U.S. and European leaders now face an unpleasant choice as they decide how aggressively to use economic sanctions in response to Russia’s military invasion of Ukraine.

The moral imperative is to exert maximum economic pressure rapidly on Russia to end the fighting in Ukraine as quickly as possible and repel Russian forces. But the economic imperative is to protect businesses and employment at home, minimise the fallout for lower income households and sustain support for sanctions policies.

In mid-February, top policymakers appeared to have thought they could reconcile these objectives through a carefully controlled sanctions escalation strategy exempting oil and gas trade. But that plan has broken down as a result of Russia’s slow progress on the battlefield and immense diplomatic and public pressure on U.S. and European leaders to maximise sanctions swiftly.

U.S. and European policymakers must choose between imposing maximum pressure on Russia by cutting off oil and gas purchases or a more modest approach that will avert recession.

Recession Indicators

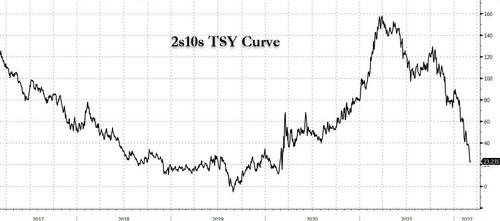

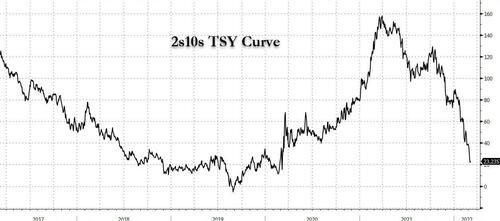

Even before the invasion, the rapid economic rebound after the pandemic was beginning to decelerate, price increases were accelerating and interest rates were set to rise. The flattening U.S. Treasury yield curve indicated a heightened probability of a mid-cycle slowdown or end-of-cycle recession in the next year.

Russia’s invasion and the sanctions that have followed super-charged these trends, disrupting supply chains, sending energy and food prices soaring and flattening the yield curve further.

The financial crisis in 2008/2009 and the pandemic in 2020/2021 were demand-side shocks that could be offset by lowering interest rates, buying bonds, cutting taxes and boosting unemployment insurance. But the invasion and sanctions are a supply-side shocks that have cut the global economy’s production capacity so they cannot be offset in the same way.

Boosting demand by more bond buying, cutting taxes or increasing government spending would simply worsen the production-consumption gap and fuel even faster inflation.

The crisis threatens to disrupt global trade in critical raw materials and industrial components ranging from aluminium, nickel and noble gases to car parts, ocean shipping and overland rail freight.

But the biggest and most immediate impact is being felt in petroleum and natural gas, where Russia is one of the world’s top exporters, and grain, where both Russia and Ukraine are major global suppliers.

Energy and food prices, which were already rising before the invasion, are now climbing at the fastest rate for 50 years, at a time when wages are increasing slowly, putting pressure on businesses and household finances.

Lower income households in advanced and developing economies will be hit particularly hard since they spend a much higher share of their income on food and fuel and have fewer options to modify spending patterns.

Uncontrolled Escalation

Top U.S. and European policymakers seem to have been alert to the risks when threatening to impose unprecedented sanctions in an effort to deter Russia’s invasion. U.S. and European sanctions were carefully crafted to exclude trade in oil, gas and other energy items from the embargo and to permit energy-related financial transactions.

Planning had assumed that sanctions would be intensified progressively and measures targeting oil and gas flows would be imposed last, if at all.

The controlled escalation strategy was designed to deter and punish Russia while limiting costs for motorists, households and energy-intensive industries in the United States and Europe.

But both sides of the conflict appear to have miscalculated the resolution of the other and underestimated what it would take to bring the conflict to a swift end.

For Russia, that meant misjudging its ability to deliver a rapid victory before sanctions plunged its economy into turmoil.

The United States and Europe, meanwhile, seemed to have assumed incremental sanctions could deter an invasion or bring it to a quick halt before the wider economic fallout was felt. For the West, the result is now broader sanctions that could last longer than anticipated, increasing economic disruption.

Limiting Disruption

U.S. and European policymakers seem to have calculated they could take a strong public line on sanctions while letting oil and gas traders to continue purchasing Russian fuel. But most traders have concluded that the legal and reputational risks are too great and have shunned Russian exports, bringing oil flows to a halt. Shell felt the impact acutely. It purchased a Russian crude cargo on March 4, only to be met with such a public outcry that on March 8 it apologized and said it would stop spot purchases immediately.

Now political pressure is mounting in the United States, and to a lesser extent in Europe which is far more reliant on Russia, for a complete ban on Russian oil and gas imports.

The possibility that the United States and Europe might initiate an embargo has already sent oil and gas prices surging to levels that will be unaffordable for many households and firms if sustained for an extended period.

In response, Russia has indicated it could cut oil and gas exports if economic warfare continued to escalate, a move that would trigger an immediate full-blown energy crisis.

There is no way the United States and Europe can replace Russian oil and gas exports fully within the next 12 months or absorb the consequences of a further price spike without entering recession.

European economies, with much bigger economic exposure to Russia, are particularly at risk of heading into a downturn.

Phased Sanctions?

U.S. and European policymakers may try to announce that they will progressively reduce oil and gas purchases from Russia according to a fixed timetable over the next two to three years. Such a phased reduction in Russian oil and gas purchases every six months would be similar to previous progressive sanctions on Iran’s oil exports.

Such a move would give more time to secure replacement supplies from others including Saudi Arabia, Qatar, Iran, Venezuela and the U.S. shale industry over the 12-36 months. It could also give U.S. and European policymakers negotiating leverage with Russia while reducing, if not eliminating, the immediate upward pressure on energy prices.

Progressive sanctions might even prove more effective if they limit the economic fallout in North America and Europe, and make them more economically and politically sustainable in the medium term.

By John Kemp, Senior Market Analyst at Reuters