The V-Shaped Recovery Never Happened

Authored by Ryan McMaken via The Mises Institute,

In a display of unconvincing enthusiasm, NBC reported Friday that payroll employment “surged” in February. Specifically, total nonfarm payrolls (seasonally adjusted) grew 379,000, month-over-month which was above the expected increase of 210,000.

That might sound great to some, but a closer look suggests jobs growth is quite a bit more sedate than the media narrative suggests. Moreover, a look at the job growth situation in recent months is a helpful reminder that the “V-shaped recovery” we were promised last spring never happened.

Some may remember all that talk about a V-shaped recovery last year. That was back when we were being assured that “two weeks” —or maybe two months— to “slow the spread” of covid-19 would pay countless dividends, because then lockdowns and forced business closures would somehow miraculously “beat back” the disease and then employment and the economy would come roaring back, the Fed could end its stimulus programs, and everything would be fine.

Back in June, CNBC announced “The recovery from the coronavirus sure looks V-shaped” and pointed to record job growth coming out of the initial collapse in employment that occurred in March and April.

But then the good news basically stopped, at least as far as employment was concerned.

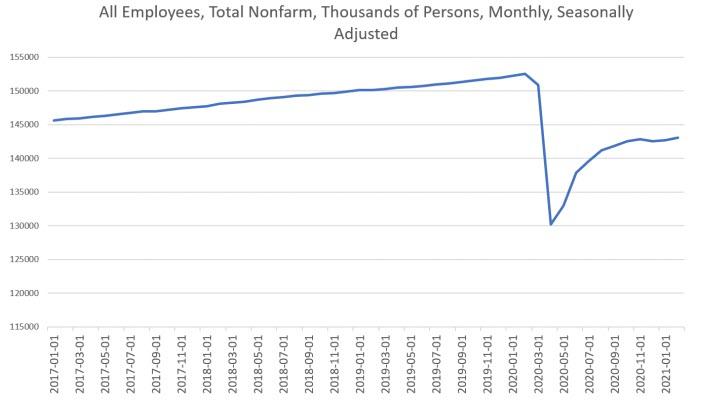

For example, while February’s month-over-month job growth might look impressive, the US remains a long, long way from where total employment was this time last year. In February of last year, before the effects of lockdowns were beginning to be felt, total employment topped 152 million in the US. After this February’s “surge” in employment, total employment was at 143 million, or still down 9 million. In other words, total employment is still where it was back in 2015.

Yes, the US has regained 13 million jobs since the bottom of the crisis back in April 2020. But as we can see in the first graph, total employment has gone sideways since last November, and is only up by 200,000 over the past four months. That’s not exactly a “surge” of anything. And it’s definitely not anything resembling a “v-shaped” recovery. It looks more like a very week version of a “check mark-shaped recovery” that some predicted last year. Except the tail end of this check mark has so far been nearly flat.

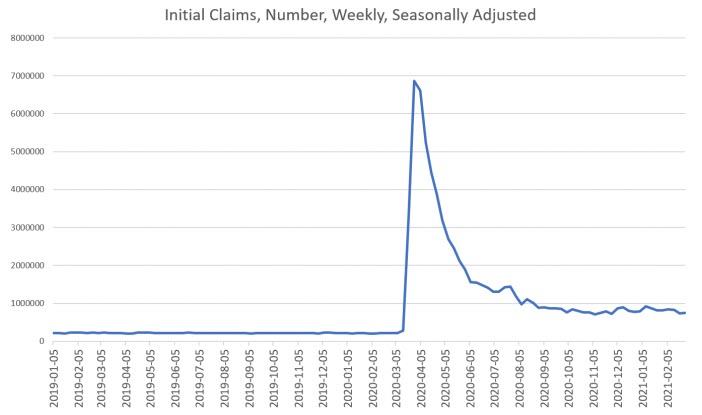

And then there is the unemployment insurance totals. New unemployment insurance claims have hovered around between 700,000 and 800,000, every week, for the past five months. There’s no evidence of any downward trend here, and the V-shaped recover turned into a long slog past the initial anemic “recovery” that took place last summer.

