They’re “Damn Near Criminally Incompetent” – David Stockman Crushes “Camarilla Of Money-Pumpers”

Authored by David Stockman via Contra Corner blog,

A Fed Lifer’s Five Basis Point Farce

We start with this gem from NY Fed president John Williams. He claims the Fed must keep injecting $120 billion per month of fraudulent credit into Wall Street because, apparently, this quarter’s likely 7% real GDP growth and 5% inflation are not sufficient to meet the Fed’s goals:

“… the data and conditions have not progressed enough for the Federal Open Market Committee to shift its monetary policy stance of strong support for the economic recovery.”…

You can’t say enough bad things about this knucklehead. He’s the very poster boy for the camarilla of academics and Fed lifers who have hijacked the nation’s central bank.

For want of doubt, here is William’s career since age 18:

1980-1984: A.B. in economics at University of California at Berkeley;

1985-1989: MA in economics at London School of Economics;

1990-1994: PhD in economics at Stanford University;

1995-2002: Federal Reserve Board staff economist;

2003-2010: Director of Research at the San Francisco Fed;

2011-2018: President, San Francisco Fed;

2018-2021: President, New York Fed.

Does this man remind you of a medieval theologian who never escaped the bosom of the Roman Catholic Church, and who did truly believe you can count the number of angels on the head of a pin?

Stated differently, Williams has been so mentally flayed by 40 years of captivity in macroeconomic models and the Fed’s theological groupthink that he can no longer think at all. And the evidence is overwhelming.

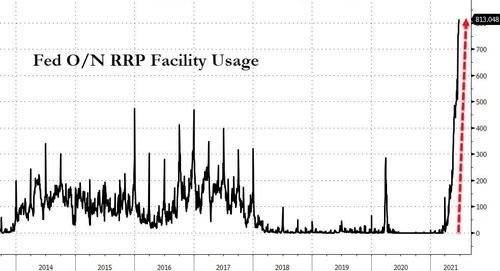

Even as the Fed is injecting $120 billion of fresh cash into the dealer markets each and every month, Wall Street has become so waterlogged with cash that upwards of $800 billion is being loaned right back to the Fed via its so-called o/n RRP facility.

That’s right. These drunken sailors have printed so much money that even Wall Street couldn’t find a place to park it with a yield above the 0.00% level that was on offer at the Fed’s RRP window.

So as head of the Fed’s trading desk on Wall Street, what did Williams propose?

Why nothing less than forcing what amounts to five more monetary angels to sit on the head of the Fed’s sacred pin.

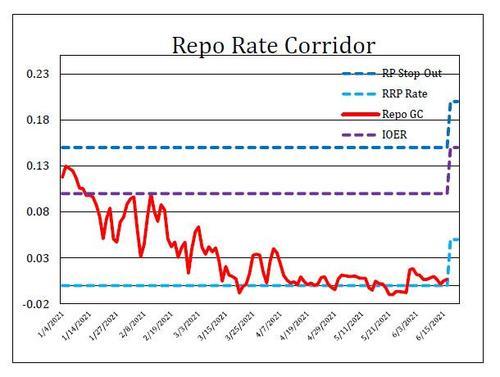

That is to say, the money market was so waterlogged with cash that the GC repo rate (red line), which is the general collateral overnight secured borrowing rate in the tri-party repo market, was being pushed under 0.00%. It was therefore threatening to drive the Fed’s sacrosanct target rate for Federal funds below its official 0-10 basis point corridor.

But when it comes to the pure marginalia of a handful of basis points in the overnight money market, the Fed commands absolute obedience. Never mind that the funds rate does not make one damn bit of difference to the borrowing costs of any household or business on main street America. And we do mean zero “difference” as in nichts, nada and nugatory.

Don’t tell Dr. John Williams, however. By his lights, the Fed must be and will be obeyed by the money markets. Period.

So at its recent meeting, the Fed under Williams guidance raised the lower and upper bounds of the control corridor by the astounding sum of, well, five basis points!

