2008, the new peak oil price becomes $240 a barrel. At 6%, it becomes $310 a barrel.

Have we experienced 6% inflation per year since 2008? According to shadowstats.com, if you merely calculate CPI the way the government used to in 1990, you get an average inflation rate over this period near that number. If you calculate CPI the way the government used to in 1980, it approaches 10%. It should be noted that when the US government changes its inflation calculation methodologies, it never seems to lead to higher reported numbers. I wonder why that is?

Let’s look at it another way. Assume you believe, like I do, that gold is the only real money. How much gold buys you a barrel of oil? Today, it is a shockingly low amount – only 0.036 ounces. Yes, you read that correctly. Roughly 1 gram of gold does the trick. When oil was trading at $145 in mid-2008, its price in gold was 0.15 ounces. With gold now trading at $1,900 an ounce, that works out to about $285 a barrel oil.

Does $300 seem like clickbait now?

Look, I know what you are thinking. “On the one hand, this chicken is making a lot of sense. On the other hand, I’m reading a blog written by a chicken on Substack. How seriously can I take this stuff?”

I’ll leave you with this. If Bloomberg is flippantly dropping criminalization quotes in above-the-fold news articles detailing a sea change in how people with the real power in our society are viewing the fossil fuel industry, it’s best you sit up, pay attention, and prepare accordingly.

Tyler Durden

Fri, 06/04/2021 – 13:15

Read More

{kind=link}

{kind=link}