A common belief is that if the world does not have adequate energy, the result will be high prices. These high prices will allow more fossil fuels to be extracted or will allow renewables to substitute for fossil fuels.

In my view, the real issue is quite different: Inadequate energy supply of the types the economy requires can be expected to affect the economy in a way that causes it to become “unglued.” The economy will gradually fall apart as infighting becomes more of a problem. Goods won’t necessarily be high-priced; many simply won’t be available at any price. Political parties will fragment. Conflict within countries, such as the recent Wagner conflict with the military leadership in Russia, will become more common.

It has become fashionable to use models to predict the future, but simple models do not consider real-world dynamics. They don’t consider the importance of already existing infrastructure and the types of energy products this infrastructure requires. They don’t consider the importance of continuing food production. They don’t consider the dynamics of “not enough goods and services to go around.”

In this post, I will look at some pieces of evidence that suggest we should expect the world economy to become unglued as limits are hit. A corollary is that we cannot expect a transition to a world powered by renewables to work.

[1] It is easy to show that the energy supplies of a finite world will eventually fall short.

Anyone can model the energy supplies of a finite world as a bucket of sand and a scooper. If the scooper is used to remove the sand from the bucket, it will eventually become empty. If we start with a larger bucket of sand, perhaps the process can be delayed. Or, if we use a smaller scooper, the process will be delayed. But the result will be the same.

Back in 1957, Rear Admiral Hyman Rickover of the US Navy gave a speech in which he said,

For it is an unpleasant fact that according to our best estimates, total fossil fuel reserves recoverable at not over twice today’s unit cost, are likely to run out at some time between the years 2000 and 2050, if present standards of living and population growth rates are taken into account.

In this speech, Rickover pointed out the importance of fossil fuels to maintain our standard of living and to win wars. It was clear to the military that fossil fuel energy supplies were tremendously important in preventing future problems for the economy.

[2] History shows that economies tend to grow and eventually collapse.

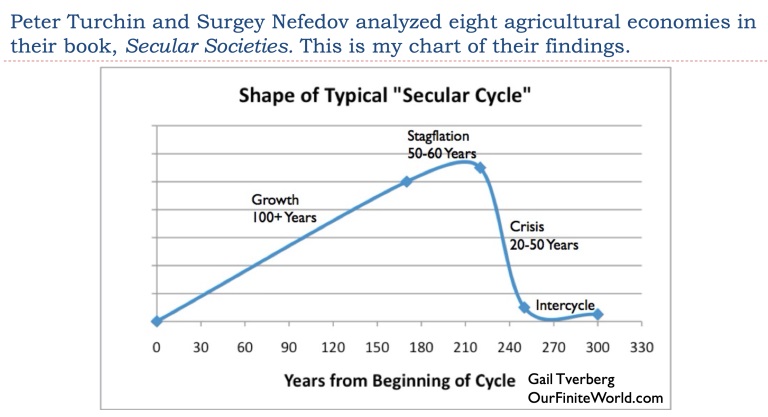

Economies tend to operate in cycles, as illustrated in Figure 1.

Figure 1. My chart of the findings of Peter Turchin and Surgey Nefedov in their 2009 book, Secular Cycles.

The eight economies analyzed by Turchin and Nefedov moved into a new area or acquired a new energy resource. These economies tended to grow for a long periods, well over 100 years, until the populations hit the carrying capacity of the available resources. These economies were able to work around these resource limits during a period of Stagflation, which typically lasted about 50 to 60 years. Eventually, the problems became too great to be overcome. A Crisis Period of falling population and GDP, lasting 20 to 50 years, typically ensued.

[3] The world economy today seems to be following a similar cycle based on its use of fossil fuels. In fact, we seem to be in the Crisis Period of such a cycle.

Today’s fossil fuel-based world economy started growing at varying times, in various places around the world, becoming well established by the early 1800s. It seems to have hit a Stagflation Period between 1970 and 1980. Recent patterns in oil supply per capita, interest rates, and debt levels suggest to me that the world economy has entered the Crisis Period of the current cycle.