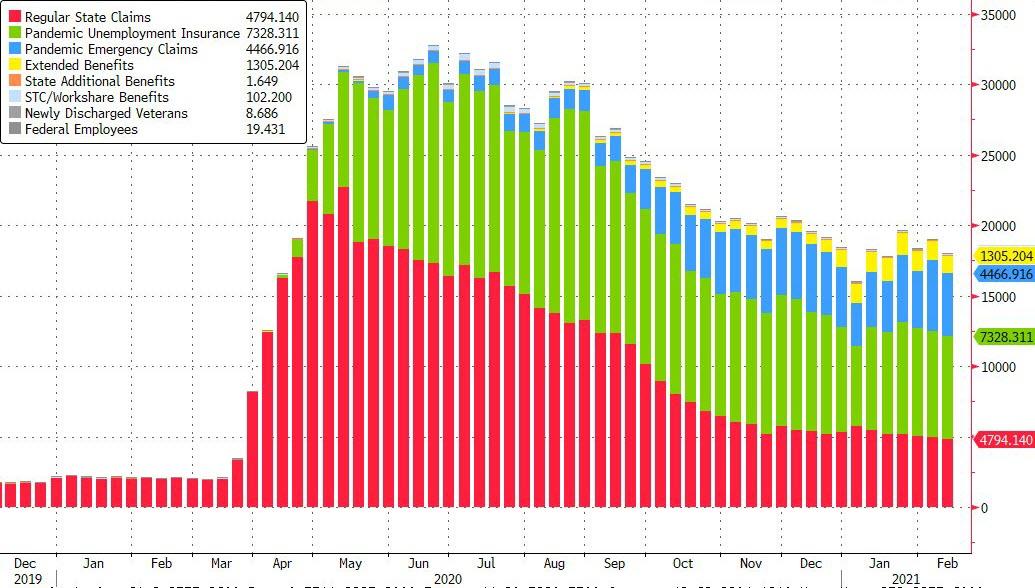

Continuing unemployment claims are slowly lessening, however. Since the beginning of the calendar year, continuing claims have fallen from 5.1 million to 4.2 million.

In both cases, totals remain well within recessionary territory. Back during the Great Recession, for example, continuing claims peaked at 6.6 million. Claims totaled about 1.7 million in 2020 before the recession began.

Unemployment has also remained stubbornly high among those making claims under the Pandemic Unemployment Assistance program. In early January, total continuing claims under the PUA was at 8.3 million, continuing a long slow trend downward. By early March, continuing claims had only fallen to 7.3 million.

That’s progress, but combined with regular unemployment insurance, it means there are still more than ten million Americans receiving some form of unemployment insurance, which hardly suggests a robust recovery.

The unemployment rate remains troublingly high as well. The headline unemployment rate for February was reported as falling to 6.2 percent. That’s certainly an improvement from April 2020’s peak rate of 14.8 percent.

But as is so often the case, the headline rate masks a more complex reality surrounding the unemployment rate.

Although the official rate is 6.2 percent, the Washington Post’s Heather Long notes that the Minnesota Fed’s Neel Kashkari admitted “the true unemployment rate is around 9.5%”

Why the gap? It is a result of several factors, including falling response rates to the Labor Department’s employment surveys, the fact many have simply stopped looking for work, and ambiguities in the data over whether or not someone is only temporarily unemployed.

In other words, the official unemployment calculation excludes a great many people who would like to have jobs, but who gave up and stopped looking for work. Many others are only technically “temporarily” unemployed but in practice are jobless. The official data says many of these people are “on leave.”

Fed Chairman Jerome Powell has also admitted that the unemployment rate was likely close to 10 percent in January. Not surprisingly, Kashkari predict no “liftoff” for the economy until 2022.

Taking all this together, it’s pretty clear the United States is still very much in the midst of a jobs recession.

Yet, CNBC tells us that the economy is “on fire” because GDP totals may surge in the upcoming first quarter data. “Economic growth in the first quarter could hit 10%,” CNBC triumphantly proclaims, claiming the economy has “roared back” and is set to defy even the rosiest expectation.

But unless something changes big time in the jobs situation, we’ll have to start looking at GDP the way we look at stock prices: something that reflects a lot of optimism and growth in some sectors of the economy but which has very little to do with the personal finances and job prospects of millions of ordinary Americans.

Tyler Durden

Tue, 03/09/2021 – 20:45

The V-Shaped Recovery Never Happened

Authored by Ryan McMaken via The Mises Institute,

In a display of unconvincing enthusiasm, NBC reported Friday that payroll employment “surged” in February. Specifically, total nonfarm payrolls (seasonally adjusted) grew 379,000, month-over-month which was above the expected increase of 210,000.

