A recession is coming! A recession is coming! This rallying cry is quickly turning into the baseline scenario for many financial institutions on Wall Street. After the incredible May consumer price index (CPI) report defied market expectations, investors are now panicking that the Federal Reserve will turn extra hawkish to fight inflation while triggering consecutive quarterly contractions. Unfortunately, corporate leaders are not exactly ebullient over US growth prospects either.

A new CNBC-CFO Council poll revealed that 77% of chief financial officers think the US will experience a recession during the first half of 2023 because of persistent inflation. But these executives believe the recession will be over in the second half of next year, suggesting that the economy will quickly recover. Most survey participants expect the Dow Jones Industrial Average to fall below 30,000. This would represent a 9% drop from its current level of around 31,400.

CFO respondents are ostensibly not preparing for an economic downturn despite the sour opinion on the economy. Thirty-six percent revealed they would increase their spending over the next year, while 44% plan to increase personnel over the next 12 months.

That said, the numbers are comparable to a recent Conference Board Measure of CEO Confidence report. It highlighted that CEOs expect the US economy will slip into a brief and mild recession, caused primarily by trying to tame rampant price inflation. Plus, it is not only business leaders who are penciling in a recession. A recent CNBC + Acorns Invest in You survey found that 81% of adults anticipate a recession this year. This opinion is shared across party lines and income demographics.

According to a new Liberty Nation poll, 90% of survey participants think the US is headed for a recession.

But some purport that it’s already here, including the Bank of America. “We’re in technical recession, but just don’t realize it,” said Michael Hartnett, the chief investment strategist at the BofA. “What can turn shallow into deep is the great unknown of the shadow banking system.”

Consumers Give Up

As Liberty Nation has repeatedly reported in recent months, consumers have been gradually losing their patience with President Joe Biden’s economy. The latest University of Michigan data suggest that consumers have given up on this economy and will now wallow in self-pity and torture themselves by binge-watching January 6 hearings.

Joe Biden (Photo by Kevin Dietsch/Getty Images)

The June Consumer Sentiment Index crashed to an all-time low of 50.2, down from 58.4 in May. This is also higher than the market estimate of 58. The Consumer Expectations Index plunged to 46.8, down from 55.2. The Current Conditions Index also declined to 55.4, down from 63.3. US consumers raised their inflation outlook, too, as one- and five-year expectations rose to 5.4% and 3.3%, respectively.

From business conditions to personal financial situations, the index placed a spotlight on a weakening economy. “Consumer sentiment declined by 14% from May, continuing a downward trend over the last year and reaching its lowest recorded value, comparable to the trough reached in the middle of the 1980 recession,” said Joanne Hsu, the Surveys of Consumers Director, in a statement.

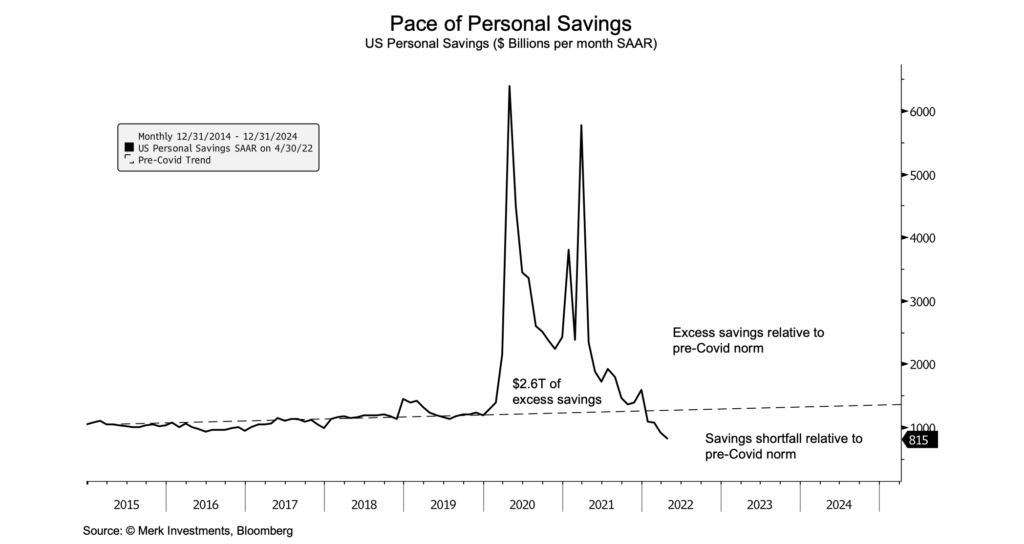

Indeed, households are in a tough position in these inflationary conditions. The personal savings rate has collapsed, credit growth has spiked, and inflation has eaten away at workers’ wage gains. According to new data from Merk Investments, that $2.6 trillion in accumulated savings in 2020 and 2021 could soon be wiped out. Moreover, with more aggressive quantitative tightening by the Federal Reserve, consumers will be spending billions of dollars more to service their debts and keep their heads above water.

Russian All The Way To The Bank

The Russian economy is weathering the economic storm clouds. All the key data points suggest that Moscow is defying the odds and both surviving and thriving, despite the international community imposing economic sanctions. Foreign exchange reserves remain strong, the purchasing managers’ index (PMI) readings are improving, inflation has calmed down, the energy industry is robust, and the labor market is holding steady.

The latest trends prompted the central bank to slash its benchmark interest rate by 150 basis points to a pre-war level of 9.5%. The market had called for a 100-basis-point reduction. This comes two weeks after the institution deployed a cut of 300 basis points, and Governor Elvira Nabiullina warned that additional loosening could be coming.

The latest trends prompted the central bank to slash its benchmark interest rate by 150 basis points to a pre-war level of 9.5%. The market had called for a 100-basis-point reduction. This comes two weeks after the institution deployed a cut of 300 basis points, and Governor Elvira Nabiullina warned that additional loosening could be coming.

“Inflation is slowing down, including under the influence of the ruble strengthening and lower inflation expectations. That gave us the opportunity to reduce the key rate again today,” Nabiullina told reporters at a news conference.

Not only is the Russian economy enduring, but the ruble is also rallying. In fact, the ruble is the top-performing currency in forex markets this year. After the central bank made the announcement, the ruble advanced nearly 0.9% to 58.2500. Year-to-date, the ruble has gained more than 22% against the US dollar, even after collapsing in the immediate aftermath of the Ukraine-Russia military conflict.

Who knew that Nabiullina would do a better job than Jerome Powell and the plethora of other Western central bankers?

Andrew Moran – Economics Correspondent at LibertyNation.com. Andrew has written extensively on economics, business, and political subjects for the last decade. He also writes about economics at The Epoch Times and financial markets at FX Daily Report. He is the author of “The War on Cash.” You can learn more at AndrewMoran.net.