To me, oil supply, particularly crude oil supply, is exceptionally important in keeping the economy growing because it is heavily used in the producing the food supply and transporting it to market. In fact, it is heavily used in transportation of all kinds. We can see what is going wrong by looking at the trend in crude oil per capita (blue line on Figure 2).

Figure 2. World oil supply per capita based on data of the US Energy Information Administration.

On Figure 2, a line is drawn at 2005, when many people believe that peak “conventional” oil was reached. The line at 2009 points out the long-term slide in oil consumption per capita between 2005 and 2009, related at least in part to the Great Recession of 2008-2009. There was another steep drop in crude oil per capita in 2020, and this drop has not been made up. Cutbacks in drilling and low oil prices suggest that per capita consumption may never recover to the 2018 level.

US interest rates over time indicate a clear up and down pattern, with increases to 1981, and mostly decreases since then (Figure 3). Raising interest rates is like putting brakes on the economy because it makes monthly payments on loans higher. Lowering interest rates is like pressing on the accelerator.

Figure 3. Interest rates of 3-month Treasury Bills, 10-year Treasury Securities, and 30-year Fixed Rate Mortgages, based on information of the Federal Reserve of Saint Louis.

The US was in a Stagflation Period after 1980. Lower interest rates helped push the economy along, at least until they could go no lower. The first place falling interest rates stalled was in 2008, when they hit zero for the shortest-term debt. About the beginning of 2021, interest rates started to rise, to try to stop inflation.

At the same time, the US’s ability to add to debt, except US government debt, seems to have stalled about 2008 and again in 2021.

Figure 4. US ratios of debt to GDP by sector based on data from the Federal Reserve of St. Louis database. Amounts for total debt and for Households (which includes not-for-profits, such as churches), Business Non-Financial, and Federal Government are from this database. Financial+ is calculated by subtraction.

The combination of Figures 2, 3, and 4 suggests that the world economy has been on shaky ground since 2008. The US economy has been operating with incredibly low interest rates. If the world loses the ability to hide energy problems behind ever-lower interest and ever-higher debt, (particularly government debt), many parts of the economy could start coming apart.

[4] The world’s total energy supply must increase at least as fast as population to keep the economy growing and away from collapse.

A couple of years ago, I did an analysis of the growth in energy consumption compared to the growth of population over the period 1820 to 2020. I found that when energy consumption was rising faster than population, there tended to be a rise in standards of living. When energy consumption grew only as fast as population, problematic things (such as wars and governmental collapses) tended to happen (Figure 5).

Figure 5. Chart by Gail Tverberg using data from several sources, in energy data from Vaclav Smil’s estimates from Energy Transitions: History, Requirements and Prospects, together with BP Statistical Data for 1965 and subsequent.

On Figure 5, the sum of red and blue areas represents world energy consumption growth by 10-year periods. The blue areas represent population growth percentages during these 10-year periods. The red area is determined by subtraction. It represents the amount of energy consumption growth that is “left over” for growth in standards of living. When growth in energy consumption was inadequate, wars tended to take place, and the collapse of the central government of the Soviet Union took place.

We are now at a point where energy consumption may decrease dramatically in future years, especially if we attempt to convert to a system based on intermittent wind and solar. The drop in energy consumption, relative to population, would likely be far worse than any situation we have experienced in the past. Besides being inadequate in quantity, wind and solar are not adapted to handling our most basic need, which is for providing the inputs farmers require to provide us with food.

[5] A key to understanding the role of fuels of the right kinds is understanding the physics-based way that the economy operates.

The economy is very much like the human body. The operation of both is governed by the laws of physics. The human body needs to consume a variety of food products. Alternative foods can be substituted, but the overall quantity of food needs to be sufficient for the population and their level of activity.

Likewise, the world economy requires a variety of energy products to operate. Substitutions can sometimes be made, but the overall quantity must be sufficient to support the activities of the economy, including providing adequate food and water for the population and ways to transport these items to the population that needs them.