That’s right. To keep cash heavy Wall Street operators from parking funds overnight in the GC repo market below its 0.00% dictum at the bottom of the corridor, its raised its RRP offer rate to 0.05% (dashed light blue line).

By the same token, banks are now choking on $3.8 trillion of excess reserves . So to keep them from putting these reserves to work at rates below the upper corridor of its sacrosanct policy target, the Fed raised its IOER rate (interest paid on excess reserves) from a comical 10 basis points to an only slightly less ludicrous 15 basis points (dashed purple line).

This farce, which was announced in weighty techno-speak, amounted to the 6-year old bully in the sandbox expostulating a belligerent, “take that!”

What the 5 basis point RRP rate actually means, of course, is that sitting on a $8.0 trillion balance sheet of essentially risk free sovereign debt, the Fed nonetheless will now borrow unlimited amounts at 5 basis points from money market funds and others engorged with cash.

Let us repeat the word borrow: The Fed is paying money markets to bring coals to Newcastle, and for no rational purpose other than because it says so.

For crying out loud, if it really wanted to drain excess cash from the money markets, which is what the recent $800 billion of o/n RRP facility borrowing amounted to, it could just sell a small portion of its immense $8 trillion hoard of Treasury bills and notes or GSE securities.

But, no, that would amount to an admission that its is changing it “policy stance” toward tightening – a shift that the Keynesian fanatics like Williams who dominate the FOMC cannot abide.

Indeed, borrowing cash from Wall Street with one-arm while it is pumping out massive new quantities of the same with its other arm is about as absurd as it gets. And paying banks 15 basis points to keep excess reserves stashed at the New York Fed is even more so.

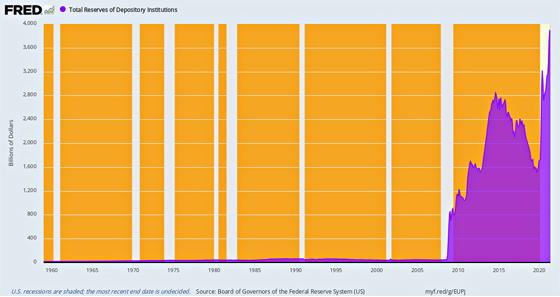

The chart below tells you all you need to know. In its misbegotten quest to keep interest rates at essentially zero on the front end of the curve, and well under 1.0% for tenors out to five years, the Fed has pumped so much cash into the banking system as to bury it in Ben Franklins.

Since the current reserve requirement on transactions balances was lowered to zero last year, the entirety of bank reserves now amount to excess reserves, which figure totaled $3.89 trillion at the end of April.

Do these people have a screw loose? The banks are literally submerged in cash, but the likes of John Williams won’t even talk about talking about tapering their $120 billion per month printathon of even more cash.

It is worth noting the thin purple area of the chart stretching from 1947 to exactly August 2008. That was the eve of the Lehman meltdown, which event caused Bernanke to jump the shark at the Fed’s printing press, nearly tripling its balance sheet in barely 13 weeks.

Before the Bernanke tsunami, however, total banking system reserves amounted to just $46 billion or a scant 0.3% of GDP. And that, in turn, represented a 50-year trend of declining bank reserves relative to GDP. The former had stood at about $30 billion and 2.5% of GDP when Nixon pulled the plug on gold-backed money in August 1971 and barely 1.2% of GDP when Greenspan cranked up the printing presses in October 1987 to bailout Wall Street from a 22% one-day meltdown.

By the end of April 2021, by contrast, bank reserves stood 17.7% of GDP, and for no valid reason of economics, finance or banking. Banks were choking on cash because the madmen in the Eccles Building mindlessly believe, as John Williams averred above, that near-zero interest rates and massive monetization of the public debt are “supporting the economic recovery”.

Total Reserves of the Banking System

No, they are not. Upwards of $6 trillion of fiscal stimulus is doing that job, and then some.