That might sound great to some, but a closer look suggests jobs growth is quite a bit more sedate than the media narrative suggests. Moreover, a look at the job growth situation in recent months is a helpful reminder that the “V-shaped recovery” we were promised last spring never happened.

Some may remember all that talk about a V-shaped recovery last year. That was back when we were being assured that “two weeks” —or maybe two months— to “slow the spread” of covid-19 would pay countless dividends, because then lockdowns and forced business closures would somehow miraculously “beat back” the disease and then employment and the economy would come roaring back, the Fed could end its stimulus programs, and everything would be fine.

Back in June, CNBC announced “The recovery from the coronavirus sure looks V-shaped” and pointed to record job growth coming out of the initial collapse in employment that occurred in March and April.

But then the good news basically stopped, at least as far as employment was concerned.

For example, while February’s month-over-month job growth might look impressive, the US remains a long, long way from where total employment was this time last year. In February of last year, before the effects of lockdowns were beginning to be felt, total employment topped 152 million in the US. After this February’s “surge” in employment, total employment was at 143 million, or still down 9 million. In other words, total employment is still where it was back in 2015.

Yes, the US has regained 13 million jobs since the bottom of the crisis back in April 2020. But as we can see in the first graph, total employment has gone sideways since last November, and is only up by 200,000 over the past four months. That’s not exactly a “surge” of anything. And it’s definitely not anything resembling a “v-shaped” recovery. It looks more like a very week version of a “check mark-shaped recovery” that some predicted last year. Except the tail end of this check mark has so far been nearly flat.

And then there is the unemployment insurance totals. New unemployment insurance claims have hovered around between 700,000 and 800,000, every week, for the past five months. There’s no evidence of any downward trend here, and the V-shaped recover turned into a long slog past the initial anemic “recovery” that took place last summer.

Continuing unemployment claims are slowly lessening, however. Since the beginning of the calendar year, continuing claims have fallen from 5.1 million to 4.2 million.

In both cases, totals remain well within recessionary territory. Back during the Great Recession, for example, continuing claims peaked at 6.6 million. Claims totaled about 1.7 million in 2020 before the recession began.

Unemployment has also remained stubbornly high among those making claims under the Pandemic Unemployment Assistance program. In early January, total continuing claims under the PUA was at 8.3 million, continuing a long slow trend downward. By early March, continuing claims had only fallen to 7.3 million.

That’s progress, but combined with regular unemployment insurance, it means there are still more than ten million Americans receiving some form of unemployment insurance, which hardly suggests a robust recovery.

The unemployment rate remains troublingly high as well. The headline unemployment rate for February was reported as falling to 6.2 percent. That’s certainly an improvement from April 2020’s peak rate of 14.8 percent.

But as is so often the case, the headline rate masks a more complex reality surrounding the unemployment rate.

Although the official rate is 6.2 percent, the Washington Post’s Heather Long notes that the Minnesota Fed’s Neel Kashkari admitted “the true unemployment rate is around 9.5%”

Why the gap? It is a result of several factors, including falling response rates to the Labor Department’s employment surveys, the fact many have simply stopped looking for work, and ambiguities in the data over whether or not someone is only temporarily unemployed.

In other words, the official unemployment calculation excludes a great many people who would like to have jobs, but who gave up and stopped looking for work. Many others are only technically “temporarily” unemployed but in practice are jobless. The official data says many of these people are “on leave.”

Fed Chairman Jerome Powell has also admitted that the unemployment rate was likely close to 10 percent in January. Not surprisingly, Kashkari predict no “liftoff” for the economy until 2022.

Taking all this together, it’s pretty clear the United States is still very much in the midst of a jobs recession.

Yet, CNBC tells us that the economy is “on fire” because GDP totals may surge in the upcoming first quarter data. “Economic growth in the first quarter could hit 10%,” CNBC triumphantly proclaims, claiming the economy has “roared back” and is set to defy even the rosiest expectation.

But unless something changes big time in the jobs situation, we’ll have to start looking at GDP the way we look at stock prices: something that reflects a lot of optimism and growth in some sectors of the economy but which has very little to do with the personal finances and job prospects of millions of ordinary Americans.

Tyler Durden

Tue, 03/09/2021 – 20:45

Read More