There are other similarities, as well. Humans start out as small babies. Eventually, humans grow old. In the years leading up to death, they often become frail. The cycle downward at the end of an economy’s life is somewhat similar. Economies, even the world economy, cannot last forever.

[6] To build and maintain cities, it is necessary for energy to be easily storable.

In his book, Against the Grain, the American political scientist James C. Scott points out that in order for governments to grow and to provide infrastructure for cities, it is necessary to tax farmers. Grain is ideal for this; taxing a root crop such as sweet potatoes does not work well. Root crops are hard to see when they are growing. They also are harder to transport and store.

Clearly, farmers must have a surplus of storable energy to make cities and good roads work. They must be able to produce this surplus energy in a sufficiently profitable way that governments can tax it and use the proceeds for the benefit of the overall population.

I think that excess storable energy is the true “net energy” that some authors write about. A city cannot operate only when the wind happens to be blowing or the sun happens to be shining. Everyone would clog the roads at the same time, trying to get to a job that might last only a few minutes. Even today, if a city is to have electricity when it is needed, even in winter, there needs to be a storable supply of fuel to provide this electricity. Batteries cannot provide this level of storage; we would run out of materials.

Cities are essential for the sharing of ideas and for the operation of major industries.

We can have an economy of hunter-gatherers running on intermittent energy alone. We might even be able to have cities based on stored grain, as civilizations did in the past. But the population would need to be far less than today’s 8 billion.

[7] Both energy density and storability are needed if the world’s population is to be fed.

A farmer needs machines that are not so heavy that they will sink into the soil. Soil compaction is also an issue with heavy machines. If soil is compacted, water cannot make its way through the pores properly. Rain will tend to run off, causing erosion, instead of sinking in, to provide longer-term benefit. Soil compaction is already a problem with today’s large machinery. Less dense fuels, or the use of heavy battery packs, will make the problem even worse.

Energy dense fuel is also needed for the transportation of food. In fact, energy dense fuel, such as diesel or jet fuel, is used in nearly all of today’s very large vehicles. Heavy vehicles operated in situations that require very large bursts of power especially need energy dense fuel. Examples include semi-trailer trucks, buses that drive up steep hills, airplanes that need bursts of power to take off, agricultural vehicles that might get stuck in mud, and vehicles used in construction and road making.

Trains operating on smooth tracks, with limited gradients, don’t need the same bursts of power, so they are sometimes electric. Boats don’t generally need large bursts of power, but boats generally use an energy-dense liquid fuel to propel them on long journeys. Storing enough electricity in batteries to power such long journeys would be impractical.

The recently published 2023 Statistical Review of World Energy (now produced by the Energy Institute, instead of BP) shows that the heavier, more energy-dense types of burnable oil have been falling as a share of the world’s oil supply.

Figure 6. Chart shows that more energy dense types of oil products (sum of diesel, jet fuel/kerosene, and fuel oil) have been falling relative to the world supply of diesel or total liquids oil. All amounts used in the calculation are from EI’s 2023 Statistical Review of World Energy, except for world crude oil for 1980 through 1999, which is based on EIA data.

These heavier grades are the ones best suited to essential future energy needs, and they seem to be depleting the most quickly.

[8] Added complexity is deceptive. It looks like it can save energy, but it tends to increase wage disparities and makes the overall system more fragile.

Added complexity for an economy includes changes such as more built infrastructure (roads, dams, bridges), larger businesses, more specialization of workers, more international trade, and longer supply chains. It is easy for modelers to assume that these changes have no energy cost, but in reality, they do.

Changes enabling growing complexity go hand in hand with more debt and more financialization of the economy. With greater complexity, owners and managers of businesses, as well as highly trained workers, tend to receive a disproportionate share of the wealth. This means that little is left over for non-elite workers. These wage and wealth disparities lead to the unhappiness of the lower-paid workers. This is especially the case during economic downturns.

With added complexity, the system becomes more fragile. Supply lines become longer, so missing parts are more likely to be a problem. Repair parts for wind turbines may become unavailable, for example. The US grid would need massive improvements to handle the proposed increase in wind and solar power, and the demands of EVs. All of the simultaneous commodity demands may become too much for suppliers to meet.