What zero interest rates are actually doing is literally destroying every market function that is necessary for sustained capitalist growth and prosperity and the natural equities of the free market, as well.

The foremost victim of the Williams/Fed variety of “support for the recovery” is the function of generating real money savings from current production and income. The Fed’s ZIRP policy means that savers unwilling to expose their hard-earned wealth to the wild west casino in the stock and bond markets, which have metastasized from the Fed’s mindless money-printing, are effectively SOL.

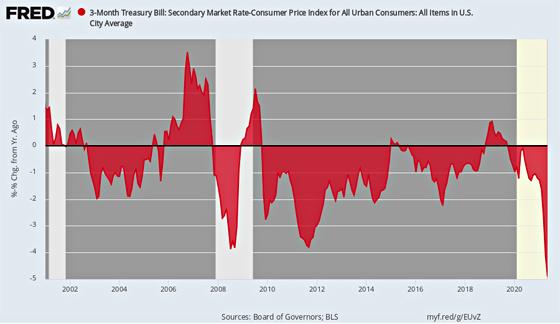

The chart below covers the 244 months since January 2001 and measures the difference between the 90-day T-bill rate as a proxy for liquid savings and the year-over-year change in the CPI. That is, the real return on savings.

As it has happened, the real savings rate has been negative during 187 of those months, or 77% of the time since 2001, when the Greenspan Fed went into money-printing hyper-drive to erase the impact of the dotcom crash.

Forget the loss of economic function that must necessarily occur when the supply of savings dries up. These Keynesian nincompoops have been anti-savings since JM Keynes himself called for the euthanasia of the bond owning rentiers back in the 1930s.

But what is even more diabolical is the Fed’s implicit edict to blue-haired widows and cautious younger people alike: Namely, put your wealth in harms’ way in the casino via the stock market or junk bonds or we will liquidate it through negative real returns on savings accounts until the cows come home.

Indeed, if the Fed could be indicted for grotesque economic and social injustice – this chart is the smoking gun. After all, never in a million years on an honest free market of sound money would savers and borrowers form the hideous bargains shown below in the vast areas below the zero line, and for 20-years running at that.

Real Return On Liquid Savings, 2001-2021

Of course, the lifetime savings of tens of millions of citizens are being gutted by an unelected monetary politburo in a manner that has never, ever been, or could be, authorized by the US Congress; and for the malign purpose of insuring the very right amount of inflation as divined by power-hungry crackpots like Powell, Williams, Clarida, Brainard and the rest of the Keynesian posse, whose contributions to the latest Fed dot plot say that the first rate-hike will not occur until 2024!

That’s sheer madness. These people are obliterating every rule of sound money and rational finance in a futile effort to deliver something that benefits no one. Namely, 2.00% inflation averaged over a secret period of time known only to the self-appointed high priests of the latter day monetary temple known as the Fed.

In fact, the crackpots in the Cleveland branch of the Fed have gone so far as to produce Lego-based animated videos explaining inflation and how the Fed has the tools to keep it on the straight and narrow. As one commentator aptly noted,

Lego people scream as a narrator describes hyperinflation, where prices increase at uncontrollable levels, before they’re reassured that the Fed’s got things under control. The final moments leave watchers with a sense of peace, showing how the Fed can keep inflation on track using its various policy tools.

“With the help of the Federal Reserve, there’s just the right amount of inflation,” the narrator explains…

A still image from an animated video released by the Federal Reserve Bank of Cleveland.

The right amount of inflation my eye!

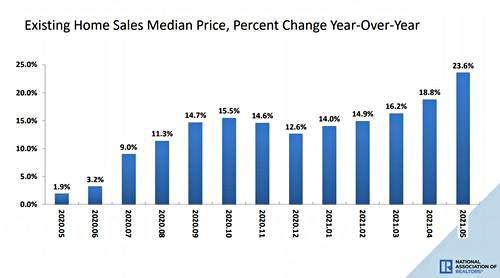

Among the manifold kinds of inflation the Fed fosters, today’s report that the median US home prices increased by 23.6% in May versus last year is surely a reminder that inflation is neither benign nor just.