Even changes in financial systems could be a serious problem. With the conflict over the SWIFT money processing system, will one group of countries start using a different financial exchange program, such as Iran’s financial messaging system SEPAM? Will Western nations find themselves cut off from purchasing inputs they depend upon?

[9] Modeling underlying the analysis for the 1972 book The Limits to Growth shows that (total materials required for reinvestment each year) as a percentage of (total economic output) is an important limit.

Somehow, the economy must provide enough goods and services both for the needs of the current members of the economy and for the investment needed to keep the system operating in the future.

The economy is squeezed in three different ways:

The population keeps growing, and each person needs food, clothing, and a variety of services.

Resources of all kinds (not just fossil fuels) become more difficult to extract due to depletion. More of the output of the economy needs to go into investment, just to get the same quantity of copper, lithium, nickel, and minerals of all kinds, including fossil fuels.

With the rising population and increasing resource use, pollution becomes a bigger problem. Mitigation efforts lead to a need to use more resources to keep pollution away from humans.

To keep the system operating, we cannot spend very much on the combination of resource extraction and pollution control, or there will not be enough resources left to meet the needs of the growing population.

This combination limit tells me is that a rapid transition of any kind toward any new energy type, even toward the use of “green energy,” is not likely to work well. There is a reason why past transitions to new energy types have been very slow. The economy cannot invest enough without starving other parts of the economy.

Some people have interpreted this combination limit as an Energy Return on Energy Investment limit of perhaps 10:1, but it seems to me to be a far more serious limit than this. At a minimum, all types of resources, including those for backup batteries and additional long distance transmission lines, must be included in any calculation for renewables.

Also, to keep the system operating, any shift from fossil fuels to renewables cannot have a delayed payback period, relative to fossil fuels, or the huge up-front investment will become a problem. The up-front investment in renewables will be higher, but there will not be enough output to support the economy. The “real” economy does not operate on an accrual basis; people need to eat every day, and aluminum smelters expect to operate every day.

As I mentioned previously, renewables aren’t really helpful for growing food. Nor are reliable enough to power aluminum smelters, so there is a real issue as to whether they should even be considered as possible substitutes for fossil fuels. They are simply add-ons to the fossil fuel system to avoid having to talk about our fossil fuel supply problems. Reframing the issue as “wanting to move away from fossil fuels to prevent climate change” saves having to talk about the inadequate fossil fuel supply problem, and the fact that fossil fuels are what make today’s lifestyle possible.

[10] Energy prices must be both high enough for producers to make a profit and low enough for consumers to afford goods made with these energy products.

It is the conflict between the needs of consumers and producers that tends to bring fossil fuel energy production down. Consumers say, “We can’t stand oil (or natural gas or electricity) prices this high, and demand that politicians hold prices down.” In fact, this just recently happened in Australia with natural gas prices. Without an adequate profit motive, drillers cut back on drilling and production falls.

Renewables have gotten mandates and subsidies, especially the subsidy of going first on the electric grid. It is these subsidies and mandates that have made investments in wind turbines and solar panels attractive. Once governments have more financial problems and these subsidies disappear, owners are likely to stop making repairs to these systems. They will not last longer than fossil fuel-based systems, in my opinion.

[11] Conclusion: We are in uncharted territory.

I mentioned that the Great Recession of 2008-2009 seemed to mark the beginning of the downturn. More financial problems are no doubt ahead, but other kinds of strange events may also occur.

It seems possible that Covid, its vaccines, and the restrictions in 2020 may even have been part of the “ungluing.” Self-organizing physics-based systems act strangely. World oil supply started declining in 2019. Militaries around the world have been concerned about fossil fuel limits for many years. Militaries have also been deeply involved with germ warfare. Economies around the world were experiencing financial problems. The shutdowns conveniently reduced demand and prices for oil, while giving economies around the world an excuse for more debt. The problems were kicked down the road until 2022 and 2023, when they reappeared as inflation.

We can’t know what lies ahead, but it may be very strange, indeed.