To be clear, we are not talking about they hoary “base effect”, either. Even last May at the bottom of the lockdown, home prices were up by nearly 2%, while the record $350,000 median price reported for May 2021 was 36% higher than the $262,000 average price during 2018.

Needless to say, the Fed’s cheap money housing boom is occurring right where you might expect it. As is the case with the stock market, the housing boom is distinctly an upper income affair. While May sales for homes above $1 million were up by a staggering 245%, volumes at prices below $250,000 were actually down from last year.

And yet these clowns say their policies have nothing to do with the growing (artificially generated) wealth disparities in American society. That’s just plain risible nonsense.

Even more importantly, there is nothing new about the above. Wage earners have been running a losing race with Fed-fueled housing price inflation for decades. But that’s especially been the case since Alan Greenspan famously noted the rise of “irrational exuberance” in asset markets in December 1997 and then promptly shoved said observation into the memory hole at the Eccles Building.

In fact, since then housing prices (purple line) are up by nearly 150%, while average weekly earnings of all private employees (brown line) have barely risen by 95%. There is absolutely no economic benefit to that yawning gap, while there is an absolute certainty that soaring house inflation is a direct result of the Fed’s massive repression of interest rates.

In a world where down payments are as low as 5% and rarely more than 20%, rock bottom mortgage rates are simply financial kerosene that fuels the inflationary housing fires.

Median US Home Price Versus Average Weekly Earnings, 1997-2020

Then again, the kind of housing inflation depicted above is not an equal opportunity interloper. It is actually profoundly capricious, conferring massive windfall gains on longtime home-owning Baby Boomers, while shellacking first time buyers and younger move-up households.

There is simply no possible justification for state policy interventions which result in such caprice, and especially when the offending central bankers are beyond any kind of democratic accountability.

Nor is the story any better for renters. As of May 2021, the median national rent reached $1,527, up 5.5% compared to a year ago, with median rents rising in 43 of the 50 largest metro areas.

Likewise, this isn’t a “base effect” case, either. Monthly rental prices are up 7.5% nationwide over the past two years, and are now above the pre-Covid trend (dashed purple line).

Needless to say, all of the Fed’s madcap stimulus has not resulted in more housing construction, which is the ostensible purpose.

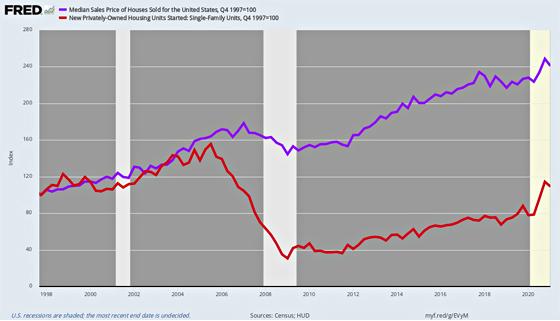

In fact, even with the recent construction mini-boom, single family starts are only up 9% since 1997, even as the median price has soared by the aforementioned 150%.

Median Home Prices Versus Housing Starts, 1997-2021

Of course, ultra low rates are good for something, if not rising living standards: Namely, financial engineering and speculation. That was made clear today when the nation’s largest single family landlord – the Blackstone Group – paid an insane $6 billion for Home Partners of America.

They latter is also a financial engineering roll-up, with about 17,000 rental units, meaning that Blackstone paid around $350,000 per unit. And that’s not owing to their modest cash flows which are projected to generate about a 5% net returns, but because Blackstone’s carry cost cost of capital is rock bottom.

In behalf of our 20-years ago partner, Steve Schwarzman, thank you, Fed!

In short, the overwhelming impact of the Fed’s hideous interest rate repression is rampant speculation in the financial markets and among the C-suites. As of June 11, for instance, YTD stock buyback announcements total a record $567 billion.

Since the top 1% and 10% of households own 53% and 88% of the stocks, respectively, it is pretty evident what the Fed’s misbegotten policies actually produce: A massive channeling of wealth to the top of the economic ladder – even as savers, wage earners, renters and younger and less affluent home buyers all take it on the chin.

At the end of the day, the camarilla of money-pumpers led by the likes of John Williams are damn near criminally incompetent. They now have junk bond spreads at the lowest level in history, and there is no doubt as to where all that radically mispriced capital is going.

To wit, to fuel the financial machinations of speculators and financial engineers, who simply extract rents from the existing stock of wealth rather than create more of it.

Tyler Durden

Fri, 06/25/2021 – 12:45

They’re “Damn Near Criminally Incompetent” – David Stockman Crushes “Camarilla Of Money-Pumpers”

Authored by David Stockman via Contra Corner blog,

A Fed Lifer’s Five Basis Point Farce

We start with this gem from NY Fed president John Williams. He claims the Fed must keep injecting $120 billion per month of fraudulent credit into Wall Street because, apparently, this quarter’s likely 7% real GDP growth and 5% inflation are not sufficient to meet the Fed’s goals:

“… the data and conditions have not progressed enough for the Federal Open Market Committee to shift its monetary policy stance of strong support for the economic recovery.”…

You can’t say enough bad things about this knucklehead. He’s the very poster boy for the camarilla of academics and Fed lifers who have hijacked the nation’s central bank.

For want of doubt, here is William’s career since age 18:

1980-1984: A.B. in economics at University of California at Berkeley;

1985-1989: MA in economics at London School of Economics;

1990-1994: PhD in economics at Stanford University;

1995-2002: Federal Reserve Board staff economist;

2003-2010: Director of Research at the San Francisco Fed;

2011-2018: President, San Francisco Fed;

2018-2021: President, New York Fed.

Does this man remind you of a medieval theologian who never escaped the bosom of the Roman Catholic Church, and who did truly believe you can count the number of angels on the head of a pin?

Stated differently, Williams has been so mentally flayed by 40 years of captivity in macroeconomic models and the Fed’s theological groupthink that he can no longer think at all. And the evidence is overwhelming.

Even as the Fed is injecting $120 billion of fresh cash into the dealer markets each and every month, Wall Street has become so waterlogged with cash that upwards of $800 billion is being loaned right back to the Fed via its so-called o/n RRP facility.

That’s right. These drunken sailors have printed so much money that even Wall Street couldn’t find a place to park it with a yield above the 0.00% level that was on offer at the Fed’s RRP window.

So as head of the Fed’s trading desk on Wall Street, what did Williams propose?

Why nothing less than forcing what amounts to five more monetary angels to sit on the head of the Fed’s sacred pin.

That is to say, the money market was so waterlogged with cash that the GC repo rate (red line), which is the general collateral overnight secured borrowing rate in the tri-party repo market, was being pushed under 0.00%. It was therefore threatening to drive the Fed’s sacrosanct target rate for Federal funds below its official 0-10 basis point corridor.

But when it comes to the pure marginalia of a handful of basis points in the overnight money market, the Fed commands absolute obedience. Never mind that the funds rate does not make one damn bit of difference to the borrowing costs of any household or business on main street America. And we do mean zero “difference” as in nichts, nada and nugatory.

Don’t tell Dr. John Williams, however. By his lights, the Fed must be and will be obeyed by the money markets. Period.

So at its recent meeting, the Fed under Williams guidance raised the lower and upper bounds of the control corridor by the astounding sum of, well, five basis points!

That’s right. To keep cash heavy Wall Street operators from parking funds overnight in the GC repo market below its 0.00% dictum at the bottom of the corridor, its raised its RRP offer rate to 0.05% (dashed light blue line).

By the same token, banks are now choking on $3.8 trillion of excess reserves . So to keep them from putting these reserves to work at rates below the upper corridor of its sacrosanct policy target, the Fed raised its IOER rate (interest paid on excess reserves) from a comical 10 basis points to an only slightly less ludicrous 15 basis points (dashed purple line).

This farce, which was announced in weighty techno-speak, amounted to the 6-year old bully in the sandbox expostulating a belligerent, “take that!”

What the 5 basis point RRP rate actually means, of course, is that sitting on a $8.0 trillion balance sheet of essentially risk free sovereign debt, the Fed nonetheless will now borrow unlimited amounts at 5 basis points from money market funds and others engorged with cash.

Let us repeat the word borrow: The Fed is paying money markets to bring coals to Newcastle, and for no rational purpose other than because it says so.

For crying out loud, if it really wanted to drain excess cash from the money markets, which is what the recent $800 billion of o/n RRP facility borrowing amounted to, it could just sell a small portion of its immense $8 trillion hoard of Treasury bills and notes or GSE securities.

But, no, that would amount to an admission that its is changing it “policy stance” toward tightening – a shift that the Keynesian fanatics like Williams who dominate the FOMC cannot abide.

Indeed, borrowing cash from Wall Street with one-arm while it is pumping out massive new quantities of the same with its other arm is about as absurd as it gets. And paying banks 15 basis points to keep excess reserves stashed at the New York Fed is even more so.

The chart below tells you all you need to know. In its misbegotten quest to keep interest rates at essentially zero on the front end of the curve, and well under 1.0% for tenors out to five years, the Fed has pumped so much cash into the banking system as to bury it in Ben Franklins.

Since the current reserve requirement on transactions balances was lowered to zero last year, the entirety of bank reserves now amount to excess reserves, which figure totaled $3.89 trillion at the end of April.

Do these people have a screw loose? The banks are literally submerged in cash, but the likes of John Williams won’t even talk about talking about tapering their $120 billion per month printathon of even more cash.

It is worth noting the thin purple area of the chart stretching from 1947 to exactly August 2008. That was the eve of the Lehman meltdown, which event caused Bernanke to jump the shark at the Fed’s printing press, nearly tripling its balance sheet in barely 13 weeks.

Before the Bernanke tsunami, however, total banking system reserves amounted to just $46 billion or a scant 0.3% of GDP. And that, in turn, represented a 50-year trend of declining bank reserves relative to GDP. The former had stood at about $30 billion and 2.5% of GDP when Nixon pulled the plug on gold-backed money in August 1971 and barely 1.2% of GDP when Greenspan cranked up the printing presses in October 1987 to bailout Wall Street from a 22% one-day meltdown.

By the end of April 2021, by contrast, bank reserves stood 17.7% of GDP, and for no valid reason of economics, finance or banking. Banks were choking on cash because the madmen in the Eccles Building mindlessly believe, as John Williams averred above, that near-zero interest rates and massive monetization of the public debt are “supporting the economic recovery”.

Total Reserves of the Banking System

No, they are not. Upwards of $6 trillion of fiscal stimulus is doing that job, and then some.

What zero interest rates are actually doing is literally destroying every market function that is necessary for sustained capitalist growth and prosperity and the natural equities of the free market, as well.

The foremost victim of the Williams/Fed variety of “support for the recovery” is the function of generating real money savings from current production and income. The Fed’s ZIRP policy means that savers unwilling to expose their hard-earned wealth to the wild west casino in the stock and bond markets, which have metastasized from the Fed’s mindless money-printing, are effectively SOL.

The chart below covers the 244 months since January 2001 and measures the difference between the 90-day T-bill rate as a proxy for liquid savings and the year-over-year change in the CPI. That is, the real return on savings.

As it has happened, the real savings rate has been negative during 187 of those months, or 77% of the time since 2001, when the Greenspan Fed went into money-printing hyper-drive to erase the impact of the dotcom crash.

Forget the loss of economic function that must necessarily occur when the supply of savings dries up. These Keynesian nincompoops have been anti-savings since JM Keynes himself called for the euthanasia of the bond owning rentiers back in the 1930s.

But what is even more diabolical is the Fed’s implicit edict to blue-haired widows and cautious younger people alike: Namely, put your wealth in harms’ way in the casino via the stock market or junk bonds or we will liquidate it through negative real returns on savings accounts until the cows come home.

Indeed, if the Fed could be indicted for grotesque economic and social injustice – this chart is the smoking gun. After all, never in a million years on an honest free market of sound money would savers and borrowers form the hideous bargains shown below in the vast areas below the zero line, and for 20-years running at that.

Real Return On Liquid Savings, 2001-2021

Of course, the lifetime savings of tens of millions of citizens are being gutted by an unelected monetary politburo in a manner that has never, ever been, or could be, authorized by the US Congress; and for the malign purpose of insuring the very right amount of inflation as divined by power-hungry crackpots like Powell, Williams, Clarida, Brainard and the rest of the Keynesian posse, whose contributions to the latest Fed dot plot say that the first rate-hike will not occur until 2024!

That’s sheer madness. These people are obliterating every rule of sound money and rational finance in a futile effort to deliver something that benefits no one. Namely, 2.00% inflation averaged over a secret period of time known only to the self-appointed high priests of the latter day monetary temple known as the Fed.

In fact, the crackpots in the Cleveland branch of the Fed have gone so far as to produce Lego-based animated videos explaining inflation and how the Fed has the tools to keep it on the straight and narrow. As one commentator aptly noted,

Lego people scream as a narrator describes hyperinflation, where prices increase at uncontrollable levels, before they’re reassured that the Fed’s got things under control. The final moments leave watchers with a sense of peace, showing how the Fed can keep inflation on track using its various policy tools.

“With the help of the Federal Reserve, there’s just the right amount of inflation,” the narrator explains…

A still image from an animated video released by the Federal Reserve Bank of Cleveland.

The right amount of inflation my eye!

Among the manifold kinds of inflation the Fed fosters, today’s report that the median US home prices increased by 23.6% in May versus last year is surely a reminder that inflation is neither benign nor just.

To be clear, we are not talking about they hoary “base effect”, either. Even last May at the bottom of the lockdown, home prices were up by nearly 2%, while the record $350,000 median price reported for May 2021 was 36% higher than the $262,000 average price during 2018.

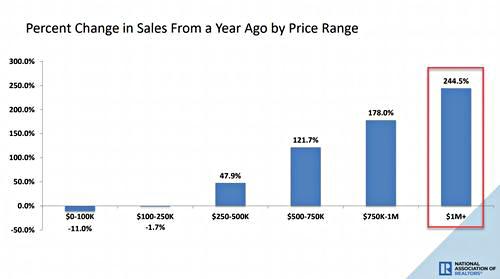

Needless to say, the Fed’s cheap money housing boom is occurring right where you might expect it. As is the case with the stock market, the housing boom is distinctly an upper income affair. While May sales for homes above $1 million were up by a staggering 245%, volumes at prices below $250,000 were actually down from last year.

And yet these clowns say their policies have nothing to do with the growing (artificially generated) wealth disparities in American society. That’s just plain risible nonsense.

Even more importantly, there is nothing new about the above. Wage earners have been running a losing race with Fed-fueled housing price inflation for decades. But that’s especially been the case since Alan Greenspan famously noted the rise of “irrational exuberance” in asset markets in December 1997 and then promptly shoved said observation into the memory hole at the Eccles Building.

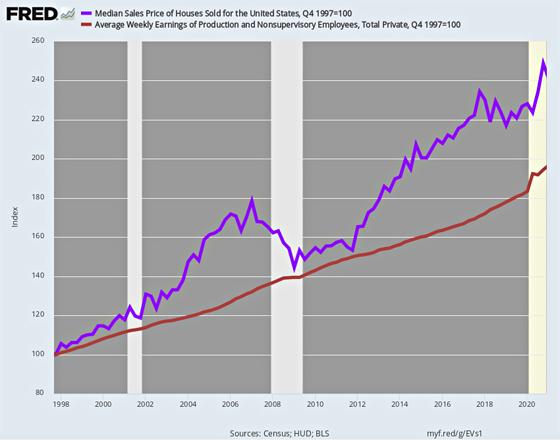

In fact, since then housing prices (purple line) are up by nearly 150%, while average weekly earnings of all private employees (brown line) have barely risen by 95%. There is absolutely no economic benefit to that yawning gap, while there is an absolute certainty that soaring house inflation is a direct result of the Fed’s massive repression of interest rates.

In a world where down payments are as low as 5% and rarely more than 20%, rock bottom mortgage rates are simply financial kerosene that fuels the inflationary housing fires.

Median US Home Price Versus Average Weekly Earnings, 1997-2020

Then again, the kind of housing inflation depicted above is not an equal opportunity interloper. It is actually profoundly capricious, conferring massive windfall gains on longtime home-owning Baby Boomers, while shellacking first time buyers and younger move-up households.

There is simply no possible justification for state policy interventions which result in such caprice, and especially when the offending central bankers are beyond any kind of democratic accountability.

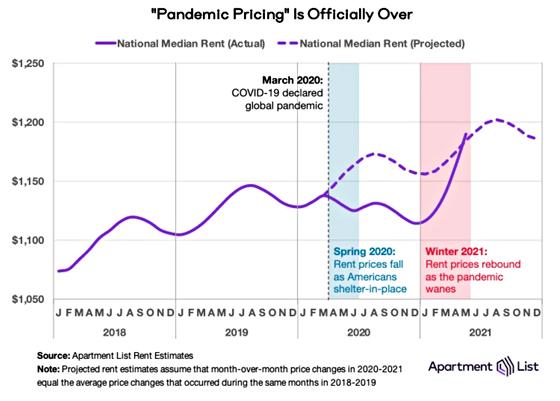

Nor is the story any better for renters. As of May 2021, the median national rent reached $1,527, up 5.5% compared to a year ago, with median rents rising in 43 of the 50 largest metro areas.

Likewise, this isn’t a “base effect” case, either. Monthly rental prices are up 7.5% nationwide over the past two years, and are now above the pre-Covid trend (dashed purple line).

Needless to say, all of the Fed’s madcap stimulus has not resulted in more housing construction, which is the ostensible purpose.

In fact, even with the recent construction mini-boom, single family starts are only up 9% since 1997, even as the median price has soared by the aforementioned 150%.

Median Home Prices Versus Housing Starts, 1997-2021

Of course, ultra low rates are good for something, if not rising living standards: Namely, financial engineering and speculation. That was made clear today when the nation’s largest single family landlord – the Blackstone Group – paid an insane $6 billion for Home Partners of America.

They latter is also a financial engineering roll-up, with about 17,000 rental units, meaning that Blackstone paid around $350,000 per unit. And that’s not owing to their modest cash flows which are projected to generate about a 5% net returns, but because Blackstone’s carry cost cost of capital is rock bottom.

In behalf of our 20-years ago partner, Steve Schwarzman, thank you, Fed!

In short, the overwhelming impact of the Fed’s hideous interest rate repression is rampant speculation in the financial markets and among the C-suites. As of June 11, for instance, YTD stock buyback announcements total a record $567 billion.

Since the top 1% and 10% of households own 53% and 88% of the stocks, respectively, it is pretty evident what the Fed’s misbegotten policies actually produce: A massive channeling of wealth to the top of the economic ladder – even as savers, wage earners, renters and younger and less affluent home buyers all take it on the chin.

At the end of the day, the camarilla of money-pumpers led by the likes of John Williams are damn near criminally incompetent. They now have junk bond spreads at the lowest level in history, and there is no doubt as to where all that radically mispriced capital is going.

To wit, to fuel the financial machinations of speculators and financial engineers, who simply extract rents from the existing stock of wealth rather than create more of it.

Tyler Durden

Fri, 06/25/2021 – 12:45

Read More

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}